Blog

Bespoke Survey Insights

Credit Card Trends | Top Three Takeaways

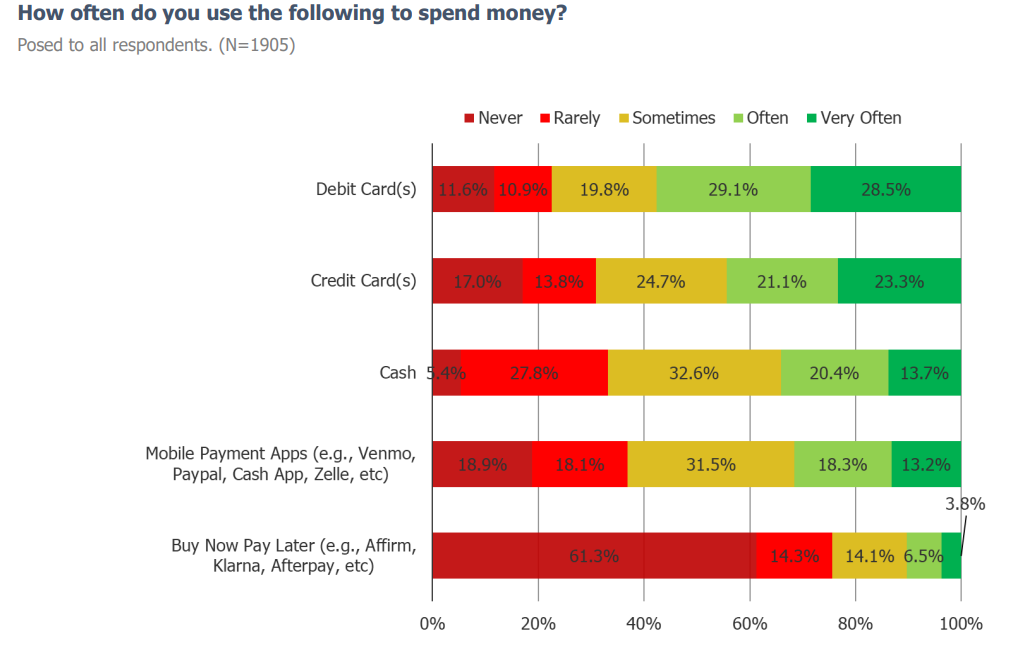

1. Debit cards were the most popular way of spending money in our survey.

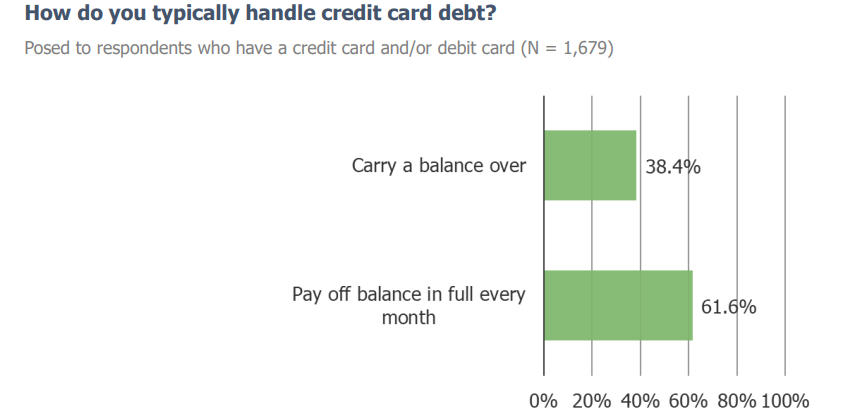

2. 61.6% of respondents report paying off their credit card balance in full every month.

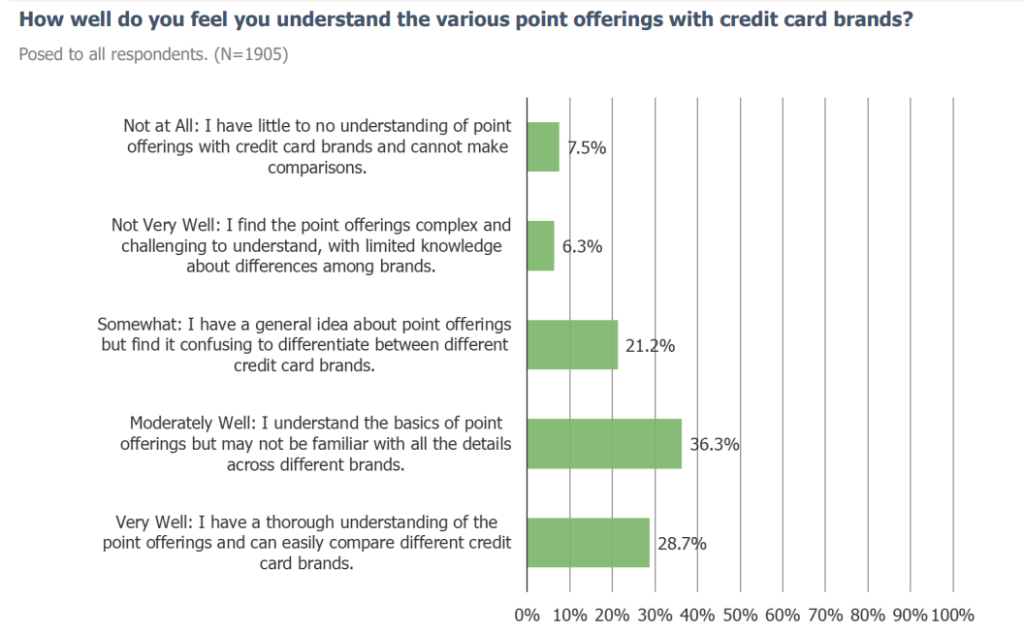

3.A plurality of respondents report understanding their various point offerings with credit card brands very well or moderately well.

