Blog

Bespoke Survey Insights

Plant Based Meat Alternatives | Top Three Takeaways

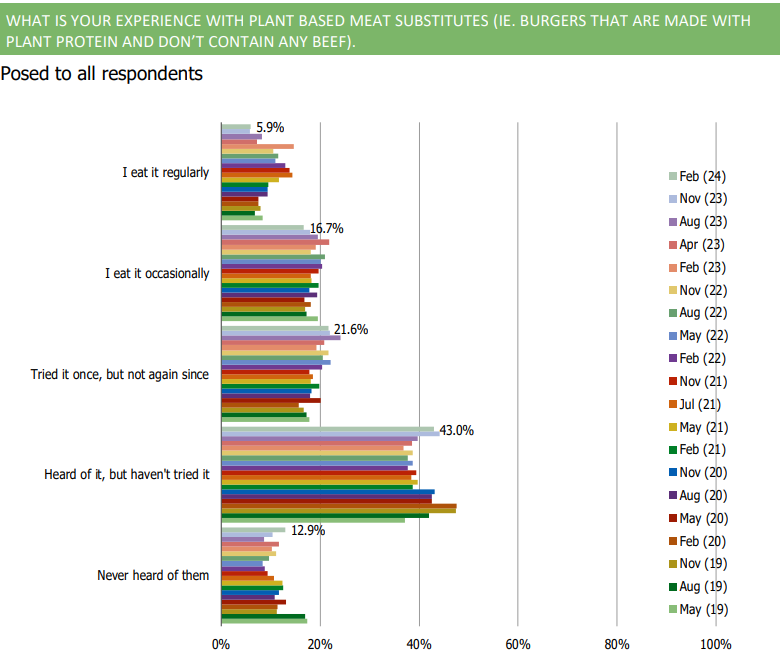

1. Self-reported plant based meat consumption continues to soften sequentially in our survey

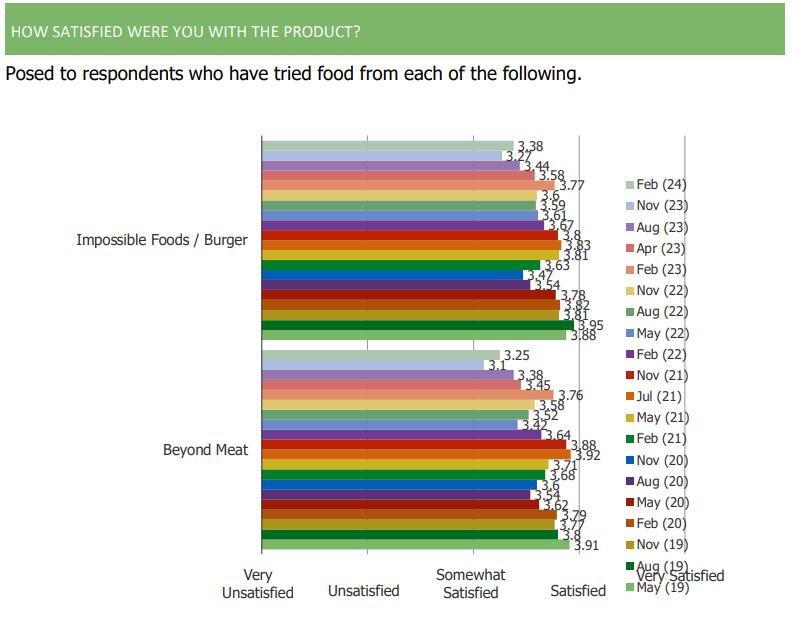

2. Among consumers who have tried plant-based meat products from brands like Impossible Foods and Beyond Meat, satisfaction with the products has worsened over the past 1-2 years.

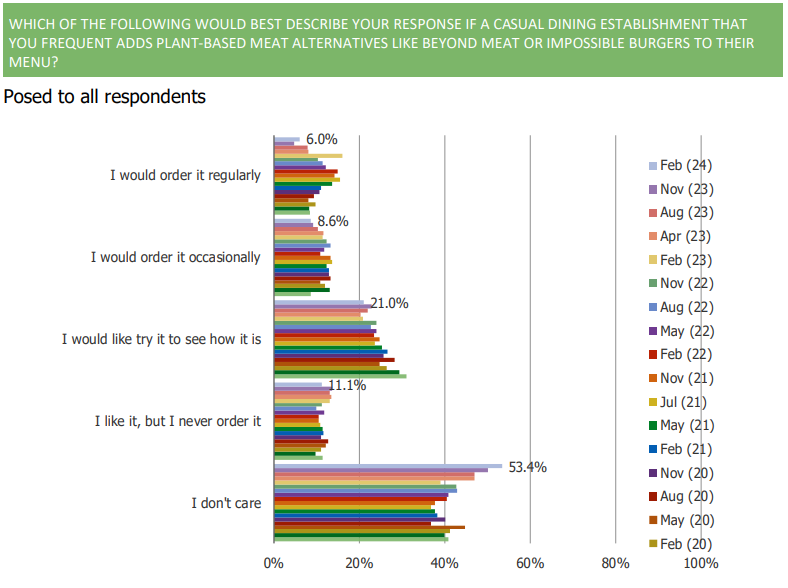

3. Consumers have grown increasingly apathetic as to whether restaurants that they frequent offer plant based meat alternatives.

Department Stores | Top Five Takeaways

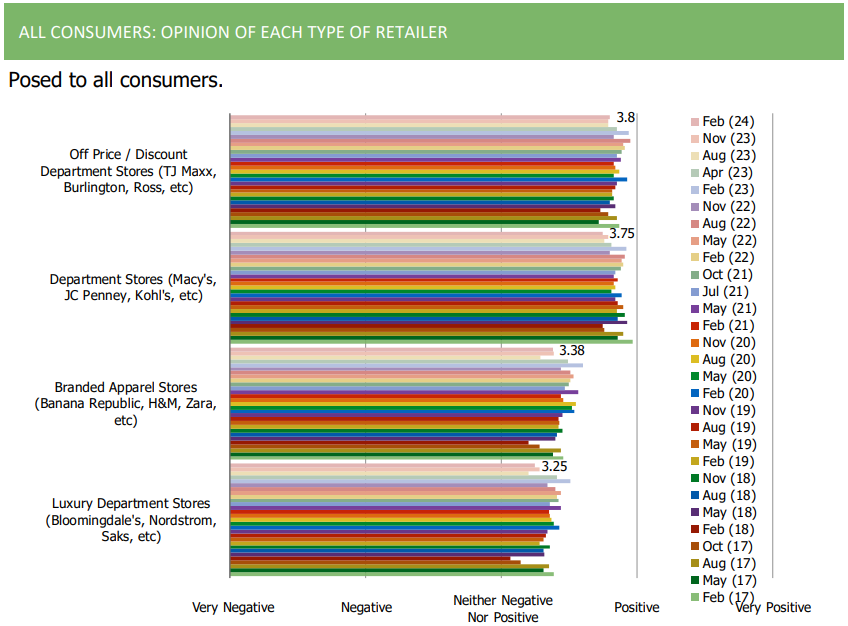

1. Consumer opinions of department stores and branded apparel retailers are net positive, but have softened a bit over the past year

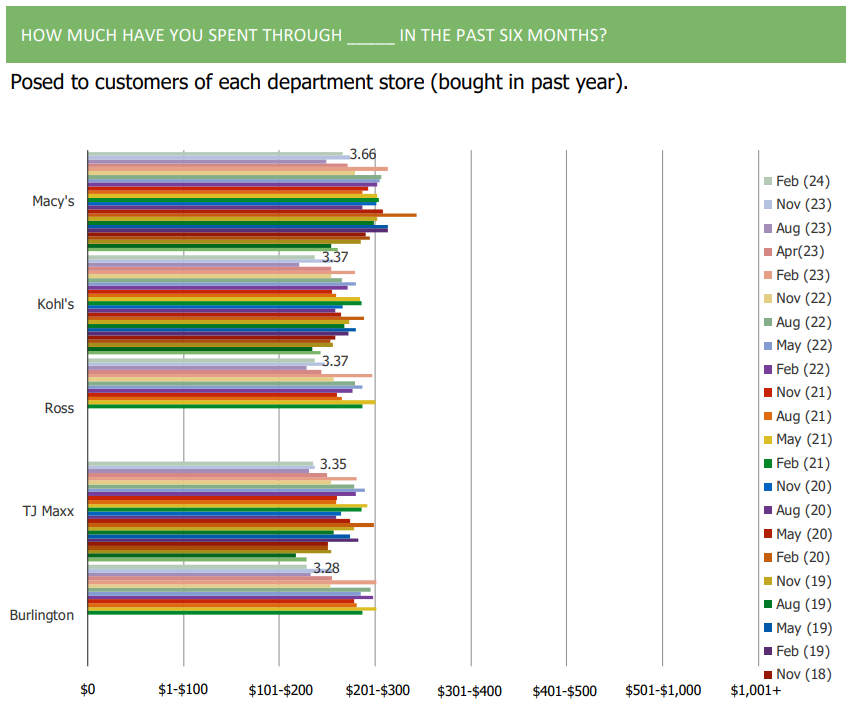

2. Across the department stores and off-price stores that we deep dive on, customer feedback around the amount of money they have spent at each over the past six months is stable q/q, but the longer term trend has been a softening on this front over the past year

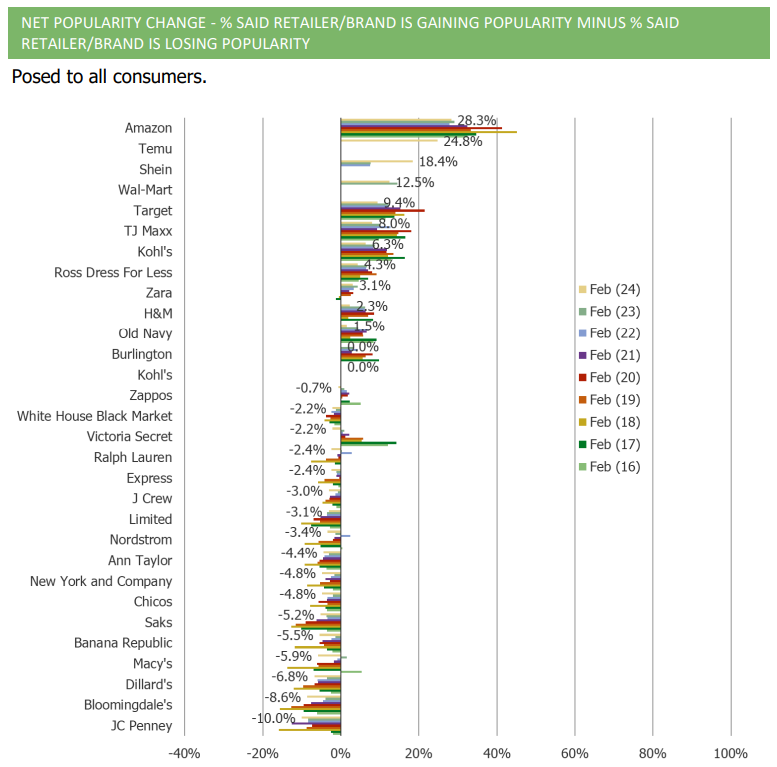

3. In our popularity change tracker, the retailers/etailers that are viewed as the largest net gainers in perceived popularity include Amazon, Temu, Shein, Wal-Mart, Target, TJ Maxx, Kohl’s, Ross, Zara, H&M and Old Navy.

