Blog

Bespoke Survey Insights

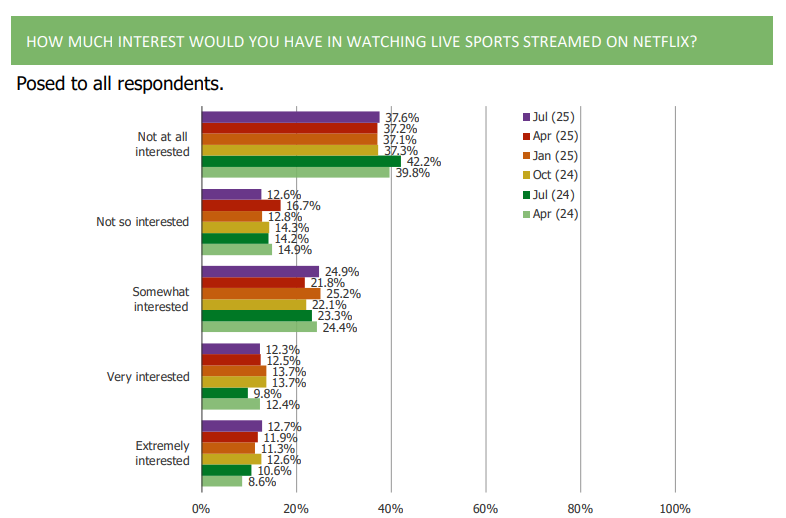

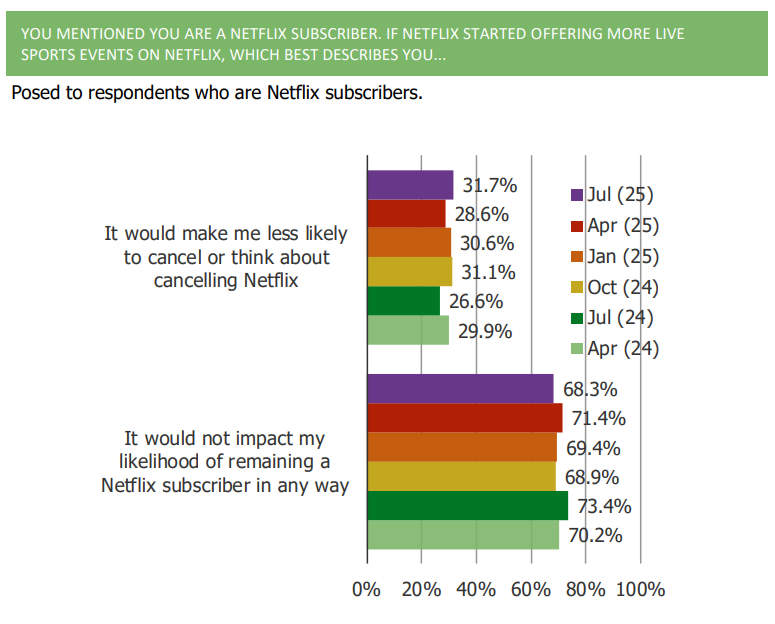

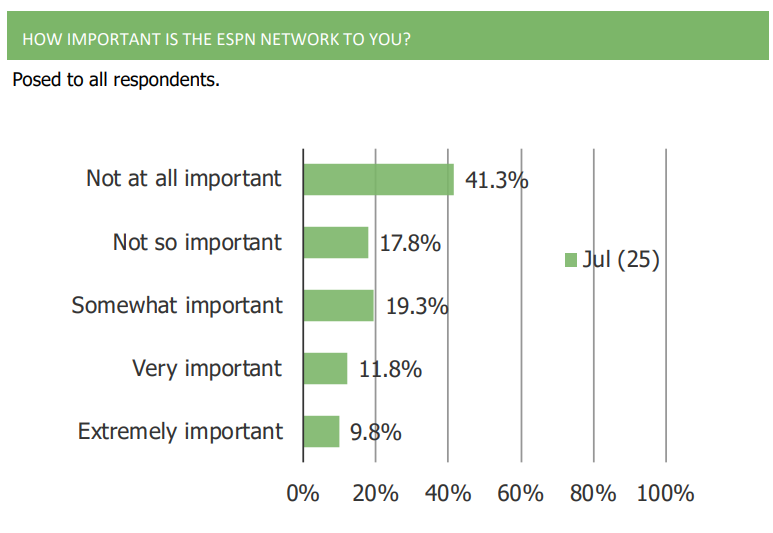