SMB Survey | Top Three Takeaways

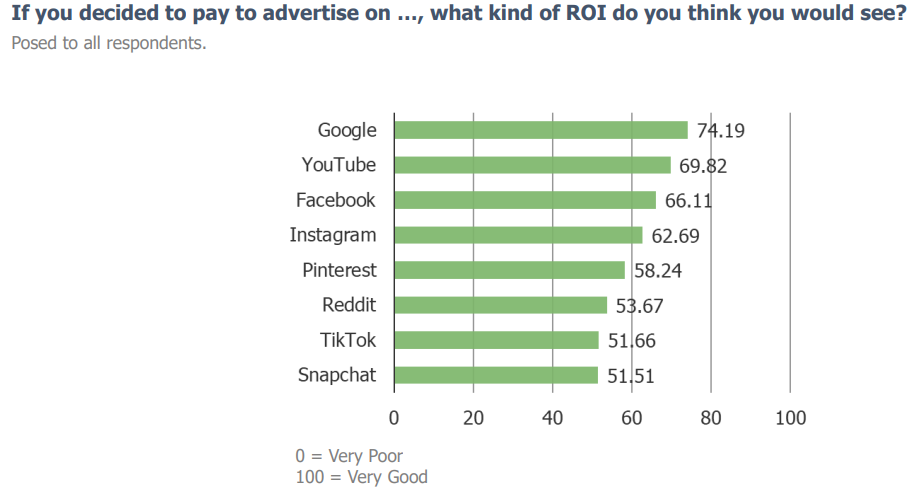

1. SMB owners believe that Google would provide the best ROI for an advertising campaign.

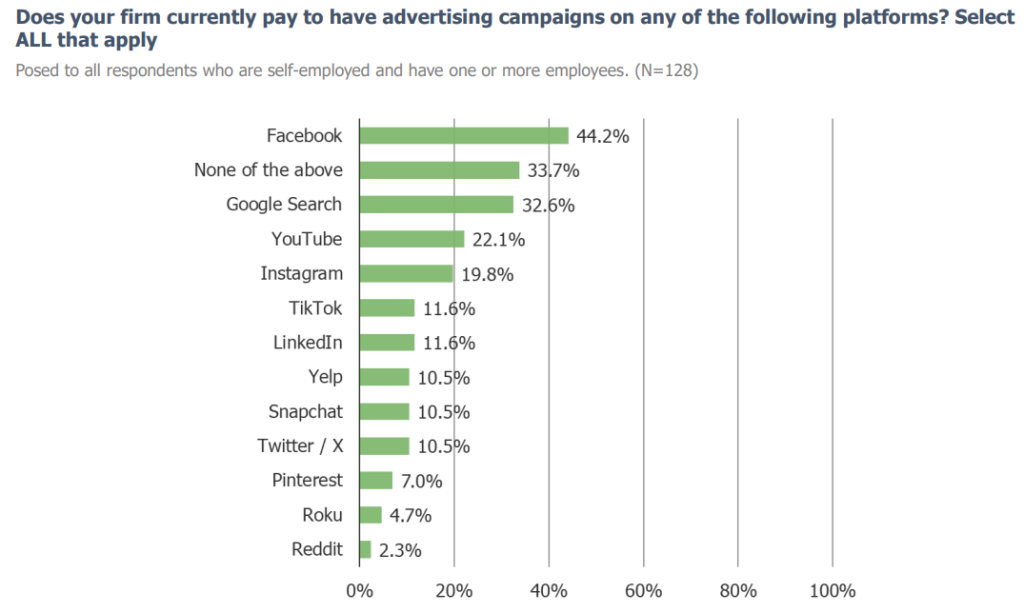

2. The top platform that SMBs choose to advertise on is Facebook.

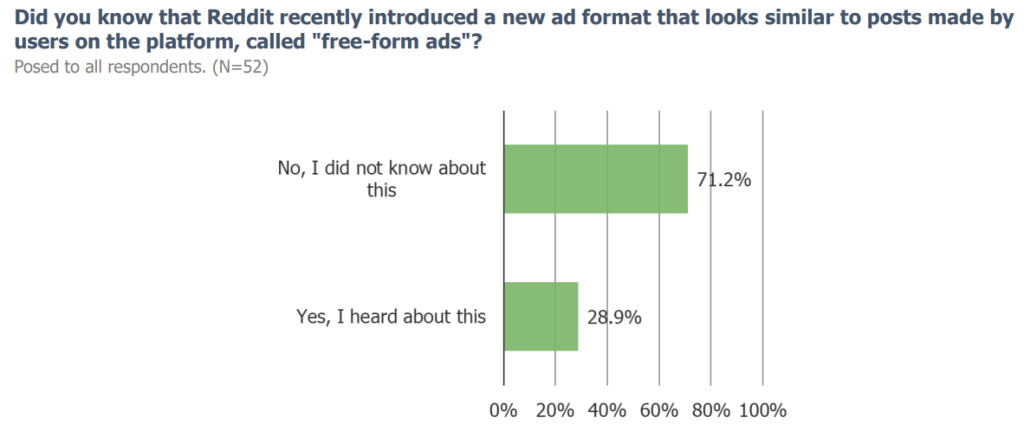

3. A plurality of SMB owners were unaware of Reddit’s Free-Form Ad format.

Video Games | Top Three Takeaways

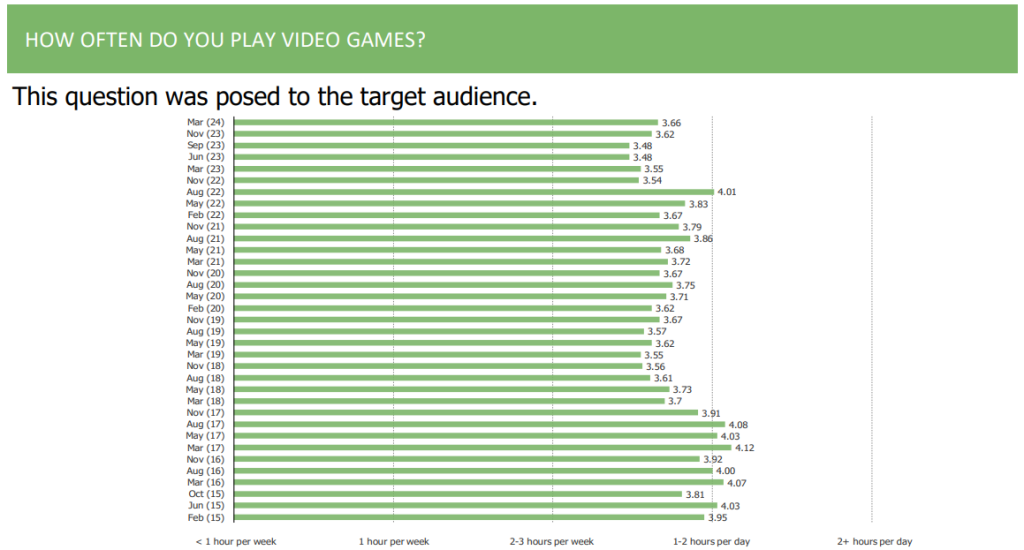

1. Video game playing frequency has improved over this quarter.

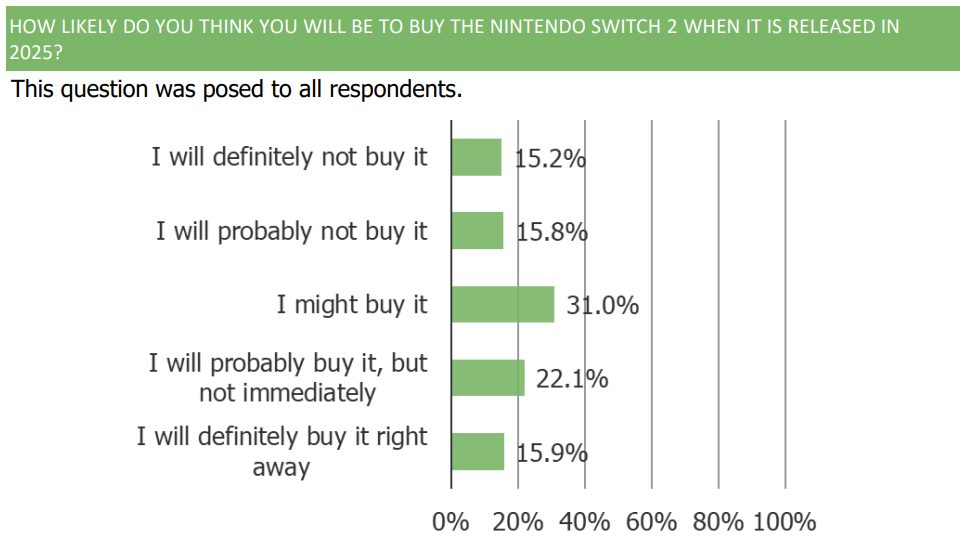

2. There is appetite for the upcoming Nintendo Switch console release in 2025, with a

mixture of responses among those with interest ranging from folks who might buy it,

some who will probably buy it but not immediately, and some who will definitely buy it

right away.