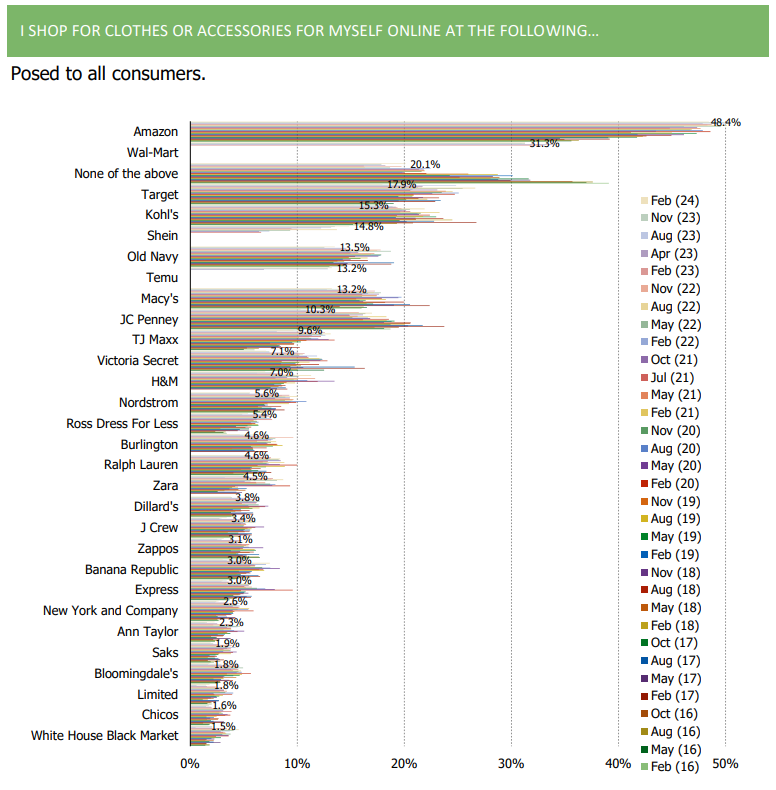

4. The share of consumers who shop Amazon for clothing has increased considerably throughout the history of our survey

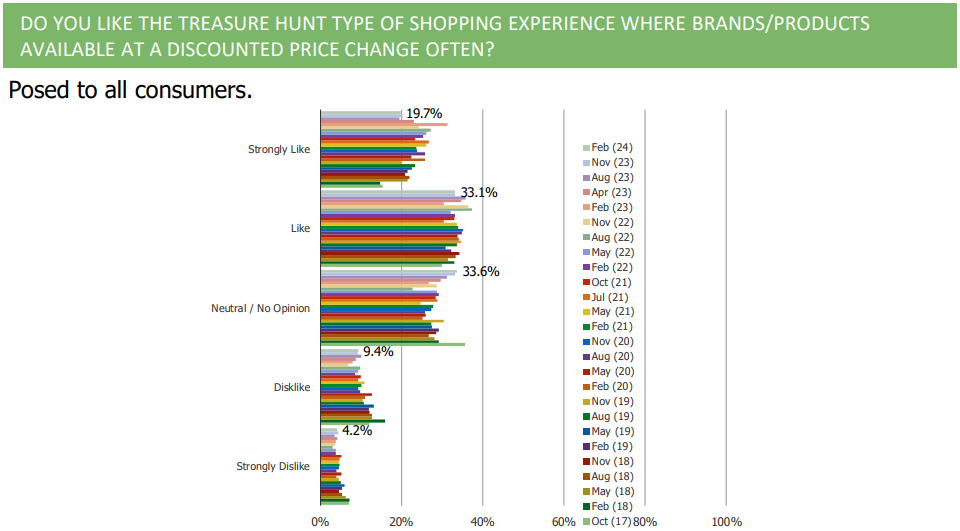

5. 52.8% of respondents like to strongly like the treasure hunt shopping experience

Low-Cost Retail | Top Five Takeaways

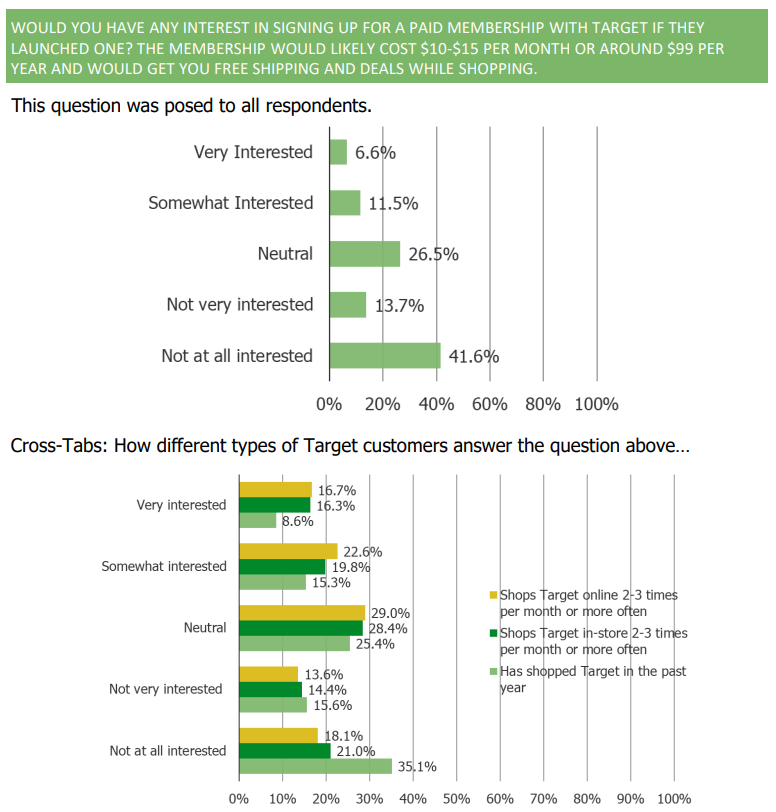

1. Projected interest in a potential/rumored paid membership program through Target is relatively low among the broader population, but ~35% of folks who shop Target 2-3+ times per month indicate being a range of somewhat to very interested.

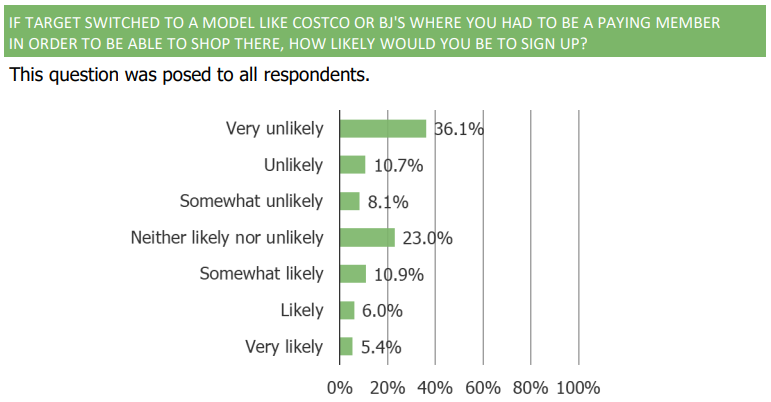

2. If Target were to pursue a Costco or BJ’s model with their “Project Trident” membership, they would find fewer customers interested in paying up compared to if they pursued an Amazon / Walmart + type program.

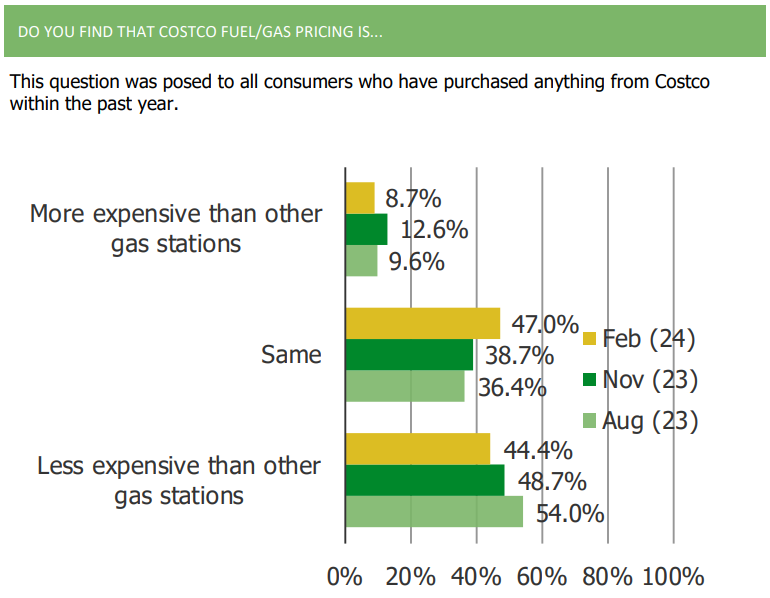

3. Costco customers continue to note that Costco fuel prices are lower relative to other gas stations, but the share has declined q/q since we started asking the question.