Streaming and Live Sports

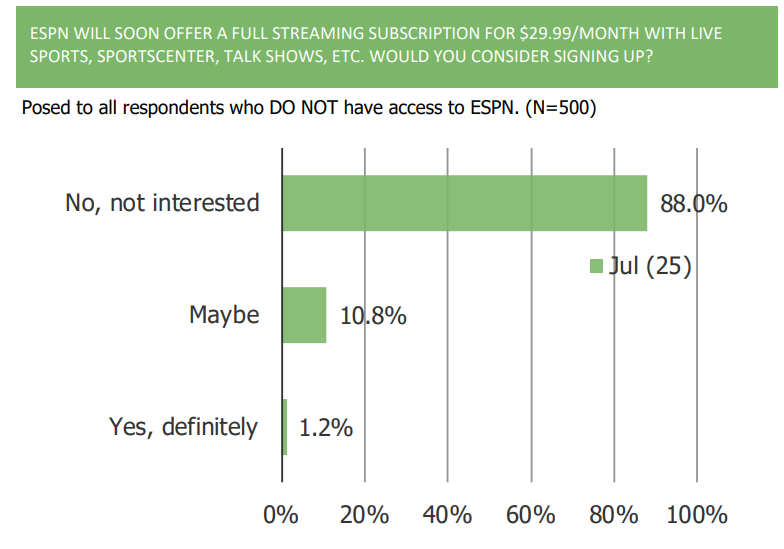

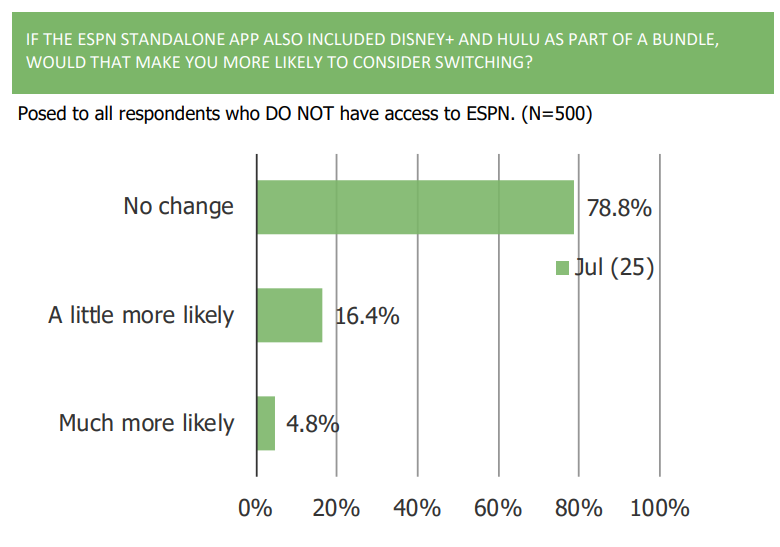

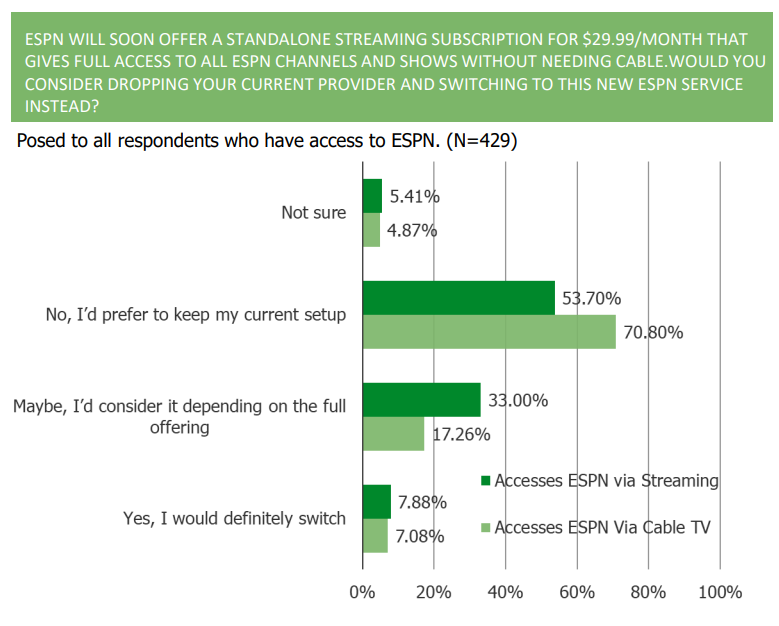

