If you are a client, login to our portal to view the full report. If your not a client and would like to request access, please email research@bespokeintel.com.

Key Takeaways:

Autos and EVs

- Self-reported auto purchase activity has softened a bit sequentially.

- We have seen declines in those in the market to buy a car in the next 6 months who would choose luxury brands (non-luxury brands have received more consistent feedback). An increasing percentage of consumers (relative to February 2023) are saying that they think the vehicle they own is worth less than the amount they still owe on the car.

- Consumers have been stubborn to shift their thinking on the safety of autonomous vehicles. Over the entire history of our survey, they have viewed humans driving themselves as safer.

Tesla

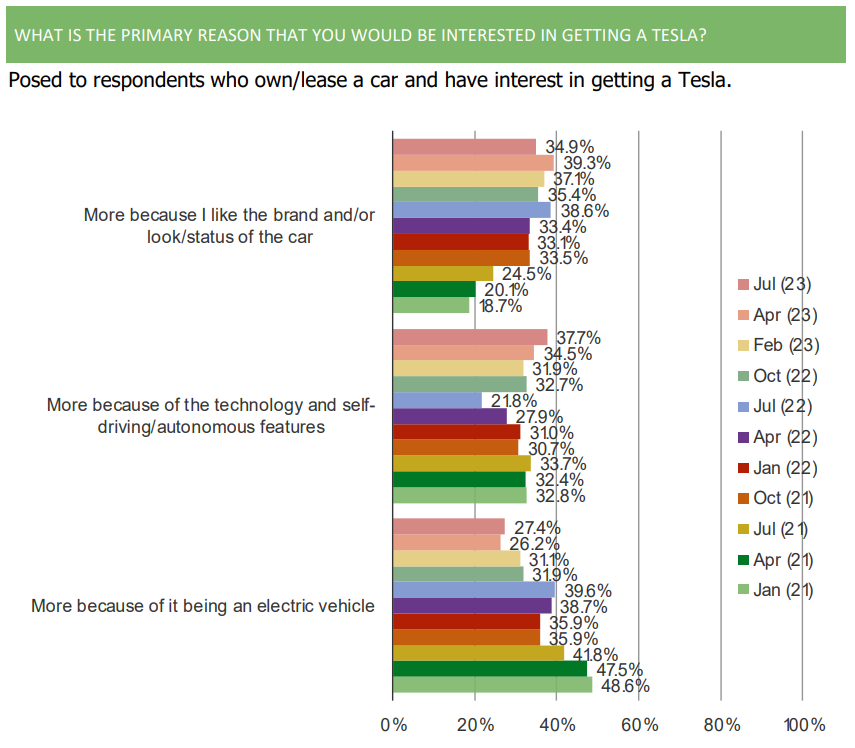

- The share of those interested in getting a Tesla who want it because it is an EV has declined over time. These folks have been increasingly likely to say they are interested in Tesla purely because of the brand and/or look/status of the car or because of the technology / self-driving features.

- The price cuts from Tesla continue to have a positive impact on consumer opinion toward the brand, but interest in getting a Tesla is softer now than it has been in prior waves of this survey.

Sample Chart From Full Report:

Consumers who are interested in Tesla are increasingly more interested because of the brand/technology, and less because it is an EV.