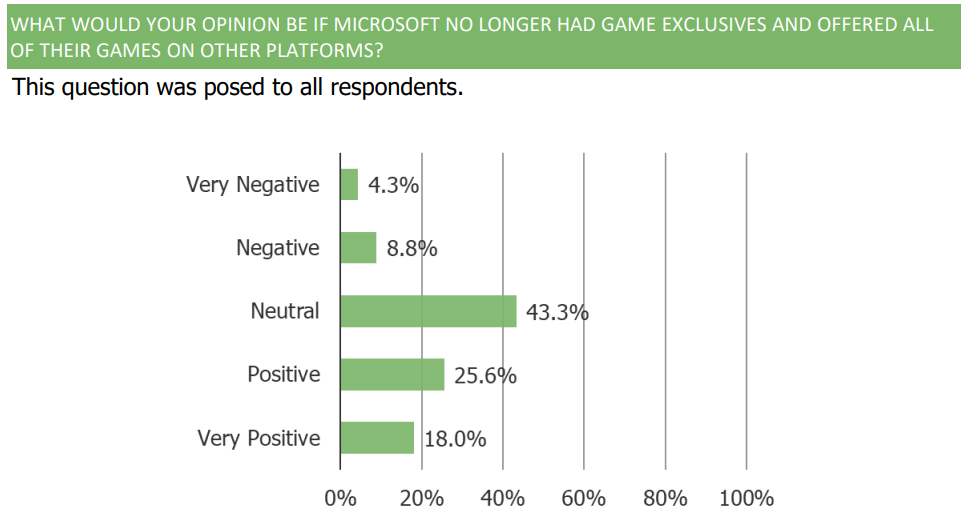

3. Gamers broadly have a net favorable view of Microsoft making Xbox exclusives available on other platforms.

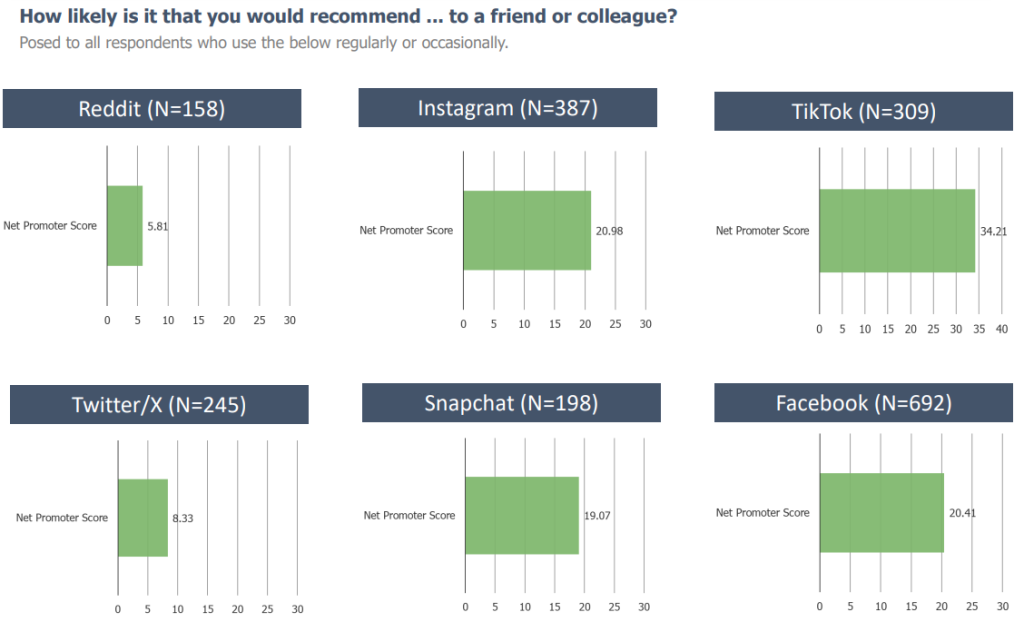

RDDT | Top Three Takeaways

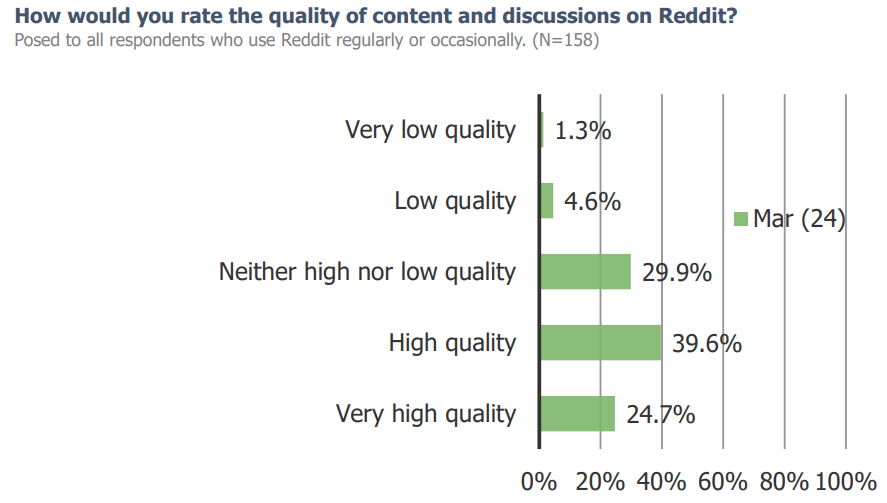

1. Consumers have a positive rating of the quality of content and discussions on Reddit.

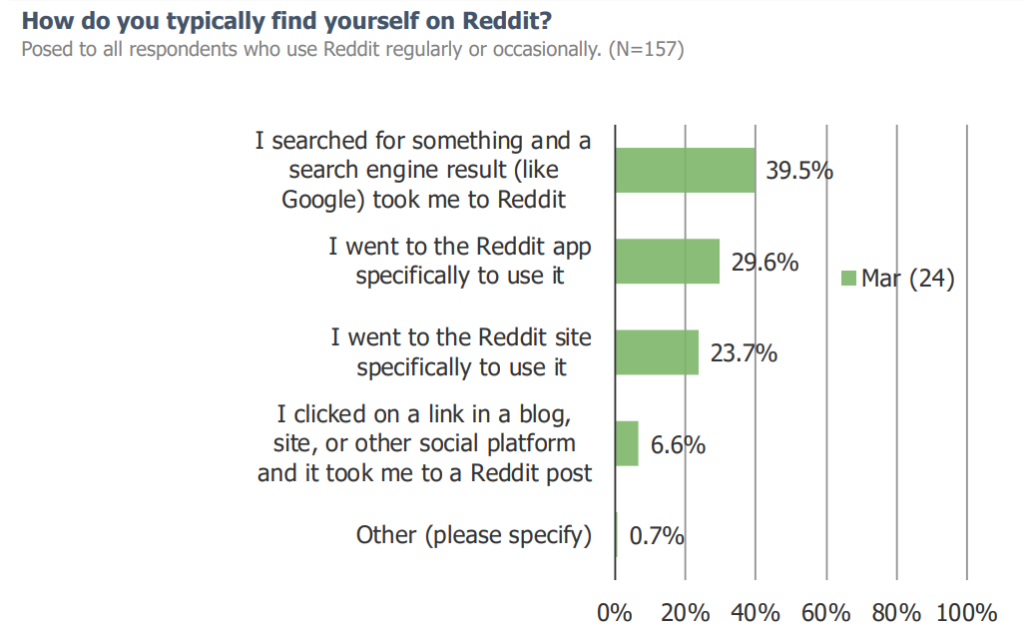

2. A plurality of Reddit users typically find themselves on Reddit after a Google search (ie, makes engagement reliant on placement and emphasis in the Google search algorithm).