New ESPN Subscription Offering

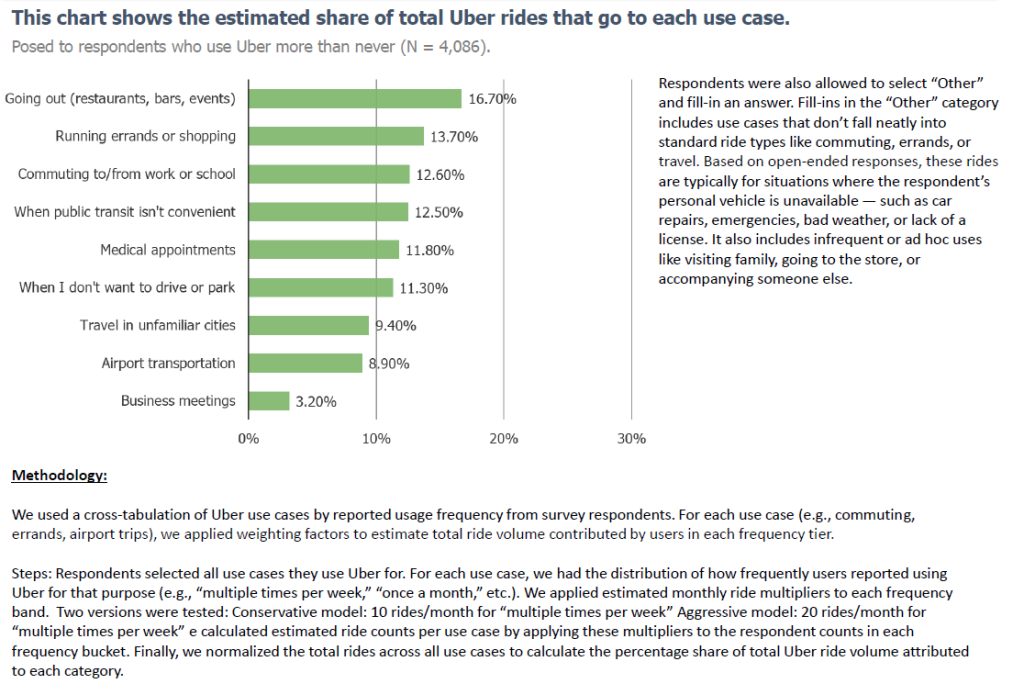

UBER Use Cases

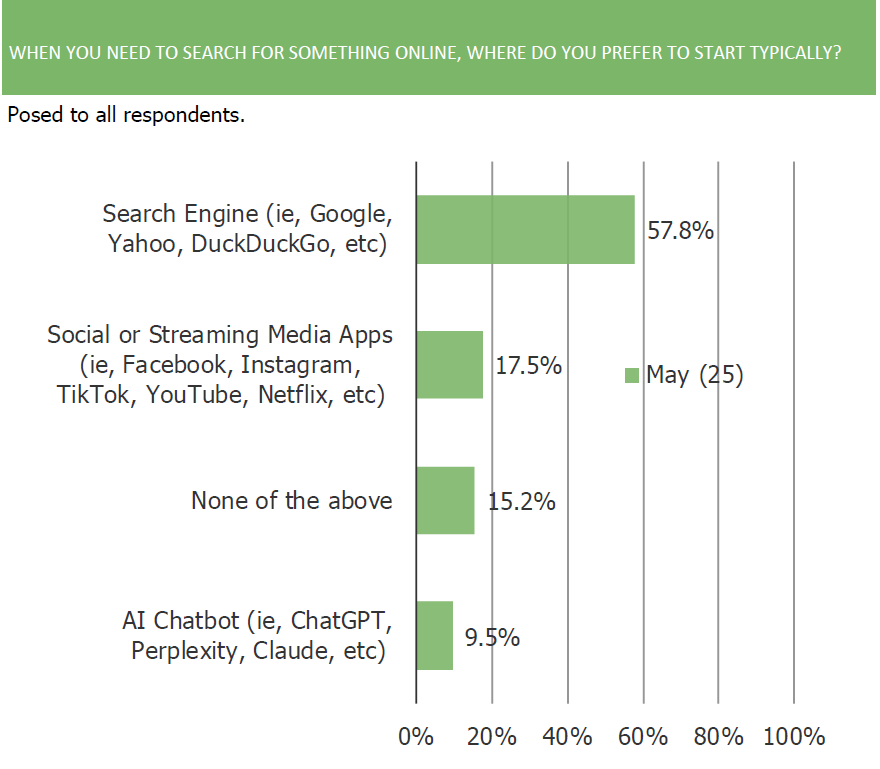

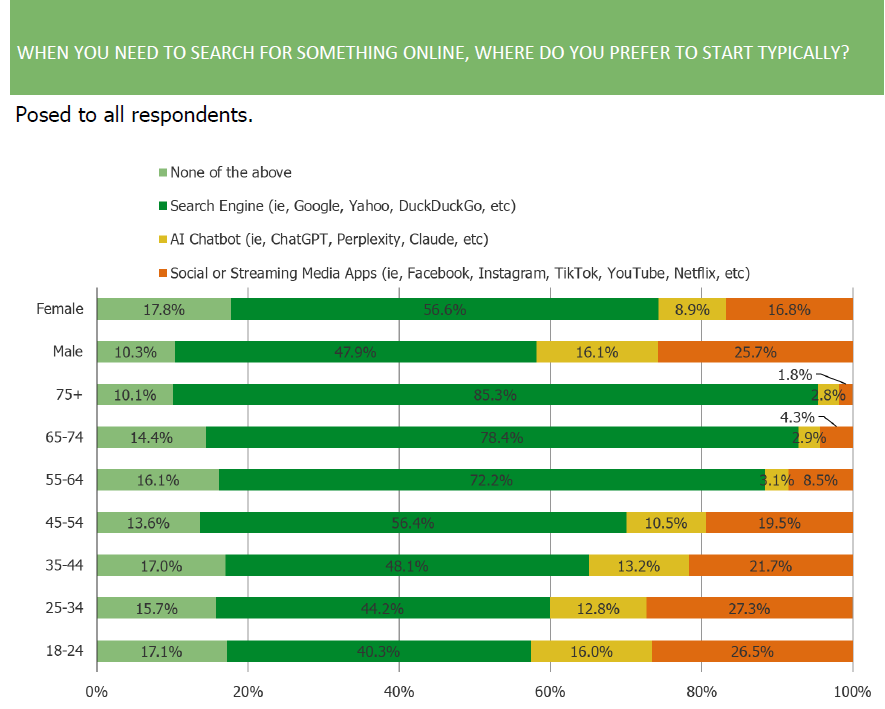