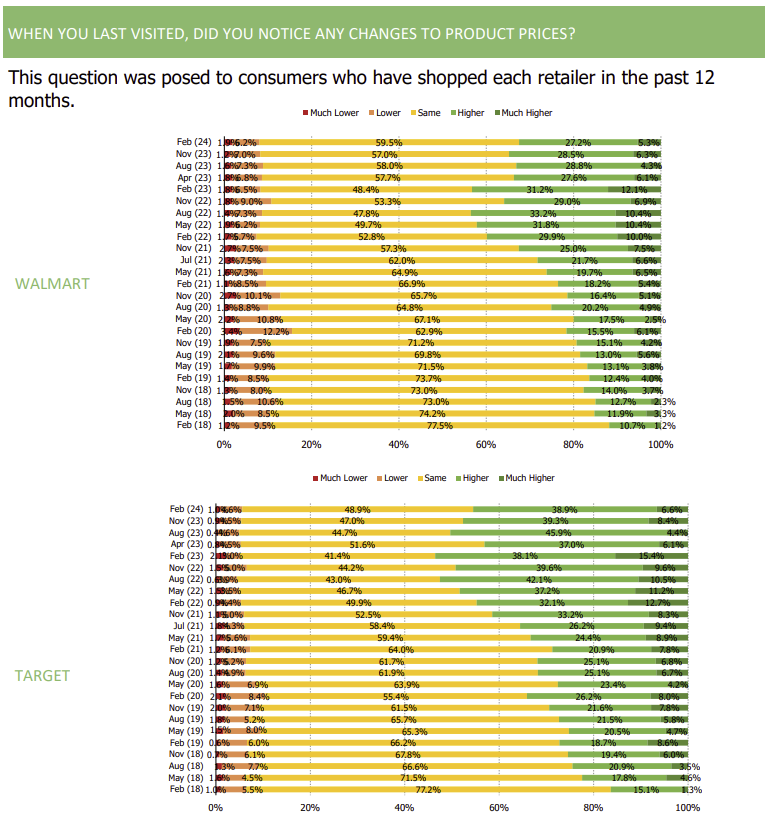

4. The share of Walmart and Target customers who flag higher prices continues to decline relative to the peak.

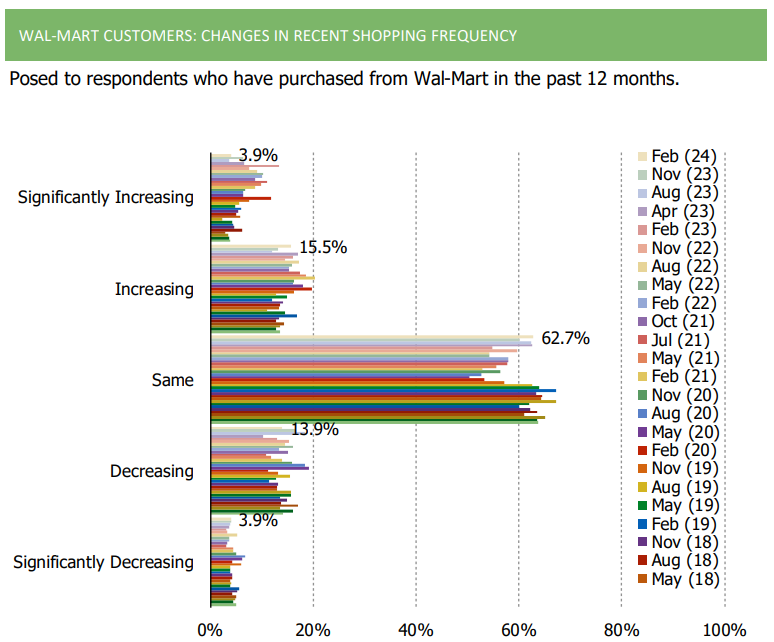

5. Self-reported Wal-Mart shopping trends have been fairly stable over time in our quarterly survey.

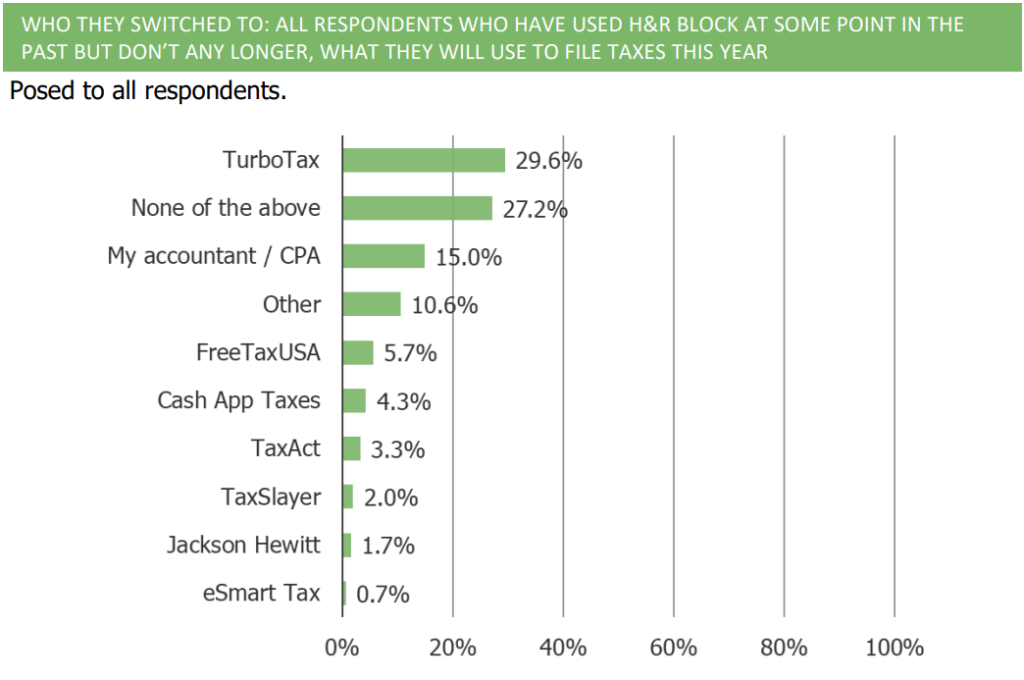

Tax Preparation Services | Top Three Takeaways

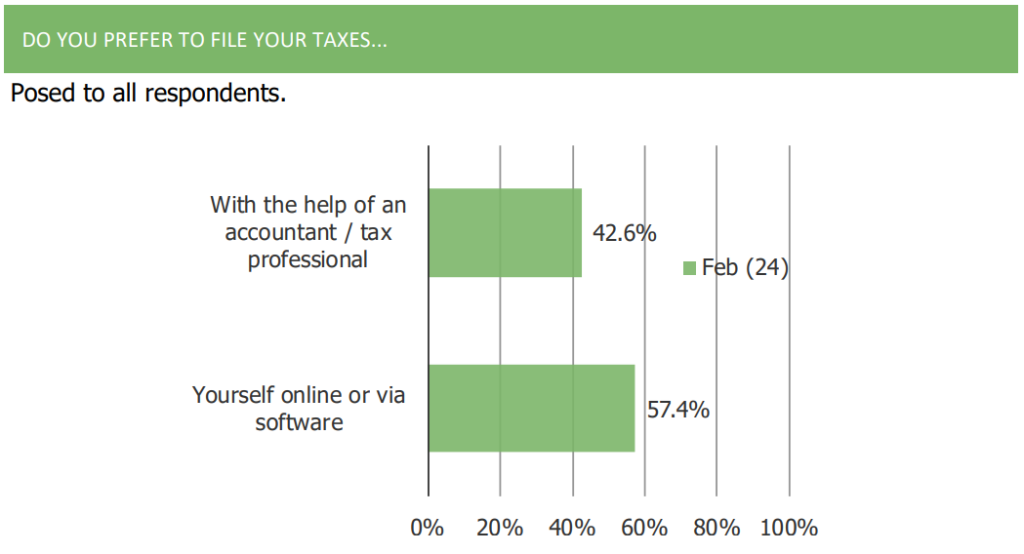

1. Respondents prefer filing their taxes online or via software over using the help of an accountant/tax professional.

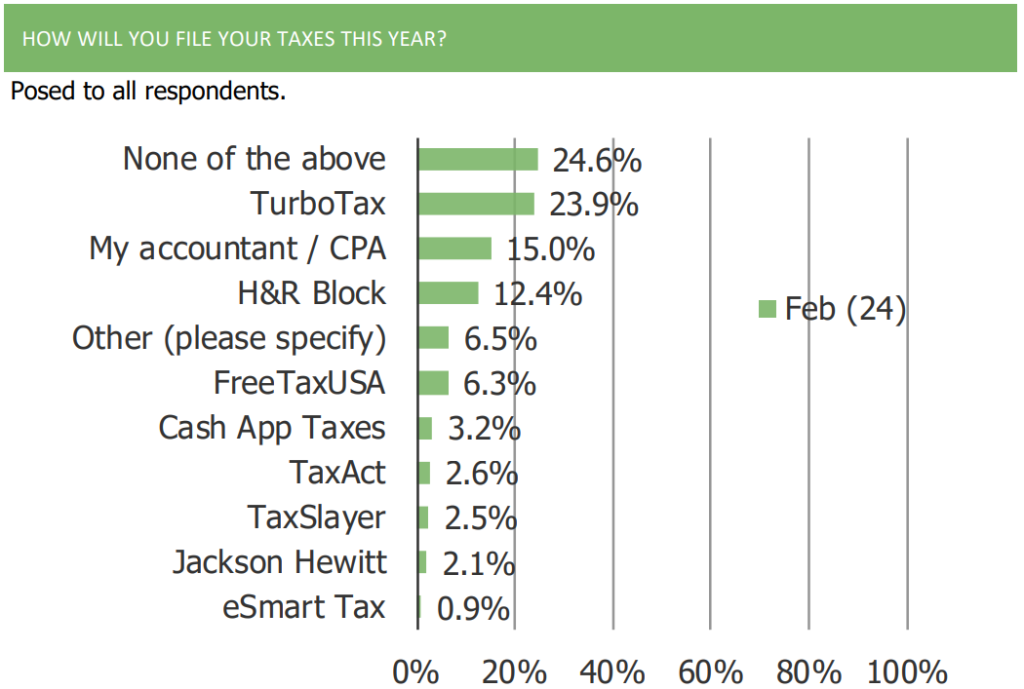

2. Of the options provided to respondents, TurboTax was the most popular option for filing taxes.

3. Of respondents who have used H&R Block in the past, a plurality (29.6%) have switched to TurboTax.

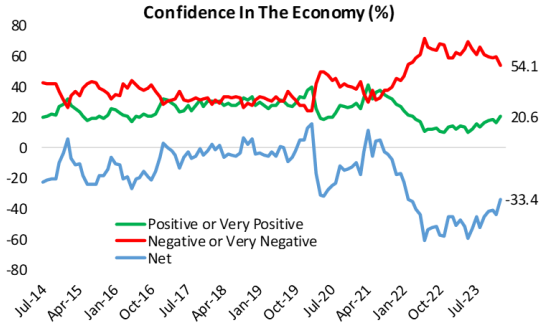