3. Consumer NPS is lower than all other social platforms we test.

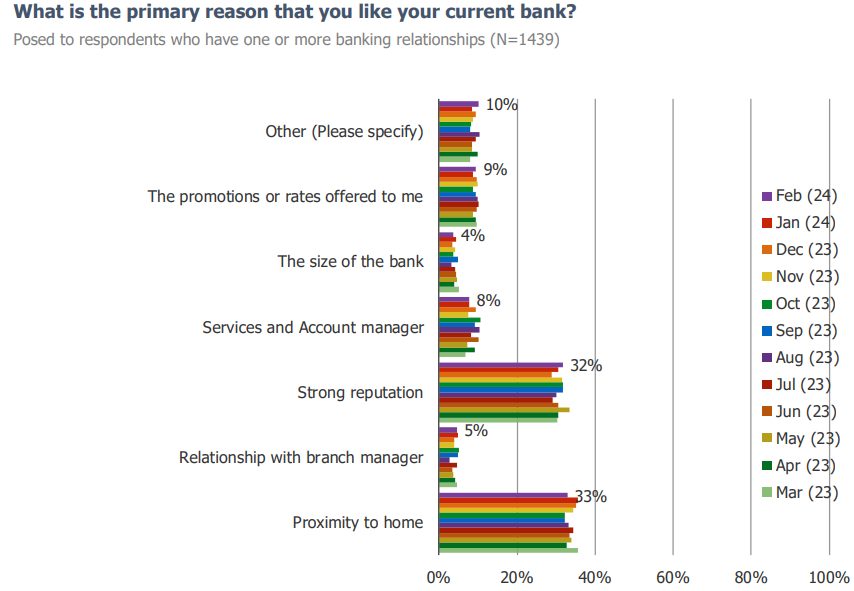

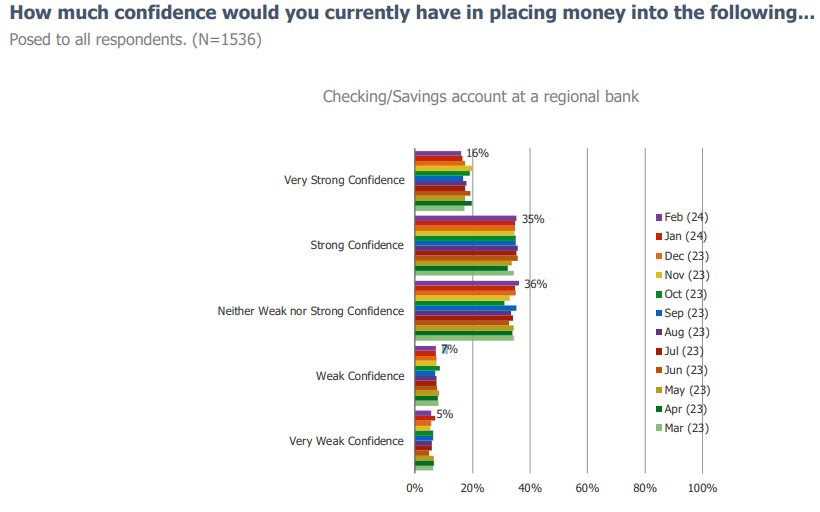

US Banking | Top Three Takeaways

1. The top two reasons for why respondents like their current bank is because of its proximity to their home and the reputation that the bank holds.

2. The vast majority (88%) of respondents have not made any changes to their banking relationships in the past 30 days.

3. A plurality of respondents have a generally strong level of confidence in keeping a checking or savings account with a regional bank.

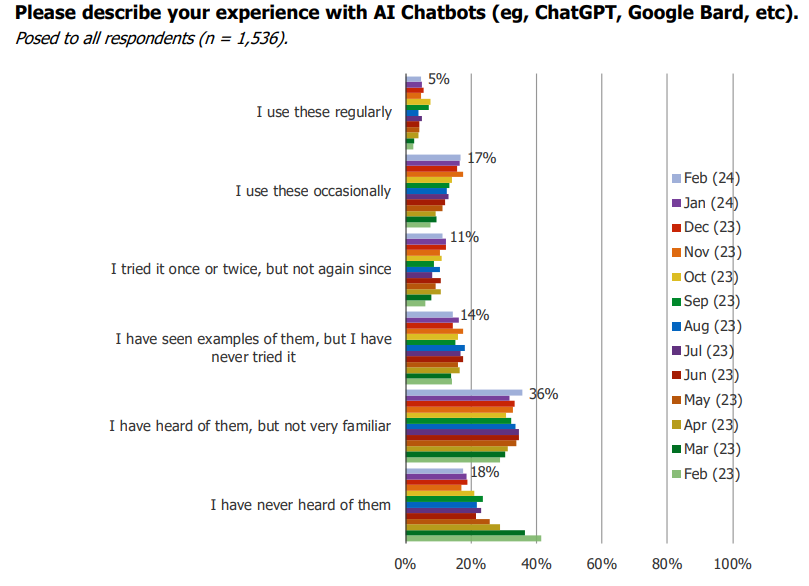

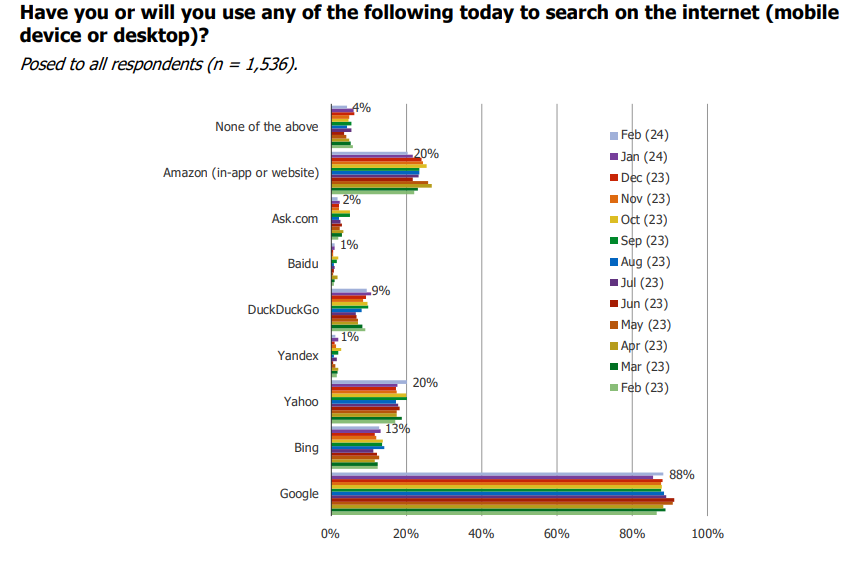

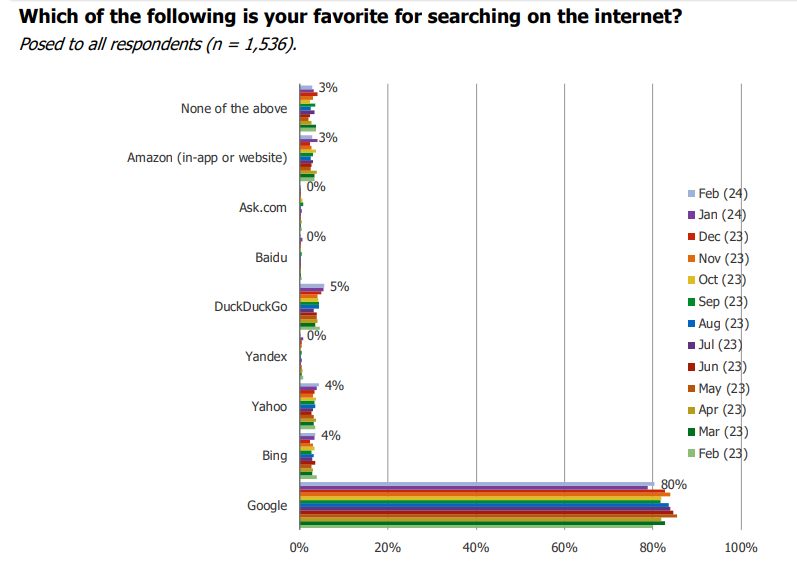

Search & AI | Top Three Takeaways

1. The percentage of consumers who are aware of AI Chatbots continues to increase.

2. When asked about what platform they use for internet search purposes, the vast majority of respondents answered with Google.