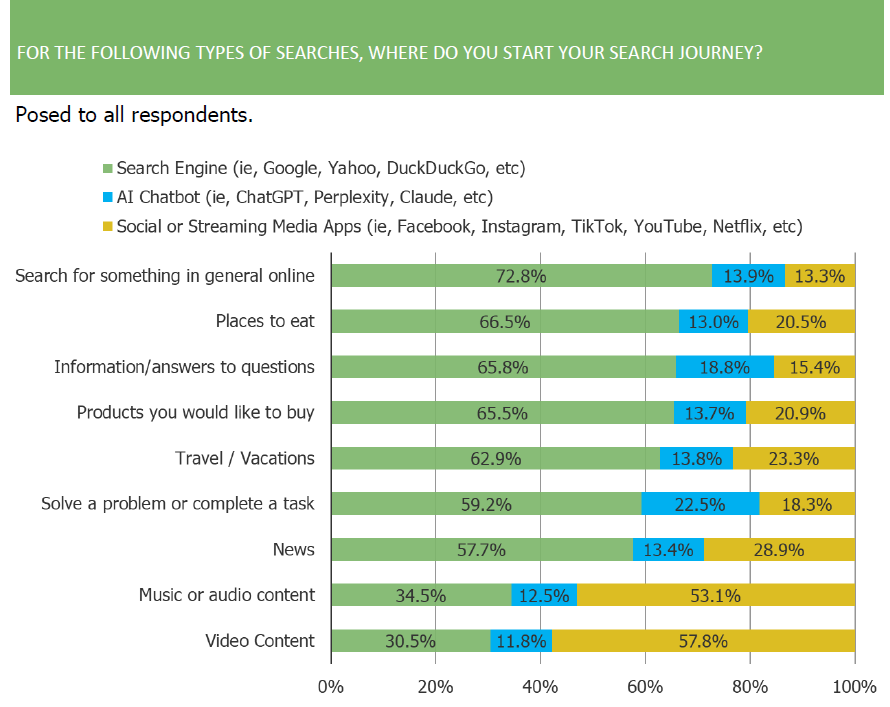

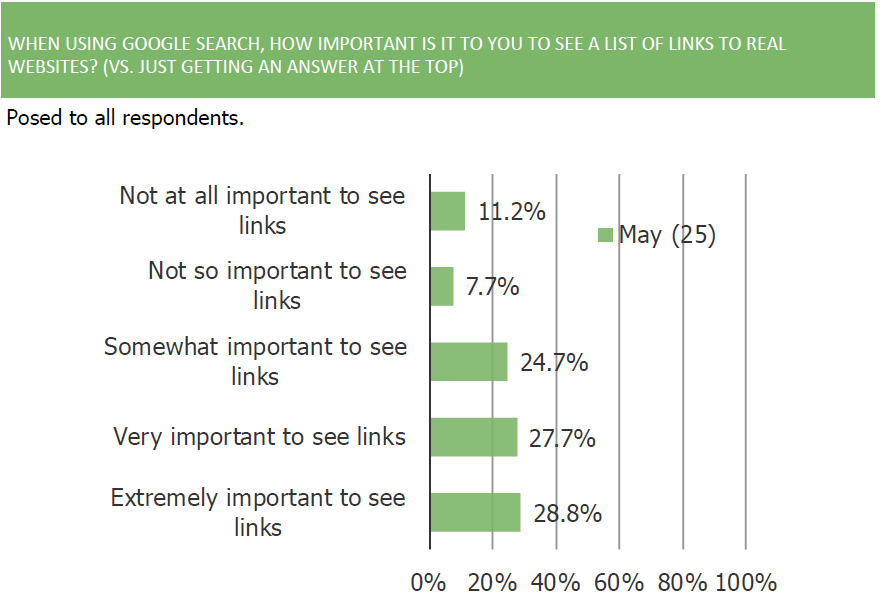

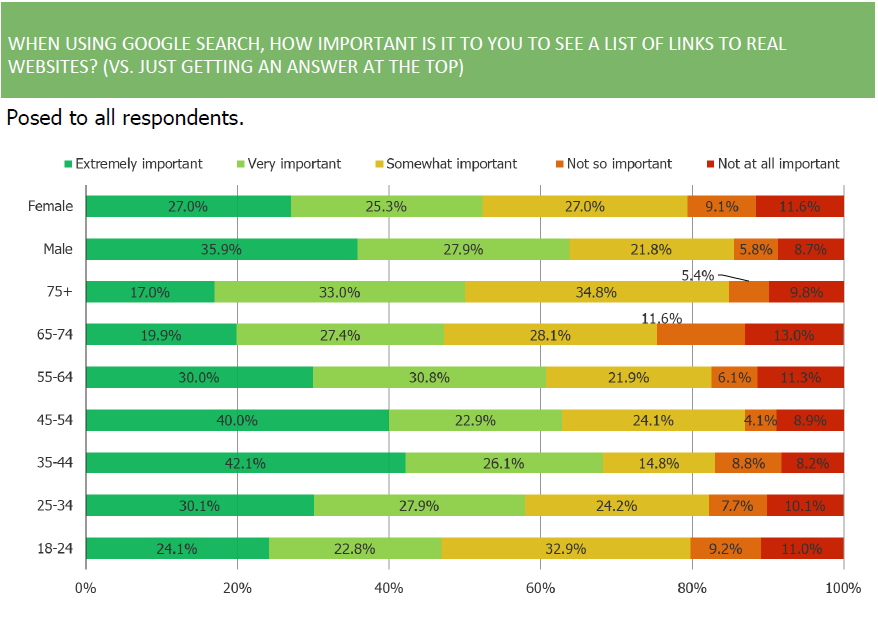

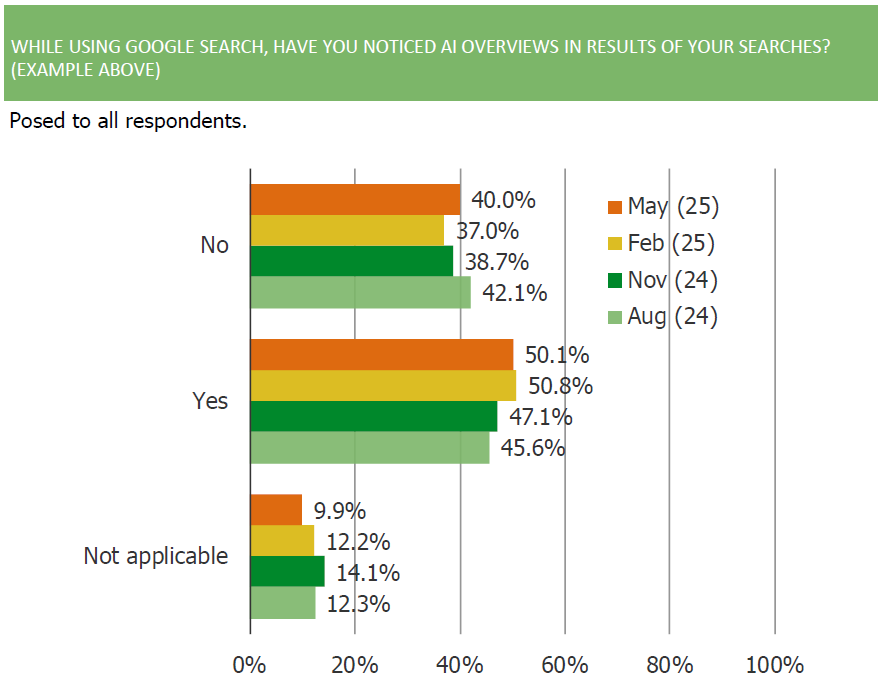