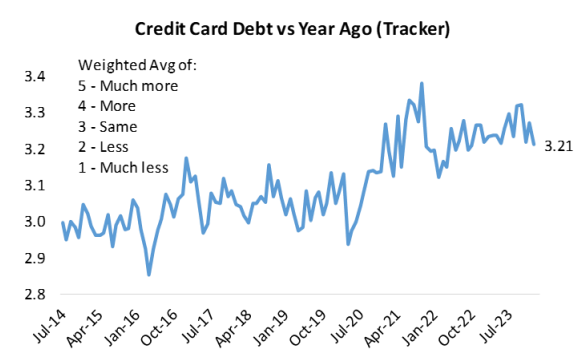

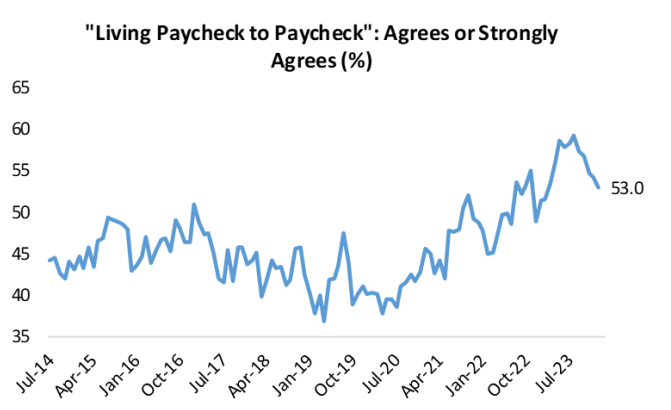

Macro Outlook | Top Five Takeaways

1. Consumer confidence in the economy has risen to the highest level in two years.

2. Respondents report credit card debt growing at a much faster rate than pre-pandemic norms.

3. The share of respondents living paycheck to paycheck has hit 11-month lows.

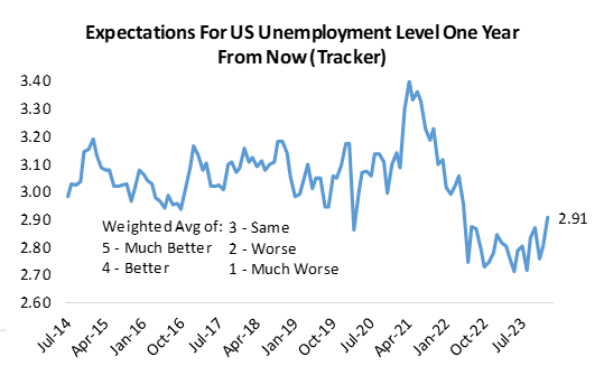

4. Consumers have become more optimistic on their outlook of the national labor market.

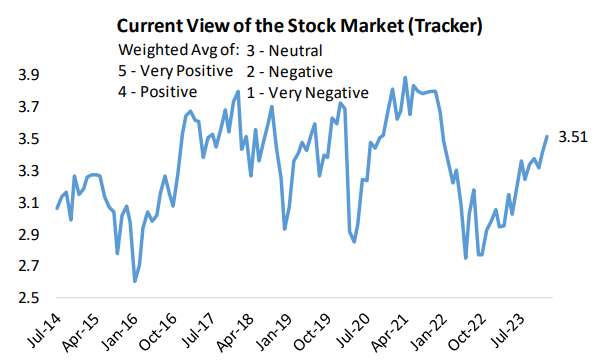

5. Consumer’s views of the stock market have risen sharply in recent months.

ROKU | Top Five Takeaways

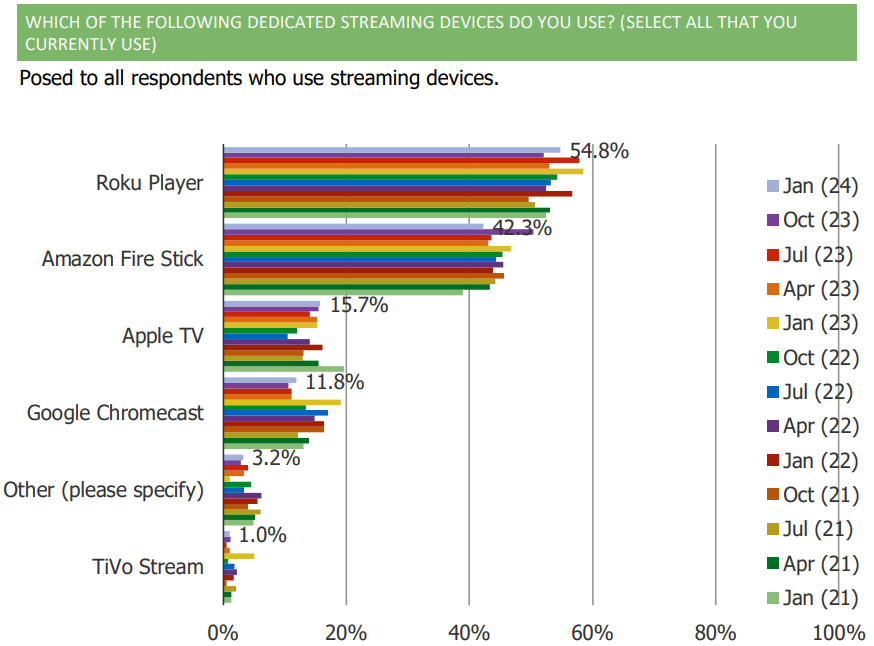

1. Roku remains the market share leader when it comes to dedicated streaming devices that consumers use. Roku leads Amazon Fire Stick and Apple TV.