3. Google remains the most popular web search platform by a large margin.

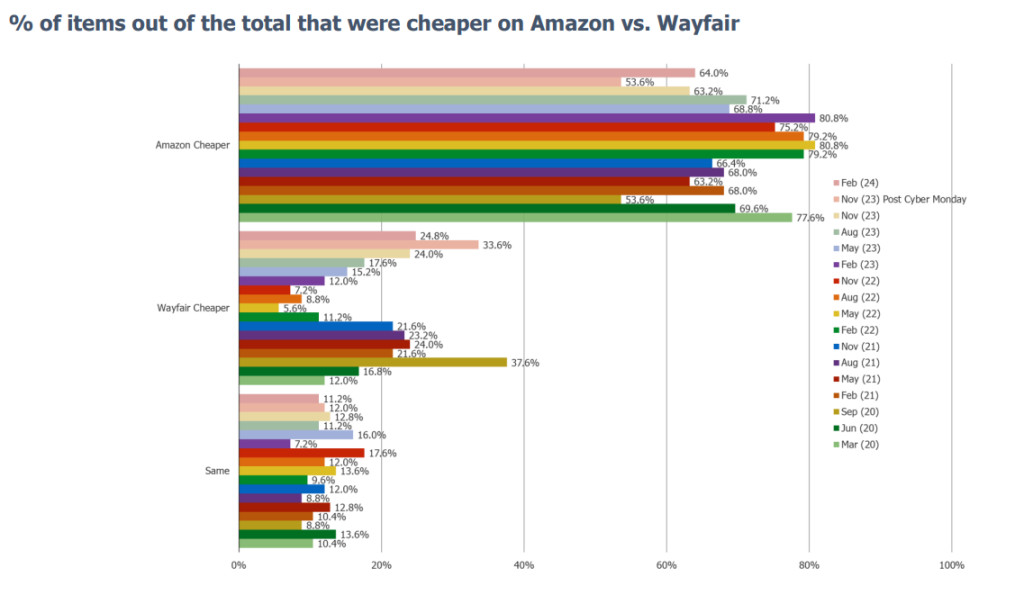

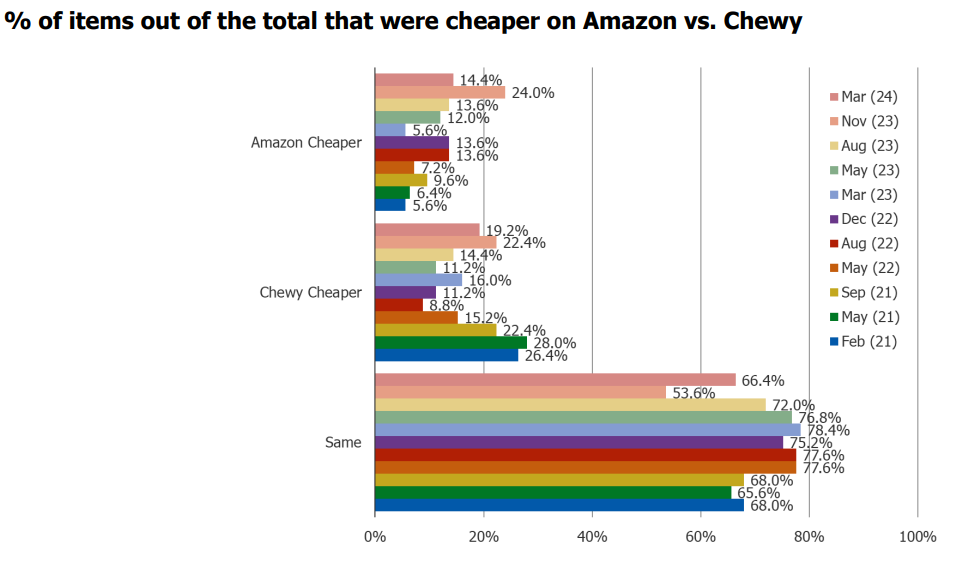

Amazon Pricing Analysis | Top Three Takeaways

1. Over recent quarters, Wayfair has progressively been getting “cheaper” on a growing percentage of identical items found on both Amazon and Wayfair. Amazon is still cheaper more often than not.

2. The share of identical items found on Amazon and Chewy that are cheaper on Chewy was basically unchanged q/q.

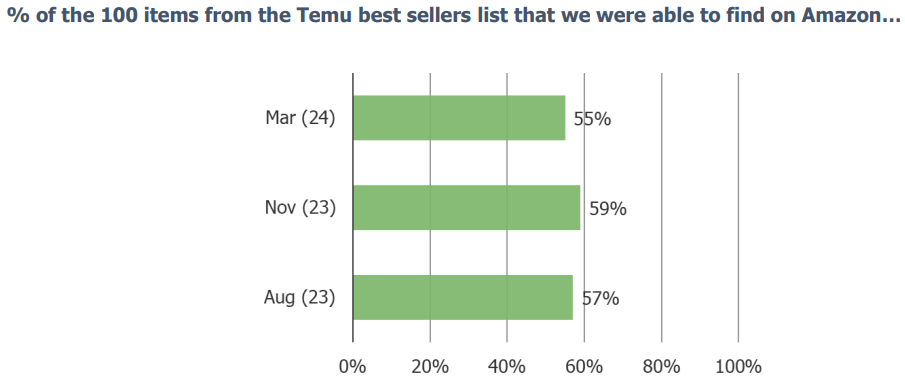

3. Around 55-60% of the best sellers that we pull for analysis from Temu are also available on Amazon. When we find identical items, Temu is cheaper 95% of the time, and by a large amount (Amazon is usually more than double the price).