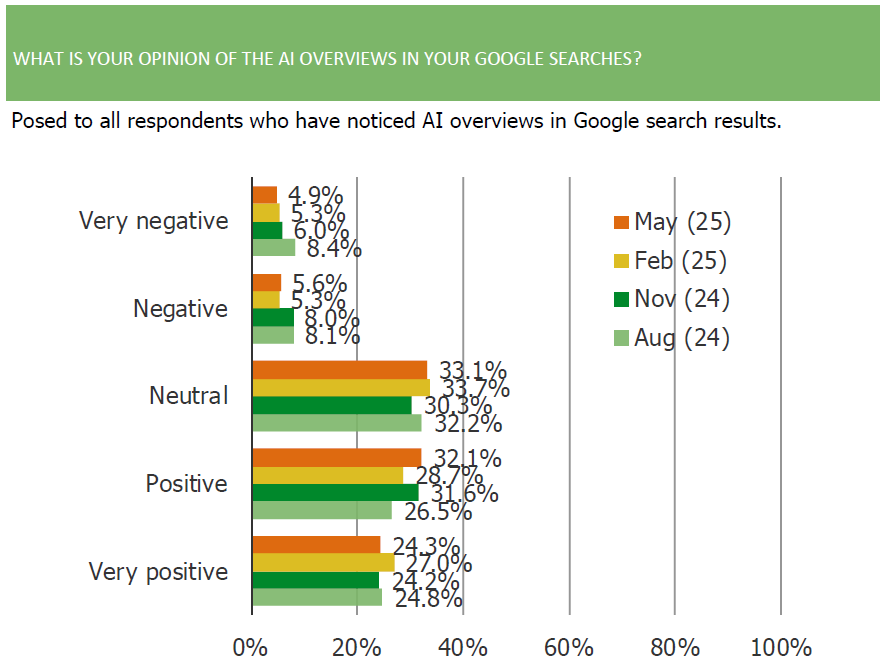

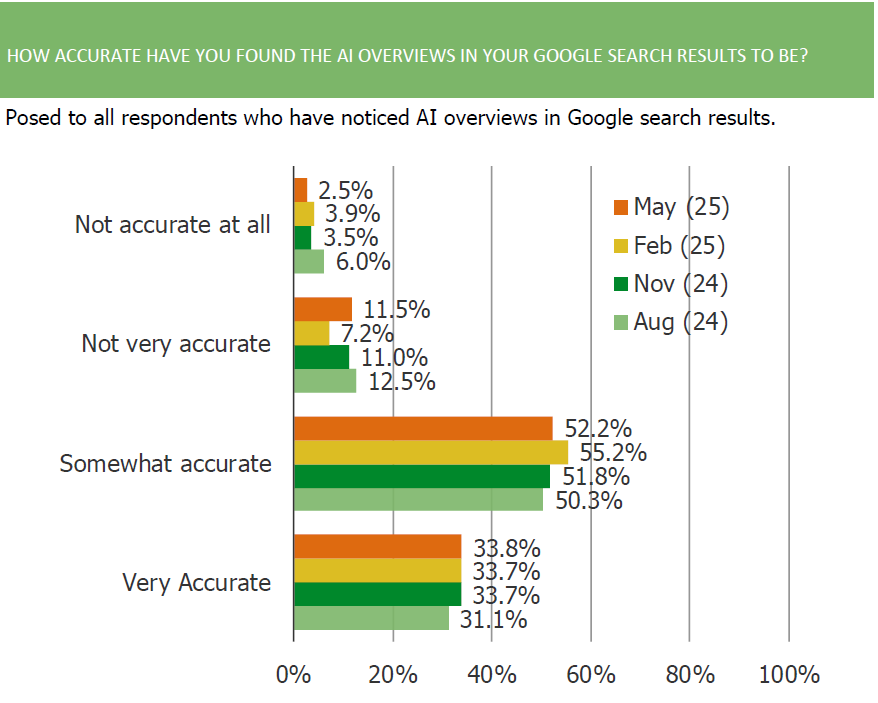

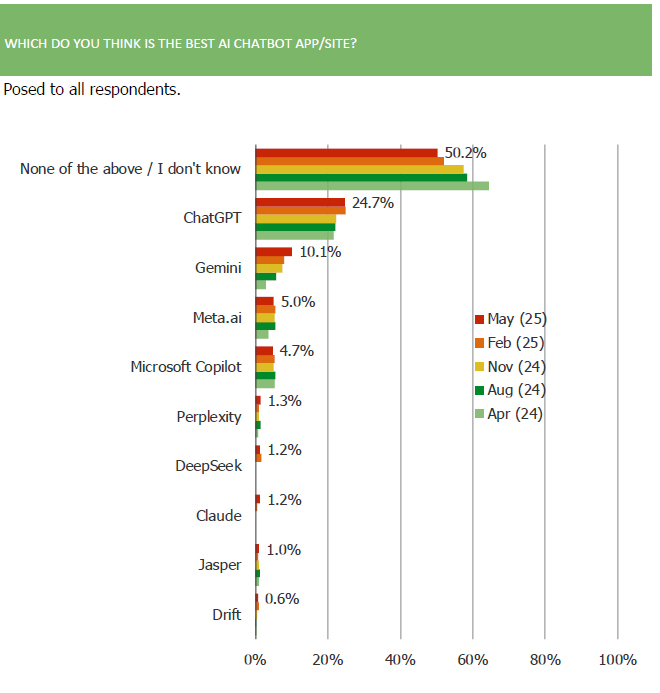

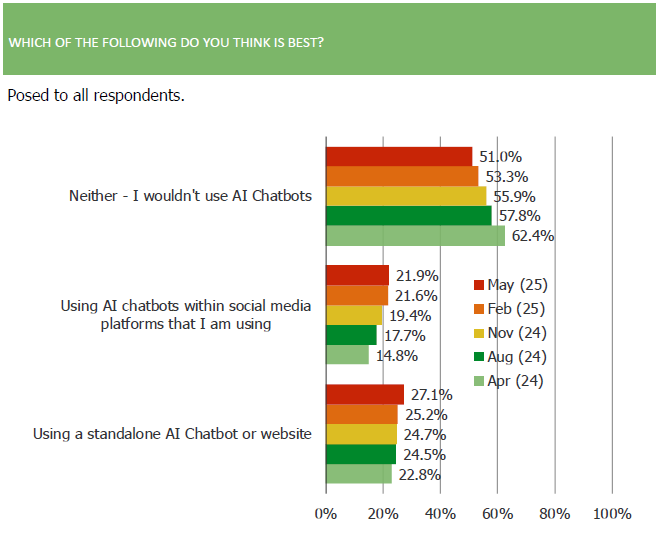