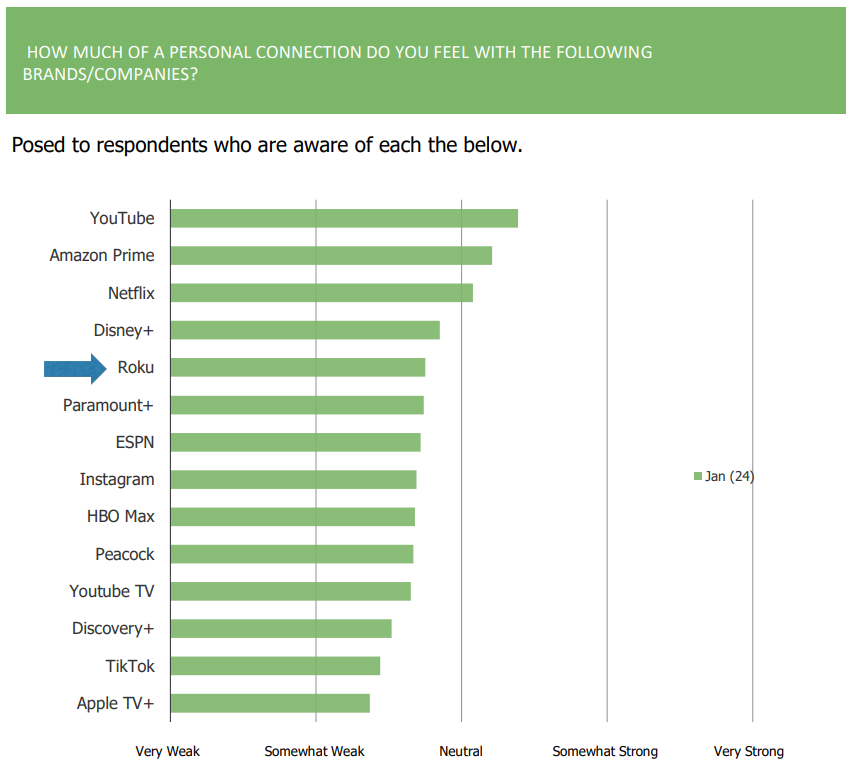

2. Consumers have a relatively strong level of connection to the Roku brand, on an absolute basis and relative to peers.

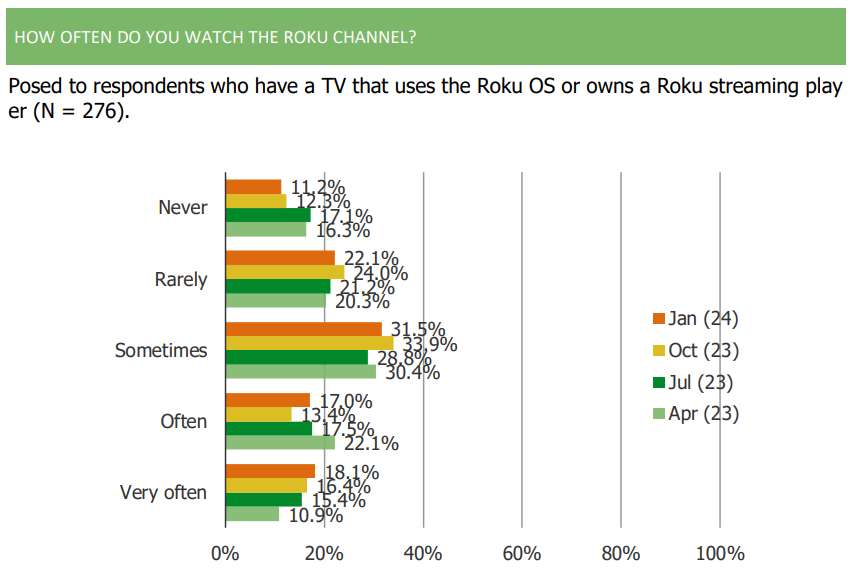

3. The share of Roku users who watch the Roku channel has increased sequentially.

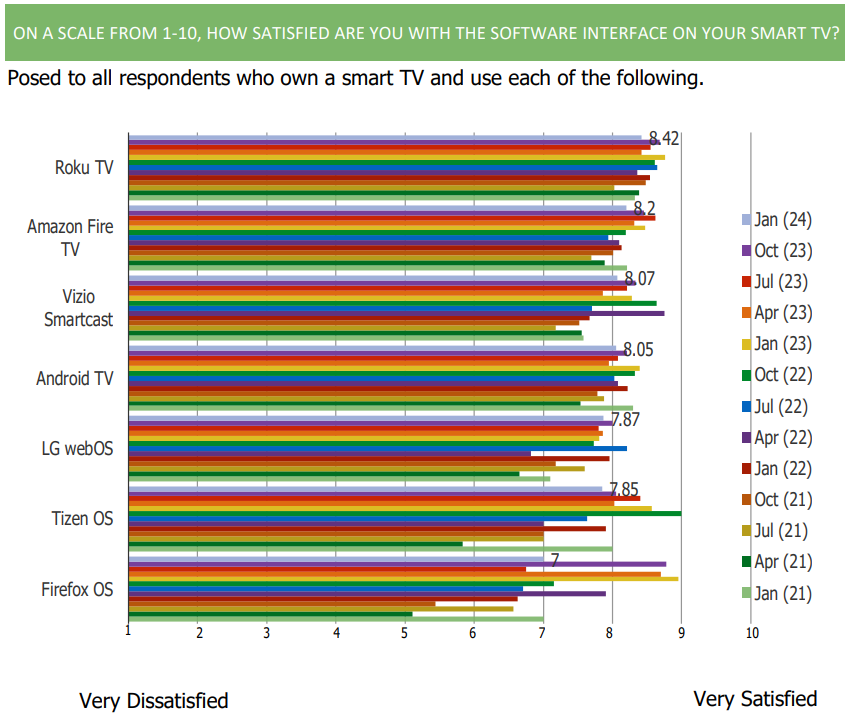

4. Consumer satisfaction with the Roku TV software interface remains high. Roku leads key competitors on this front.

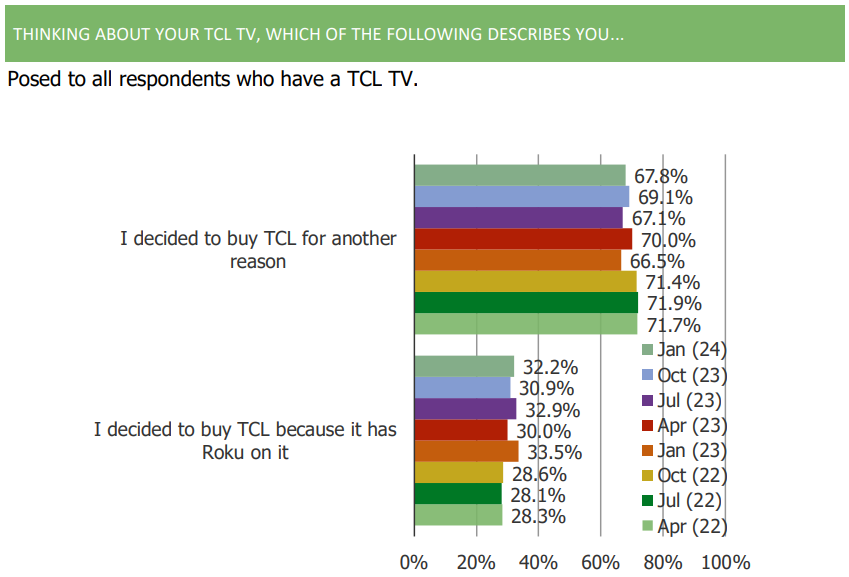

5. 32.2% of TCL owners said that they bought a TCL TV primarily because it had Roku TV on it.