Macro Update | Top Three Takeaways

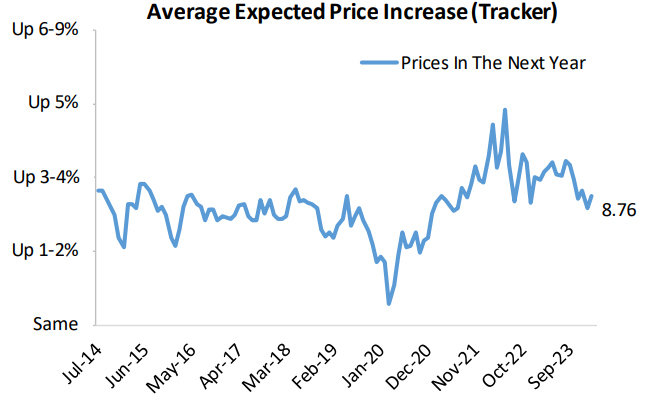

1. Inflation concerns have retreated rapidly and appear to have returned to pre-COVID norms.

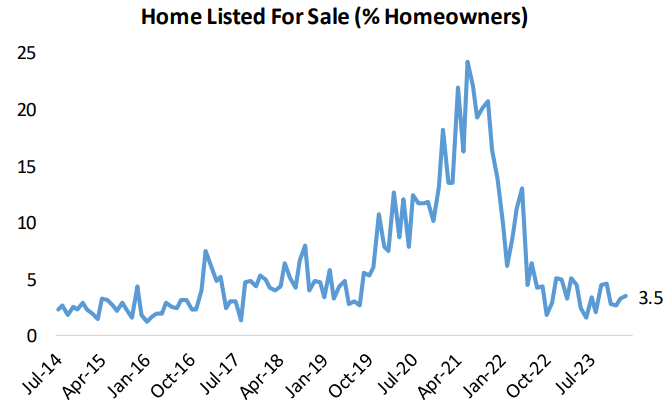

2. Very few respondents report their home listed for sale, a sign that the housing market remains constrained.

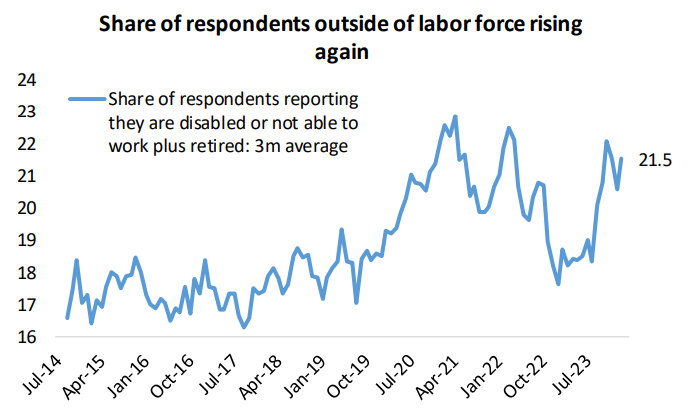

3. Over the last six months our survey reflects a sudden significant uptick in workers leaving the labor force.

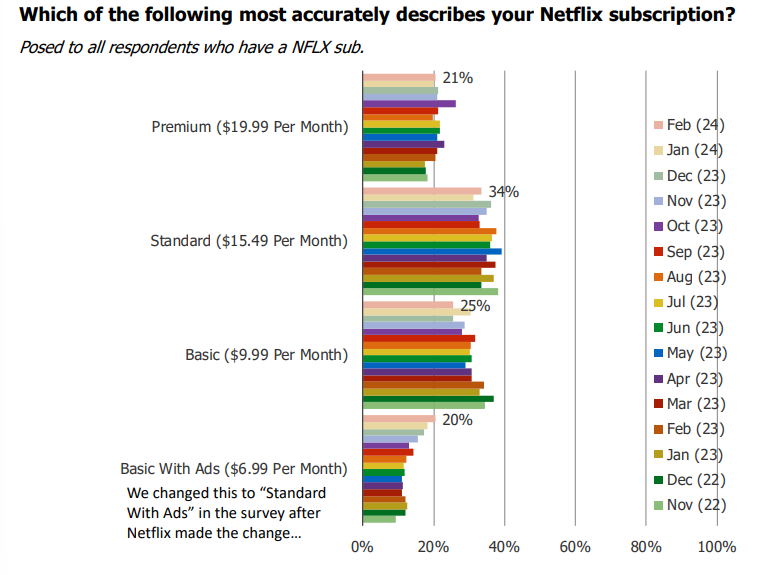

Streaming Video Monthly Update | Top Three Takeaways

1. The share of customers saying they are on the ad-supported plan has been increasing sequentially in our monthly survey.

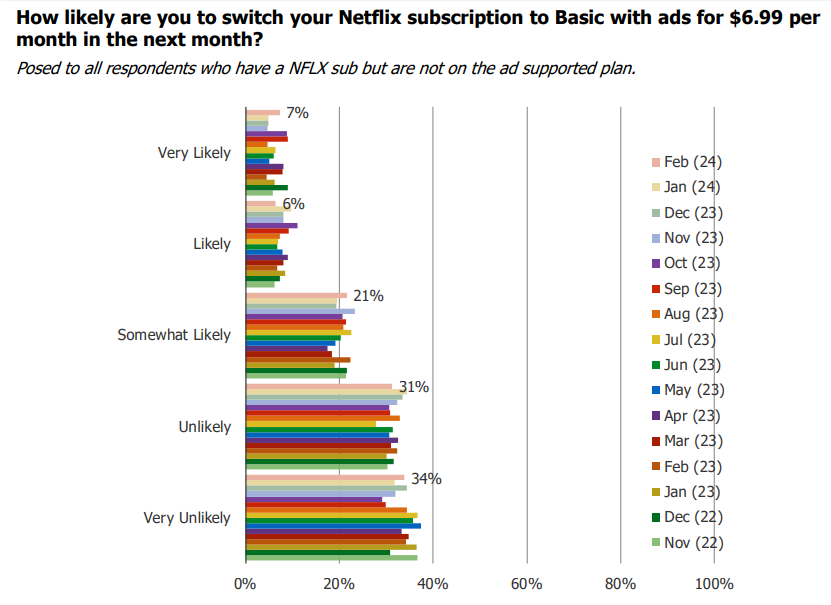

2. The share of respondents who reported that they are very likely to switch subscription packages has increased q/q.

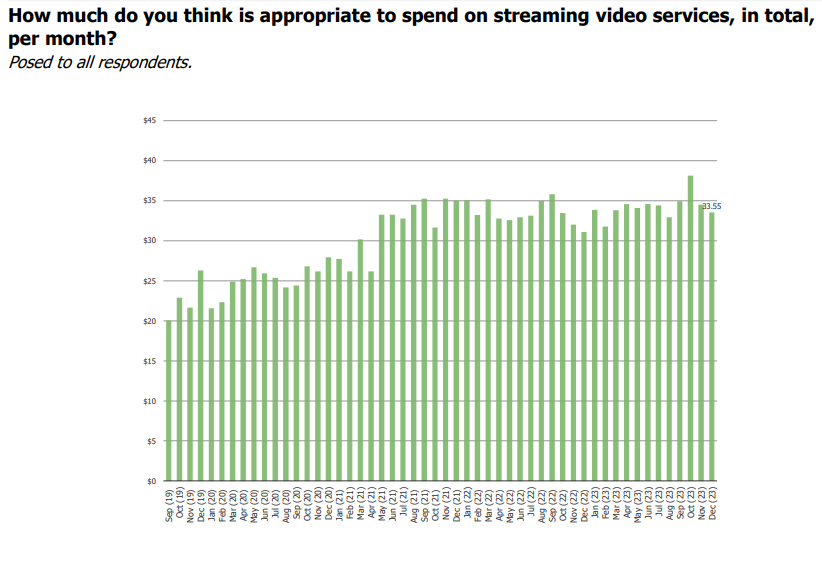

3. The amount that consumers believe is an appropriate price to pay for streaming services has declined over the past few quarters.