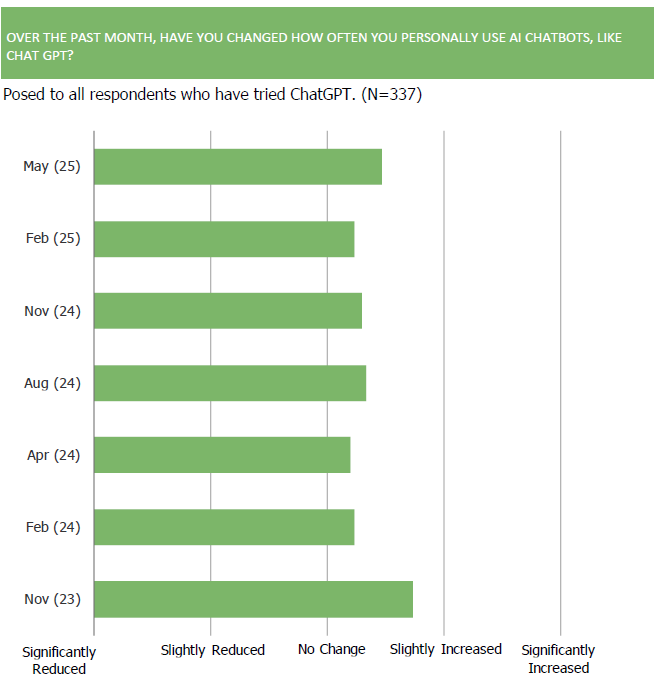

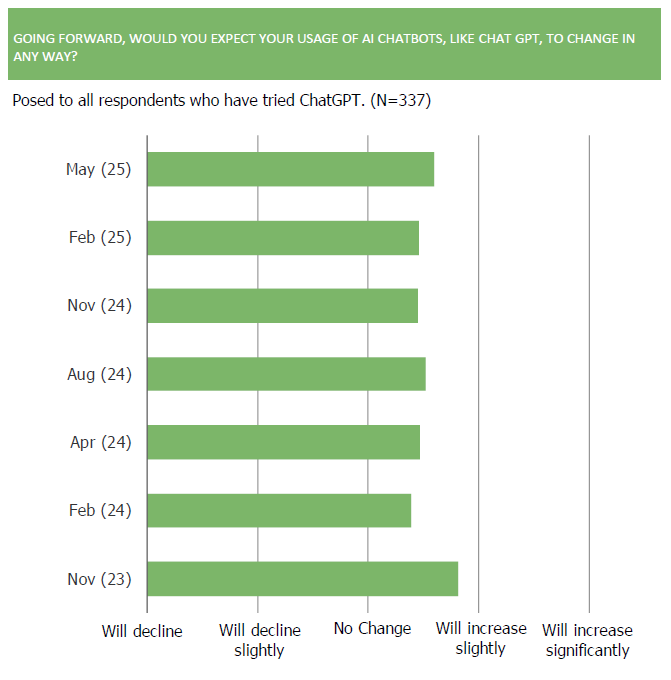

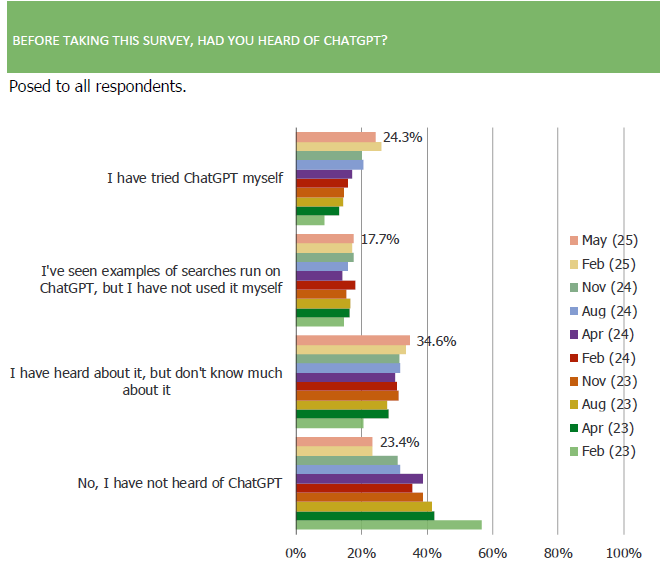