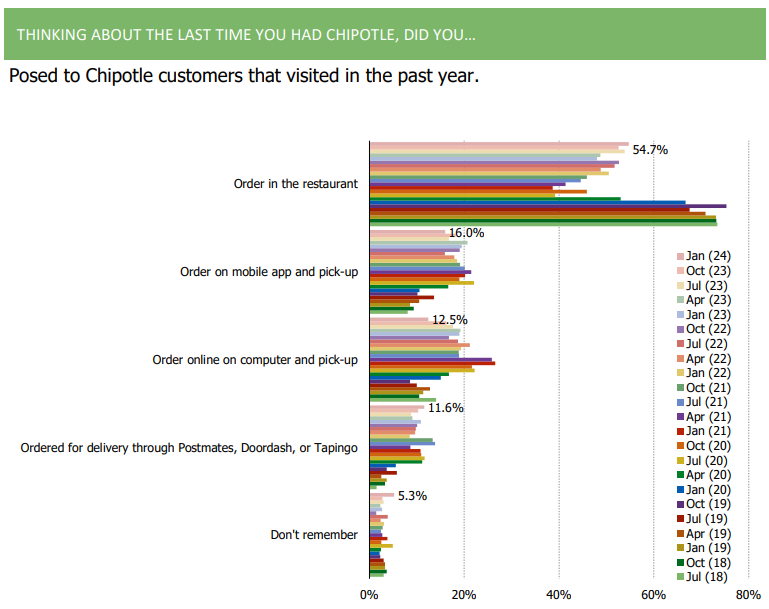

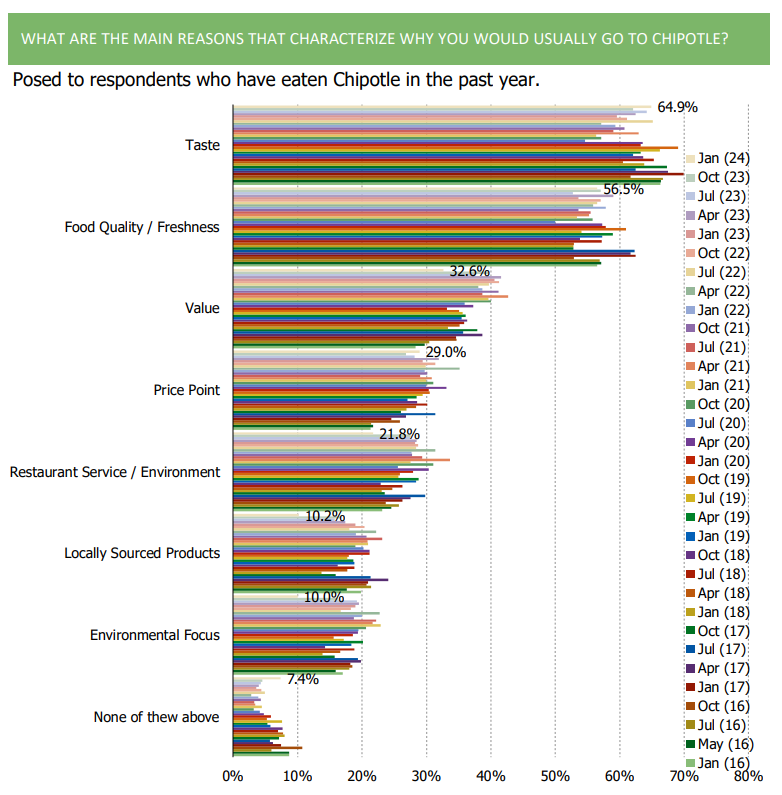

Chipotle (CMG) | Top Three Takeaways

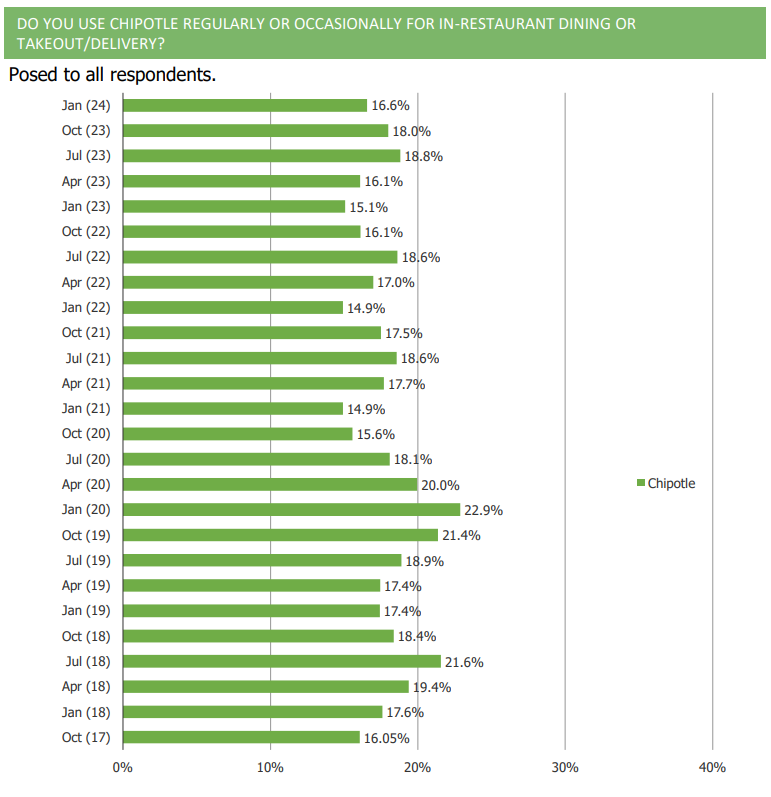

1. The share of consumers who self-report eating Chipotle regularly or occasionally has declined q/q.

2. In store orders have rebounded in the last few quarters, while mobile orders have declined as of late.

3. Taste and quality remain the top reasons why consumers frequent Chipotle.

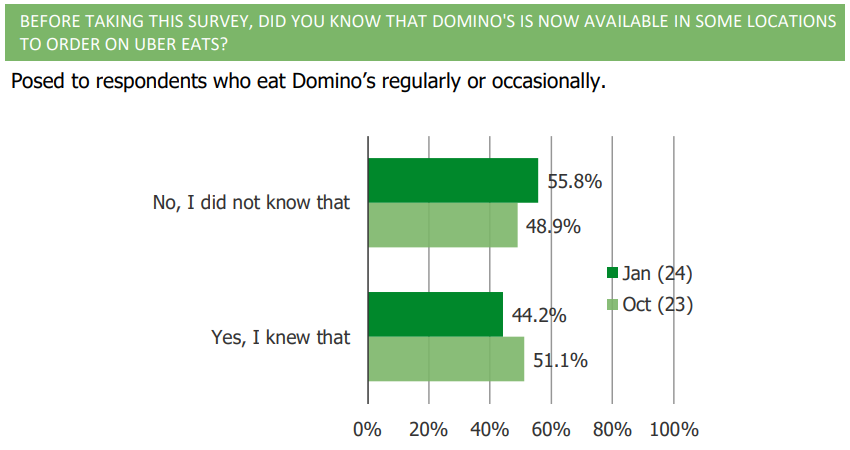

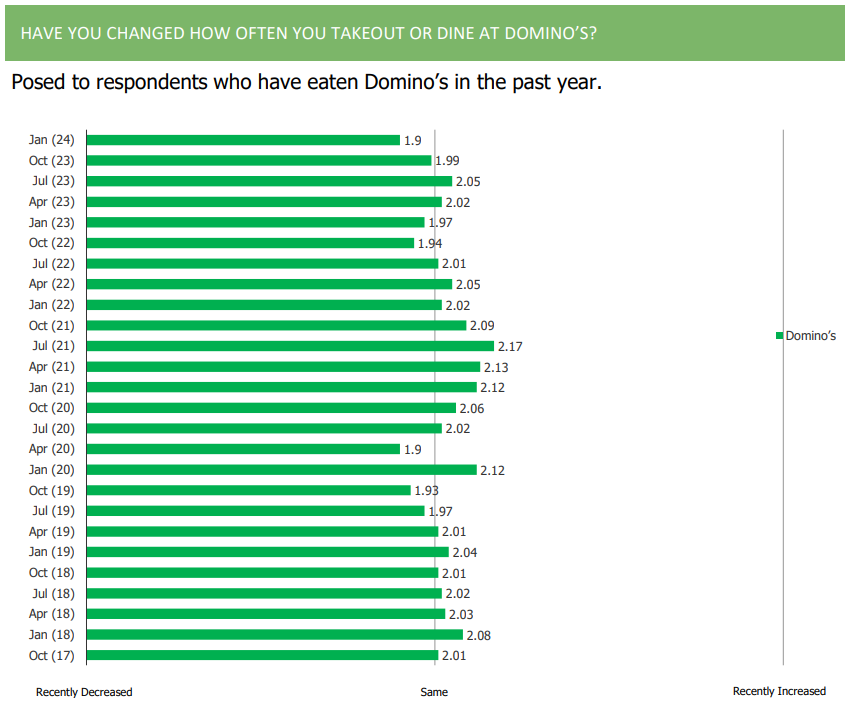

Domino’s | Three Takeaways

1. Awareness of the availability of Domino’s on Uber Eats has declined q/q.

2. Like we have observed for other casual dining platforms in our surveys, feedback around engagement is softer sequentially for DPZ.

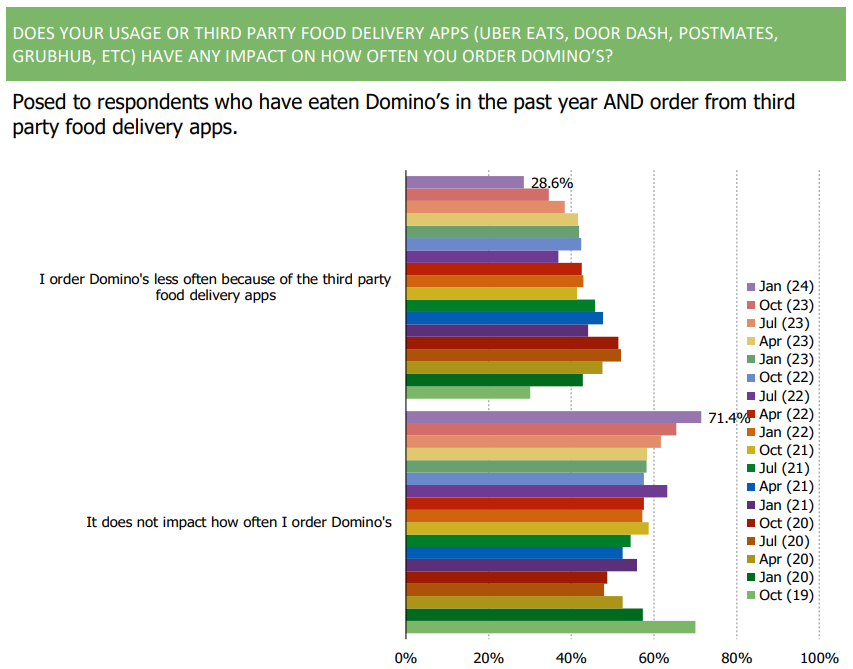

3. The share of consumers who say their usage of third party food delivery apps impacts their usage negatively continues to decline and reached a new series low this quarter.

Consumer Electronics China | Top Three Takeaways

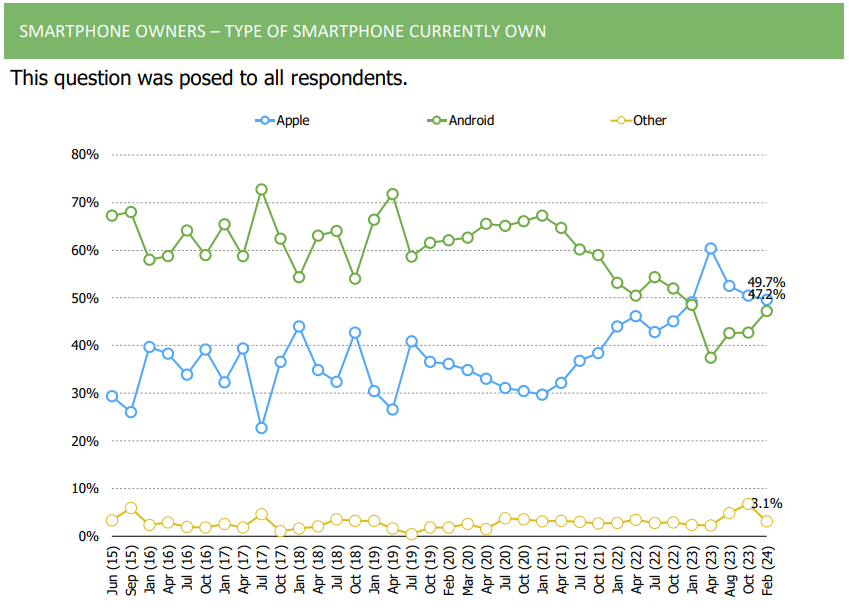

1. The share of iPhone users has continued to decline over the past few waves, but still leads Android slightly in our trackers

2. Price/cost remains one of the top reasons as to why Chinese consumers own less iPhones.

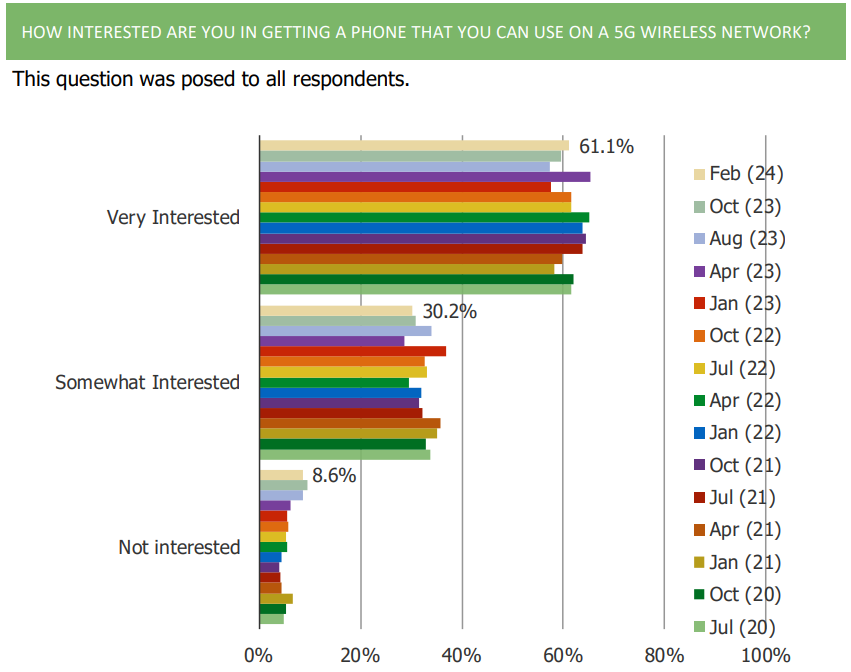

3. 61.1% of respondents noted that they are very interested in owning a smartphone that works with 5G.