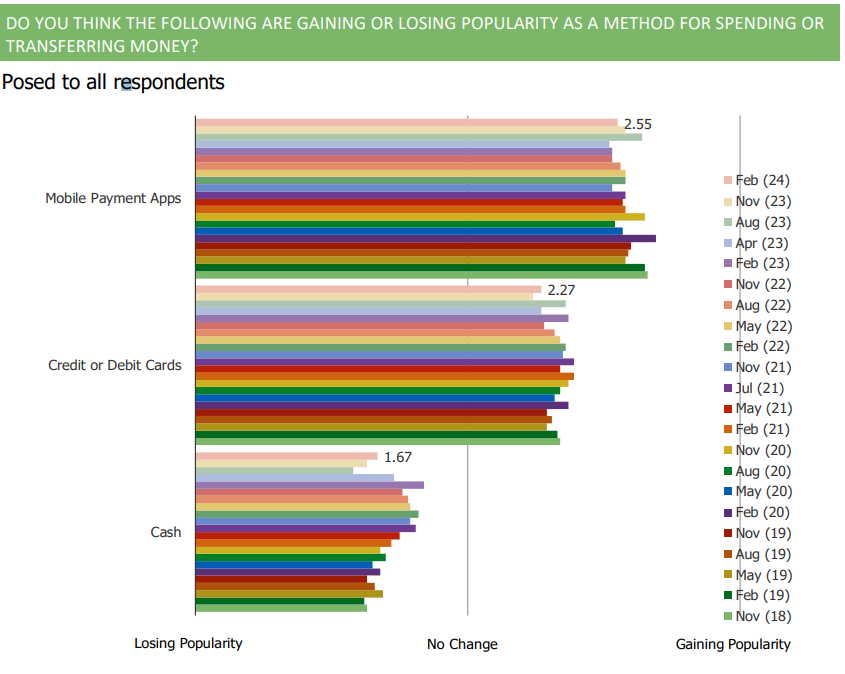

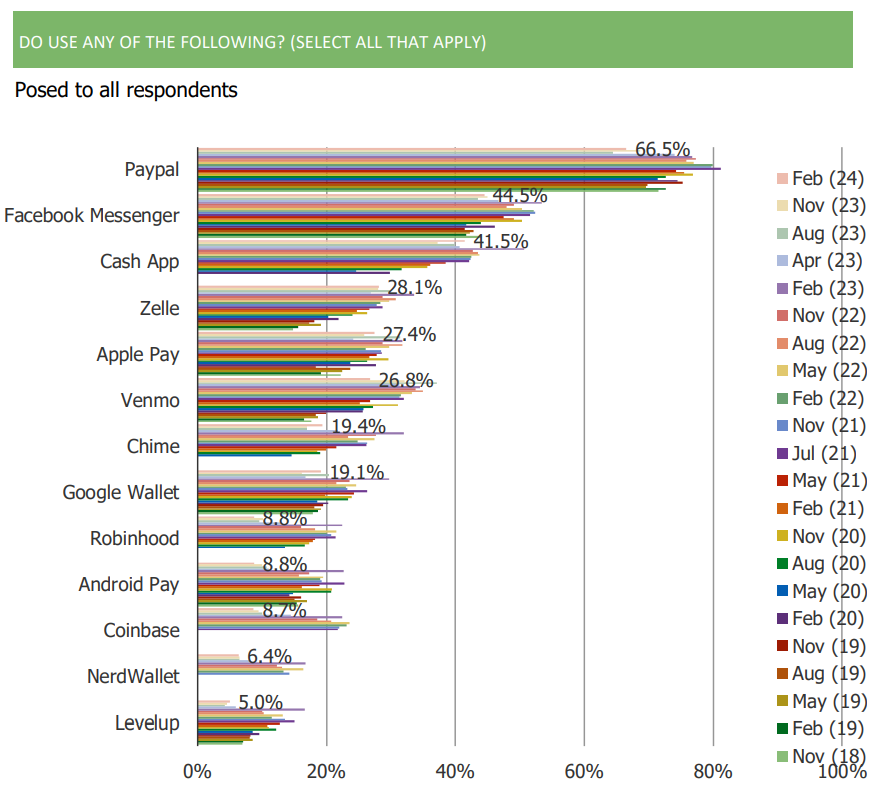

Mobile Payments, Crypto, and Investments | Top Three Takeaways

1. Respondents have been noting that they feel as if mobile payment apps have decreased in popularity over the past few quarters.

2. PayPal usage has increased q/q and remains the most popular of the payment apps that we test.

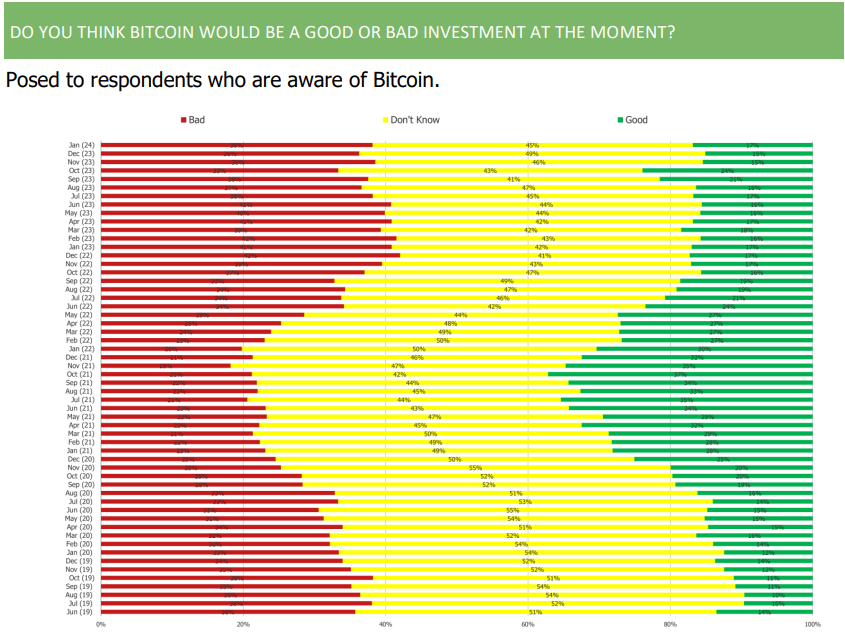

3. The share of respondents who believe that Bitcoin would be a bad investment increased q/q.

AI Chatbots | Top Three Takeaways

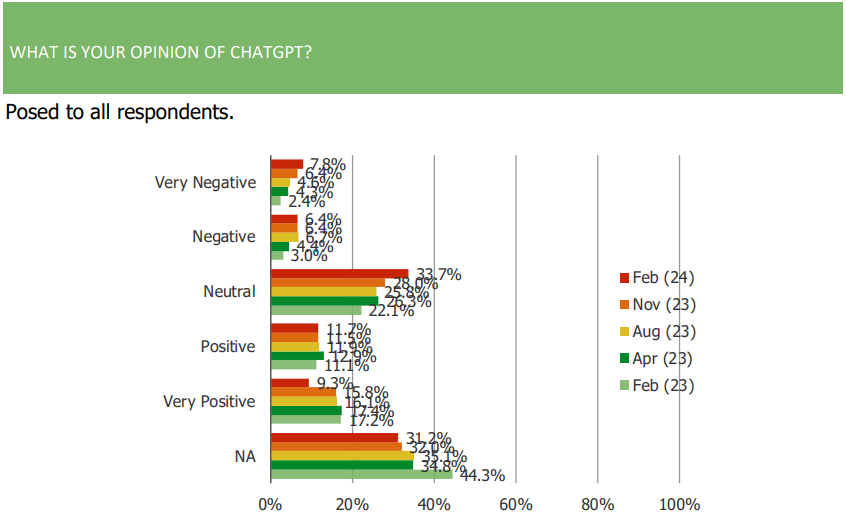

1. The share have consumers who have tried AI chatbots like ChatGPT has increased, but overall satisfaction/sentiment toward those offerings worsened q/q.

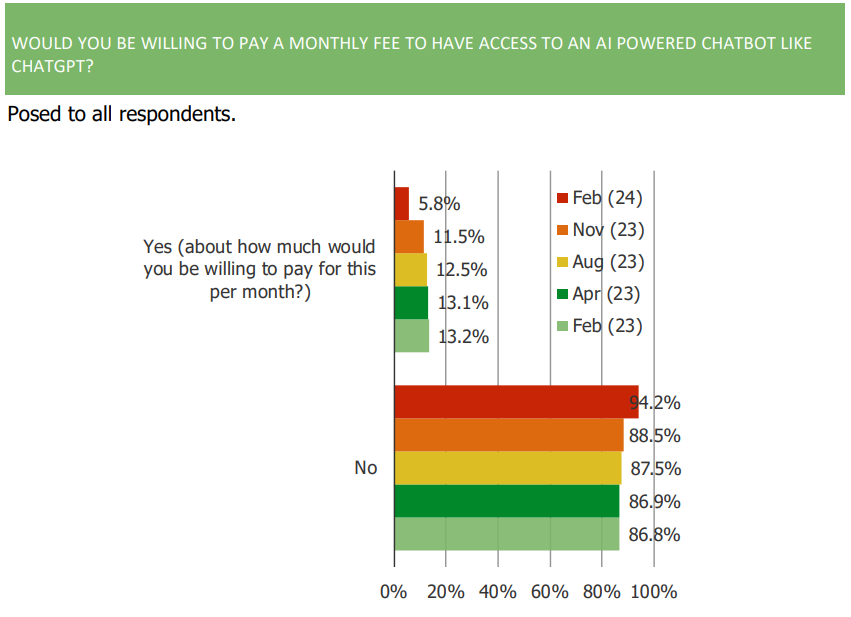

2. A decreasing number of respondents would pay a monthly fee for access to ChatGPT or other AI chatbots.

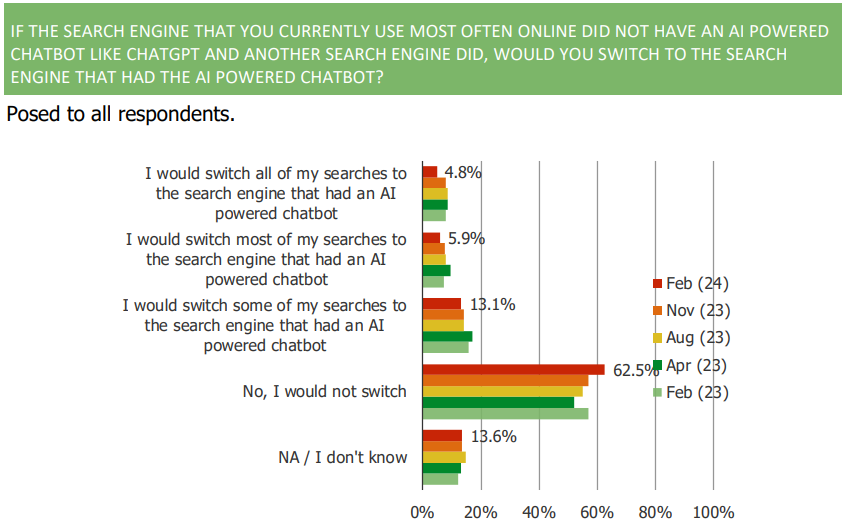

3. The majority of respondents would not switch from the search engine that they currently use, to one that has an AI powered chatbot.