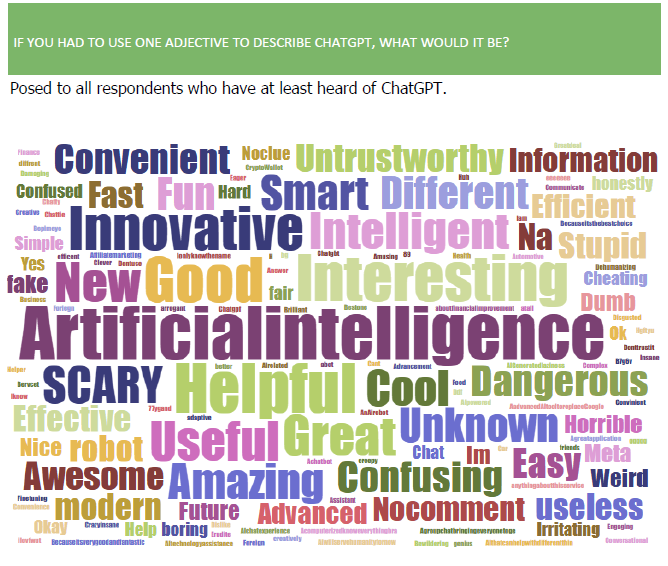

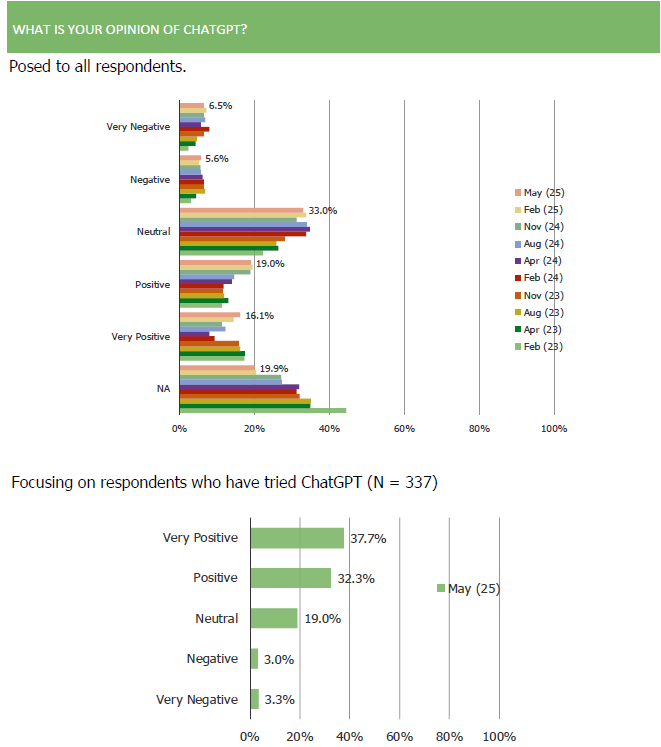

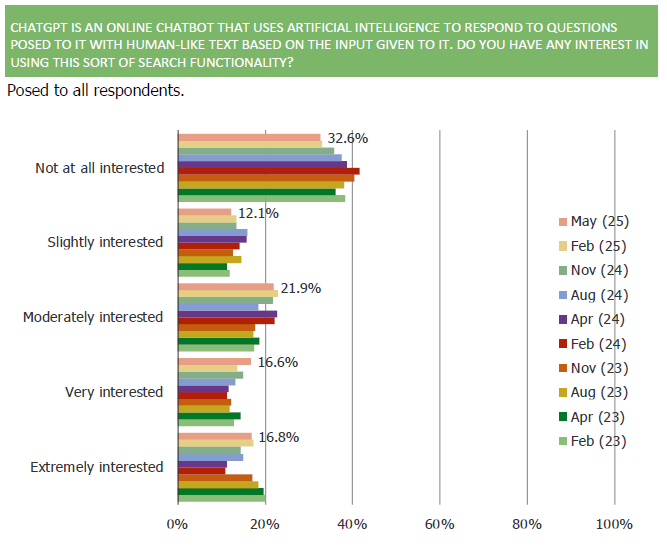

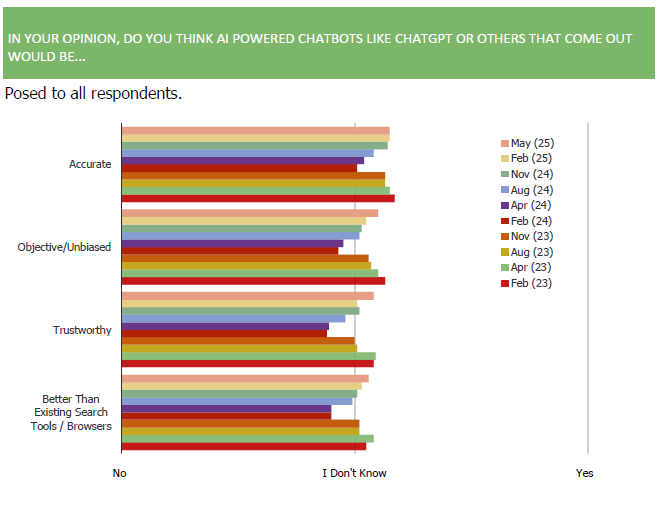