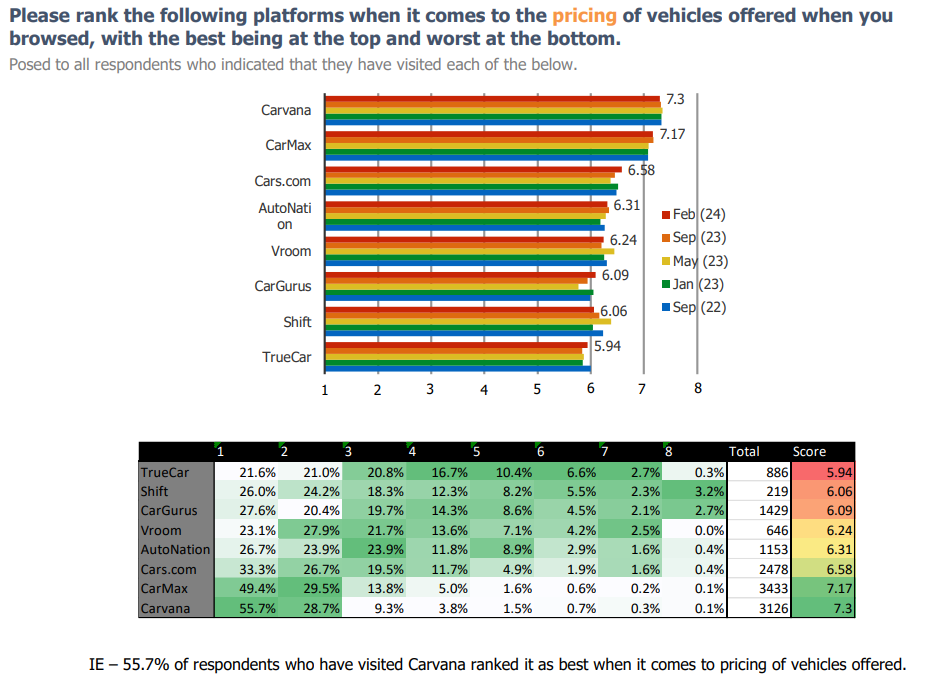

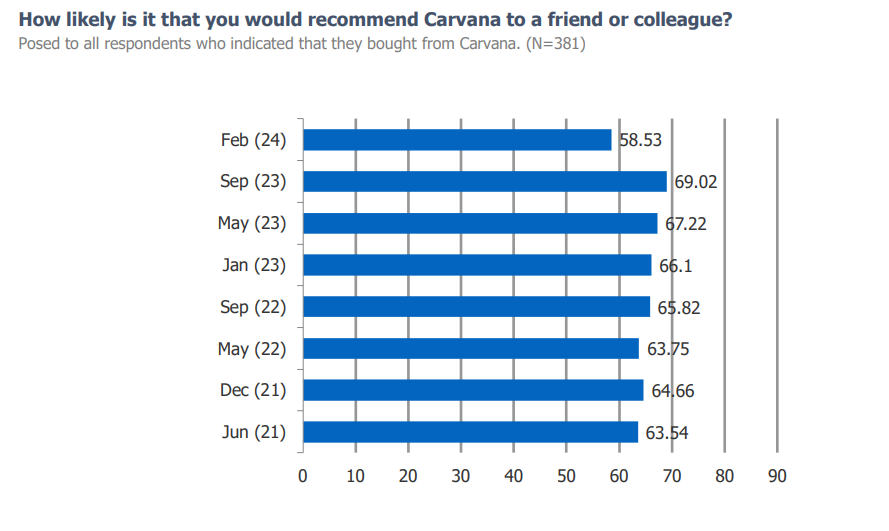

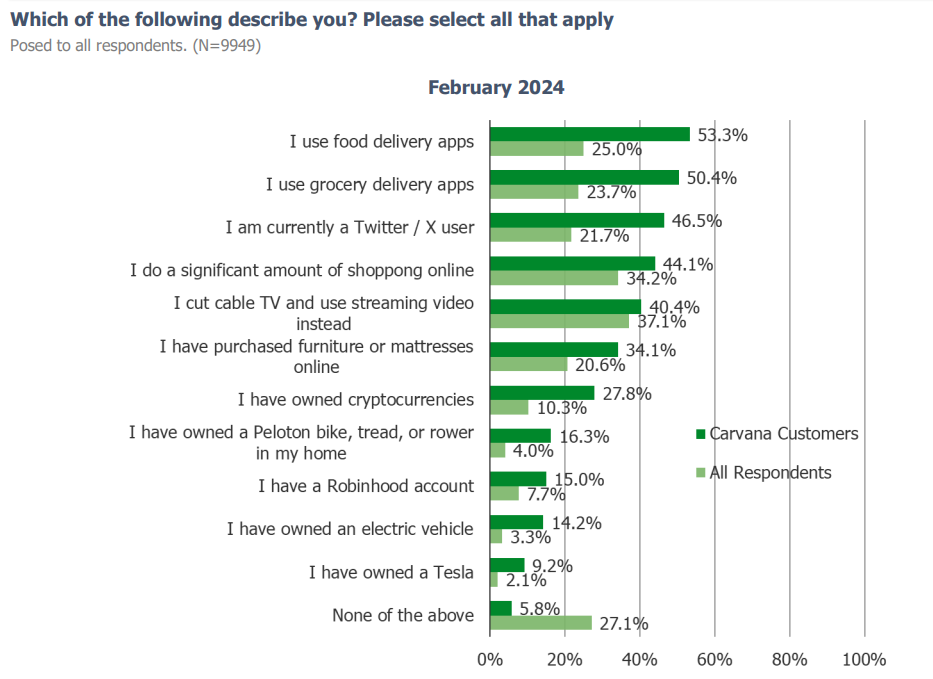

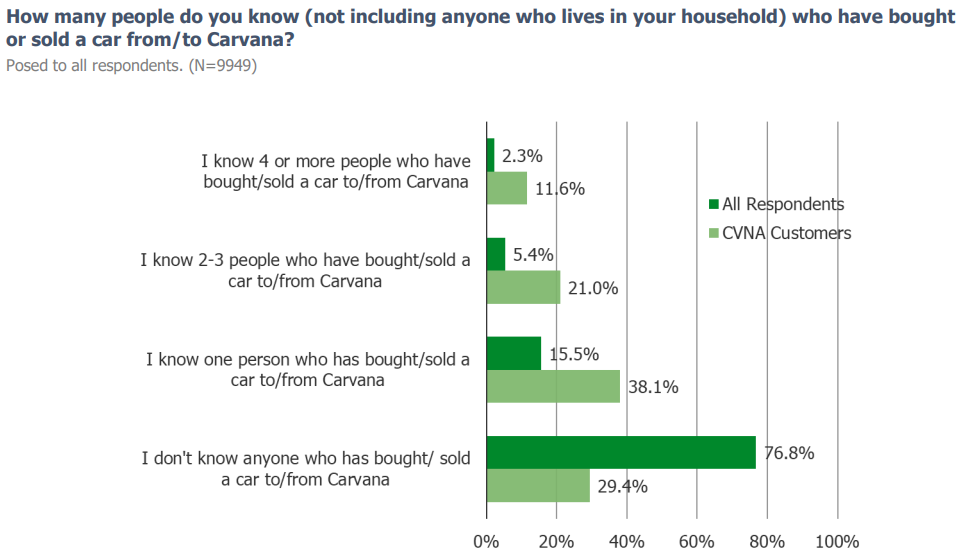

Carvana | Top Five Takeaways

1. Among those who have visited each online auto platform in our survey, Carvana ranks at the top when it comes to price and selection.

2. NPS for Carvana remains very strong but is slightly weaker this wave compared to last. Observing fluctuations in NPS for a platform like Carvana is not uncommon given the later adopter dynamic that unfolds over time.

3. Carvana customers over-index as early adopters of disruptive technologies.

4. Most respondents who have purchased a vehicle from Carvana reported knowing at least one person who has bought or sold a car to Carvana.

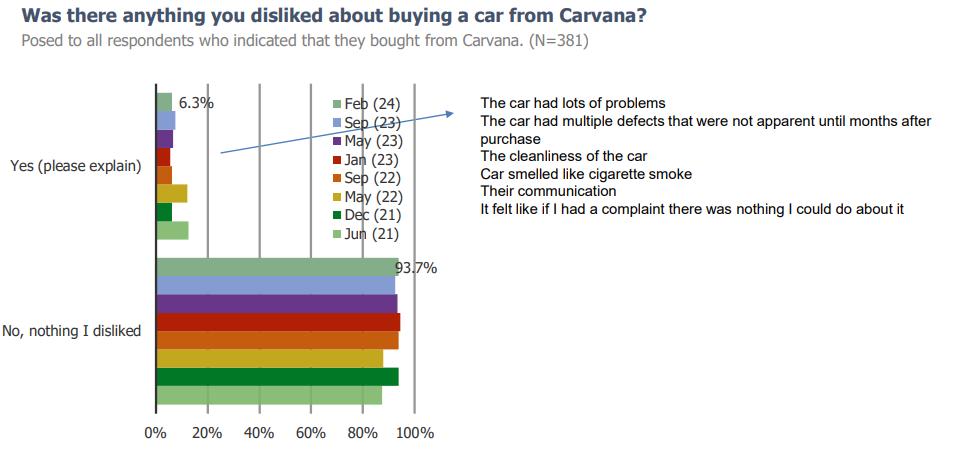

5. Overall, the feedback from Carvana customers remains positive. Customers love the convenience and ease of the platform above all else. Other customers mentioned liking the price and customer service. 90+% of customers consistently tell us that there was nothing that they disliked about buying a car from Carvana.