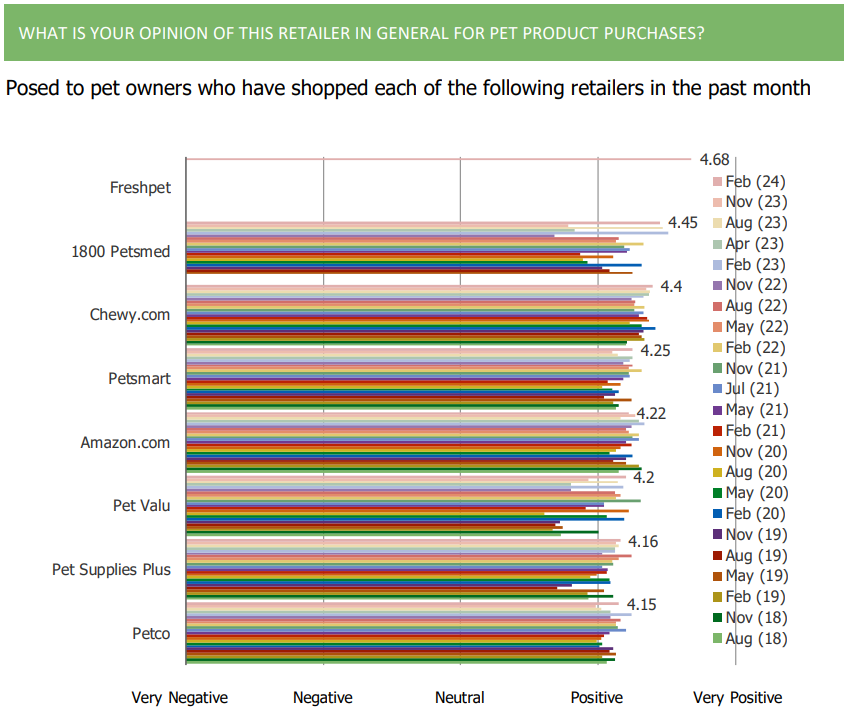

Pet Retail & Pet Health | Top Three Takeaways

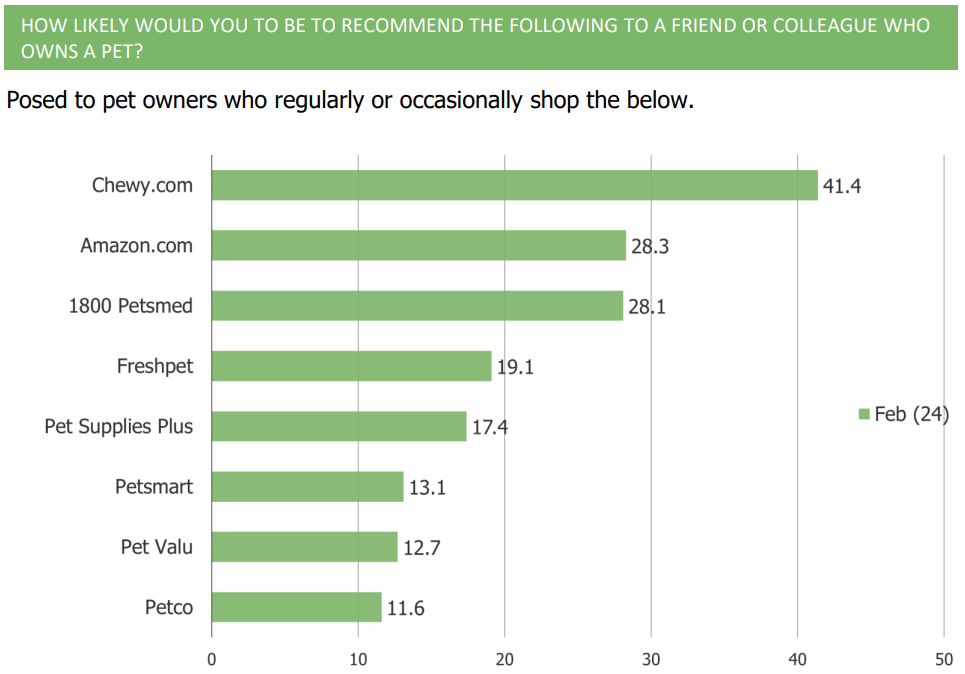

1. Chewy NPS came in at ~41, while Freshpet came in at ~19

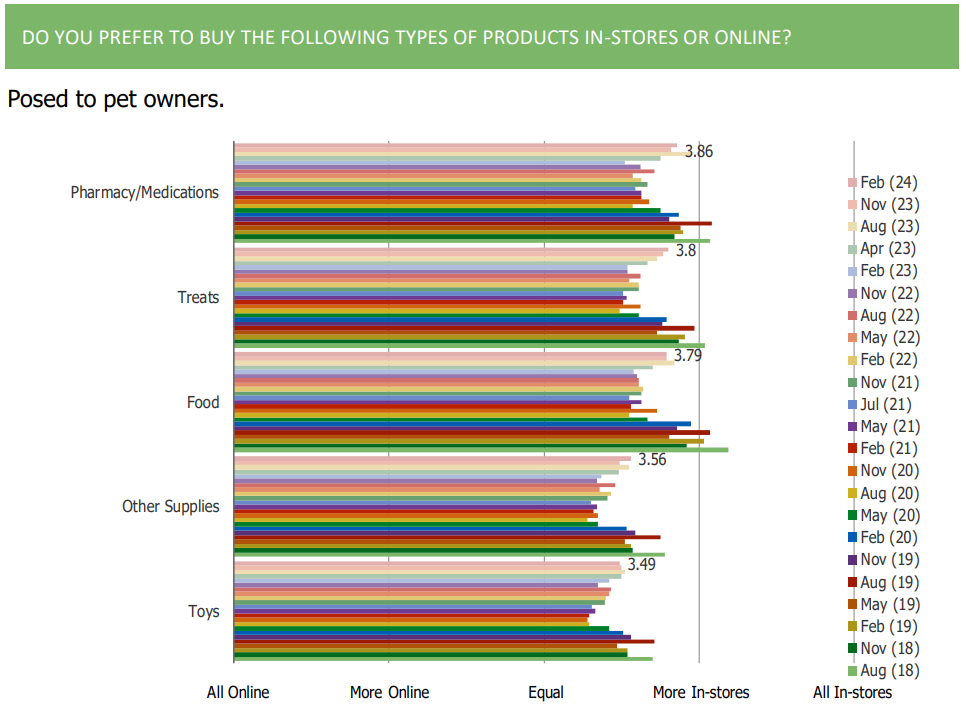

2. Pet owners shifted their shopping preferences in the direction of online buying during the pandemic quarters of our survey’s history. In the quarters following the pandemic, preferences have shifted a bit back in the direction of in-store.

3. Customer opinions of Freshpet are very positive and a touch stronger relative to Chewy, Petsmart, and Petco.