Consumer Rage & Love | Top Three Takeaways

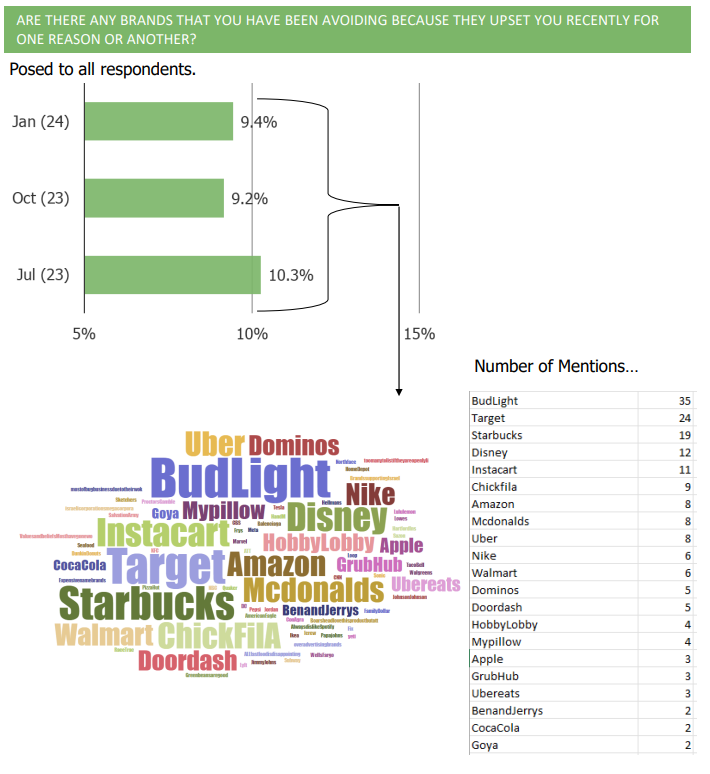

1. Around 10% of respondents report that they are avoiding one or more brands because they are upset with them for one reason or another. Top brands mentioned on this front include Bud Light, Target, Starbucks, Disney, and Instacart.

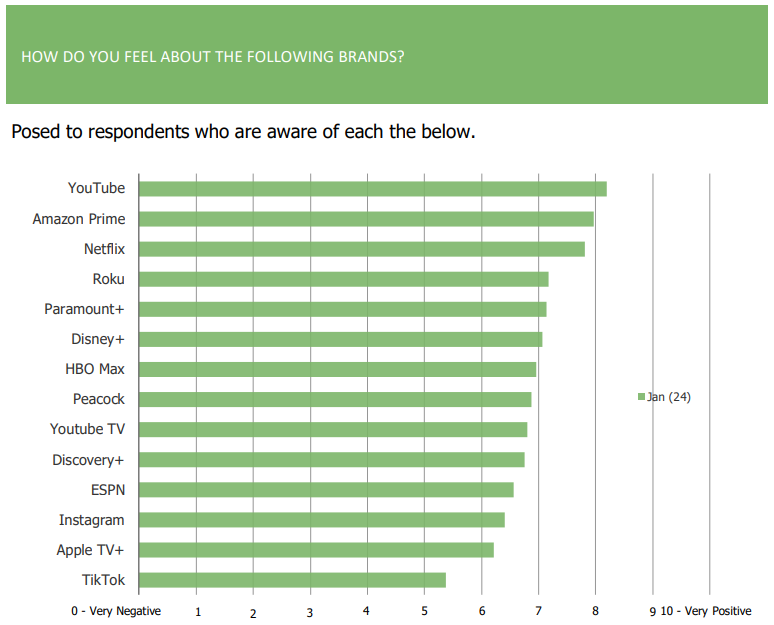

2. Brands that stood out as having very strong ties to those who are either aware of or active users of each platform include YouTube, Amazon, Netflix, and Roku.

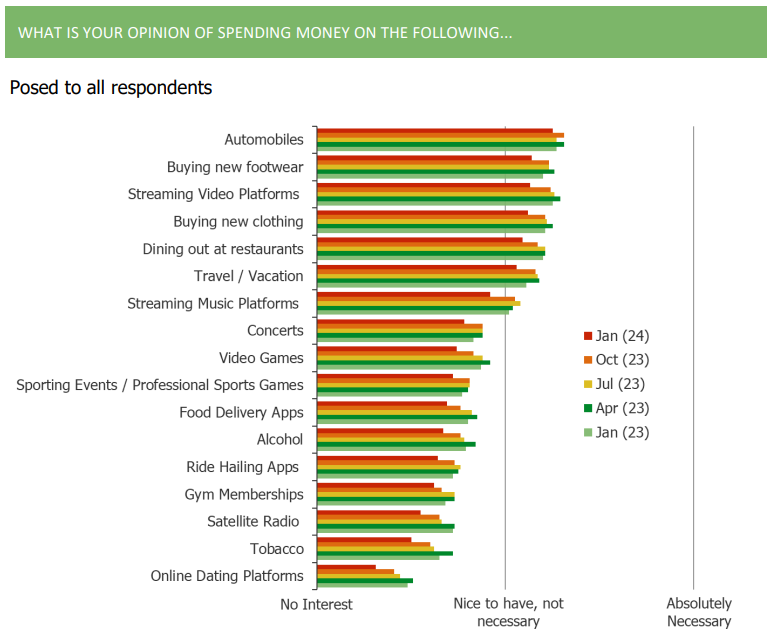

3. Consumers pulled back slightly in our January wave in their opinion of spending money across discretionary categories that we ask about.

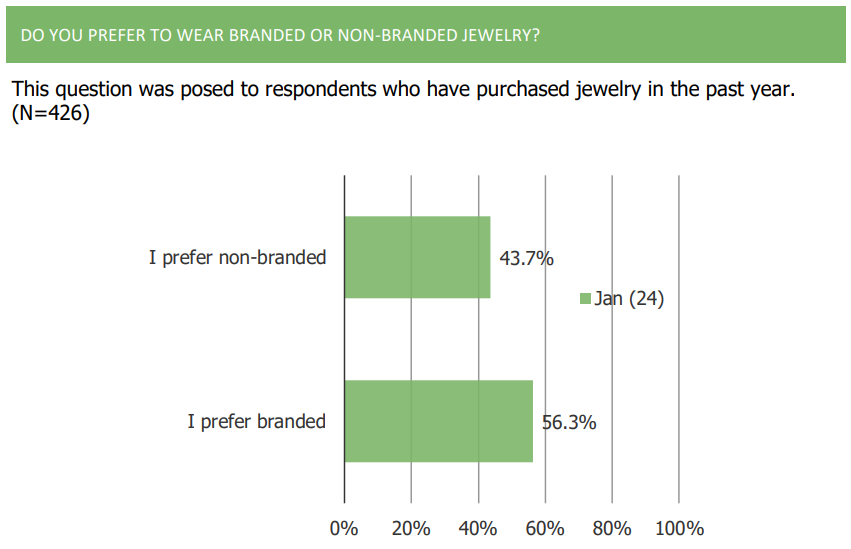

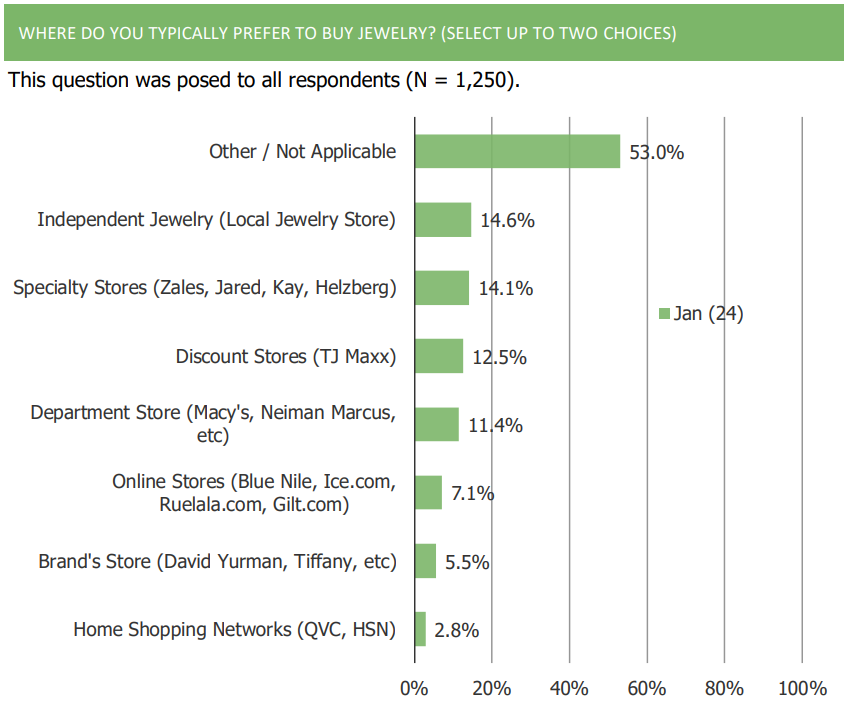

Jewelry | Top Three Takeaways

1. Consumers note that they primarily turn to independent jewelry and specialty stores to purchase jewelry.

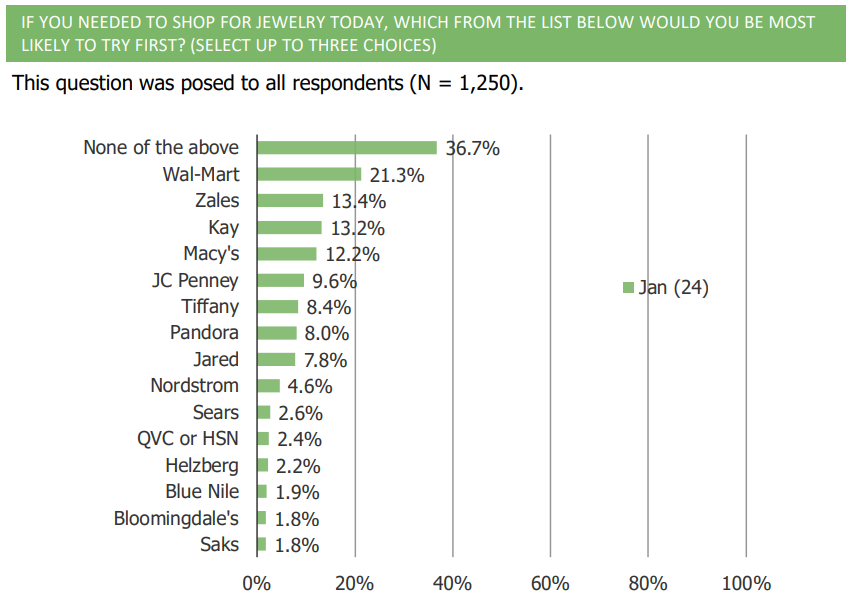

2. If they needed to purchase jewelry today, consumers indicate that they would turn to Zales and Kay. Pandora fell more middle of the pack based on our tracker.

3. A majority of consumer prefer branded jewelry over non-branded.