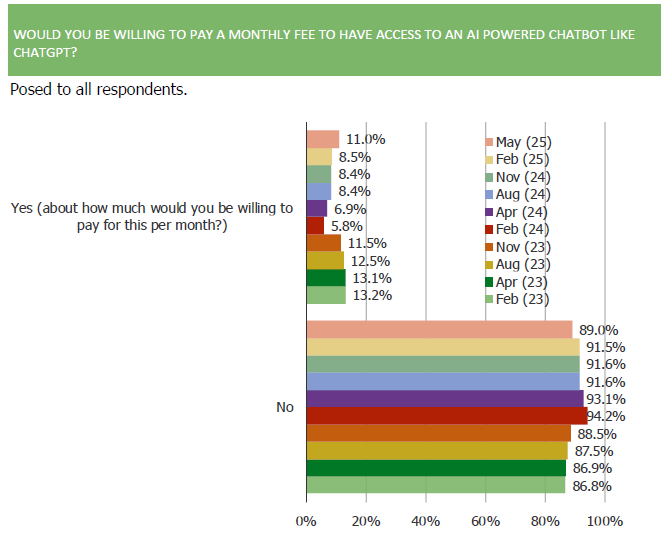

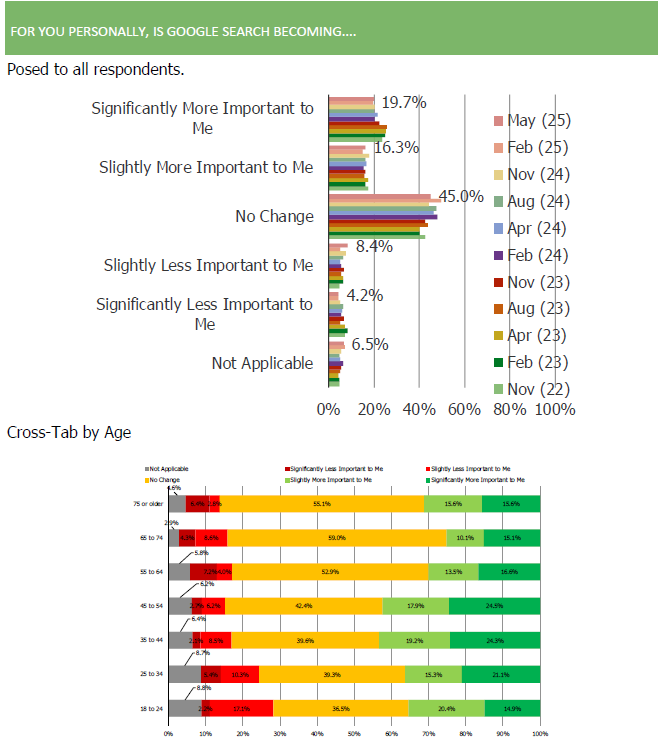

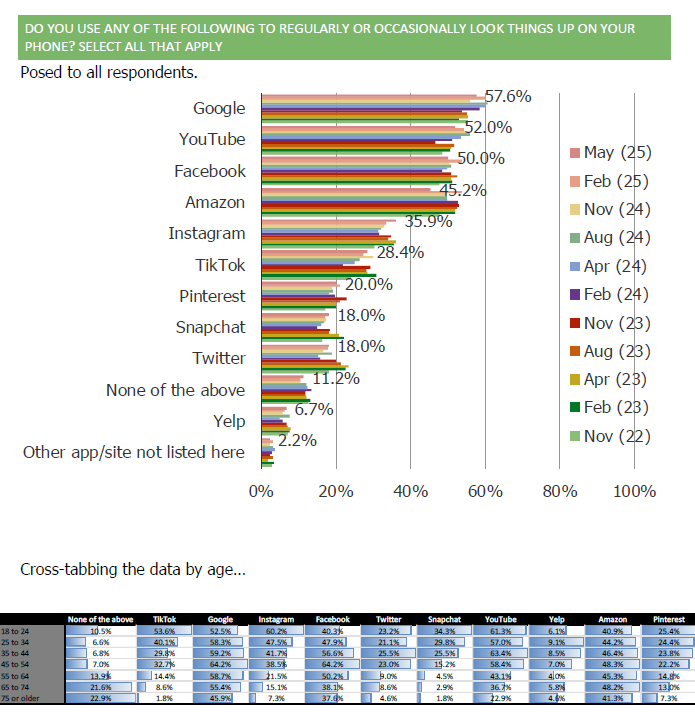

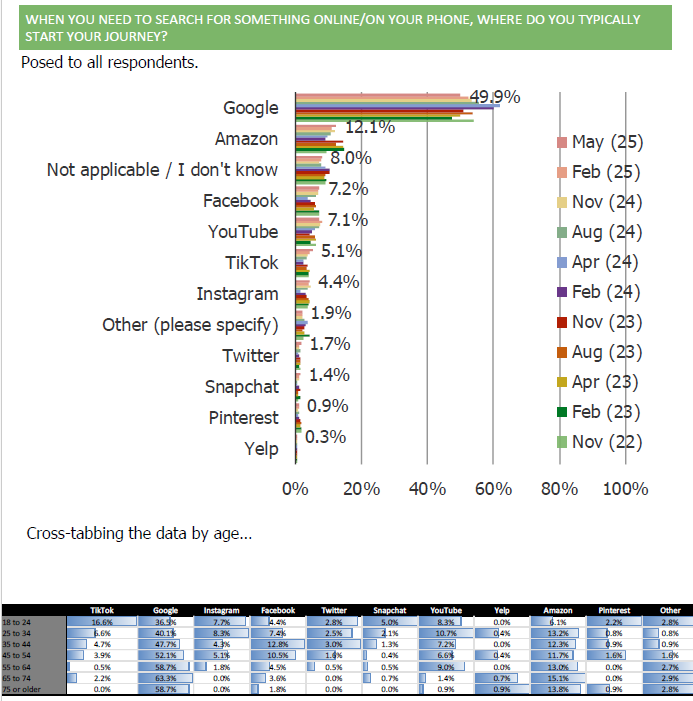

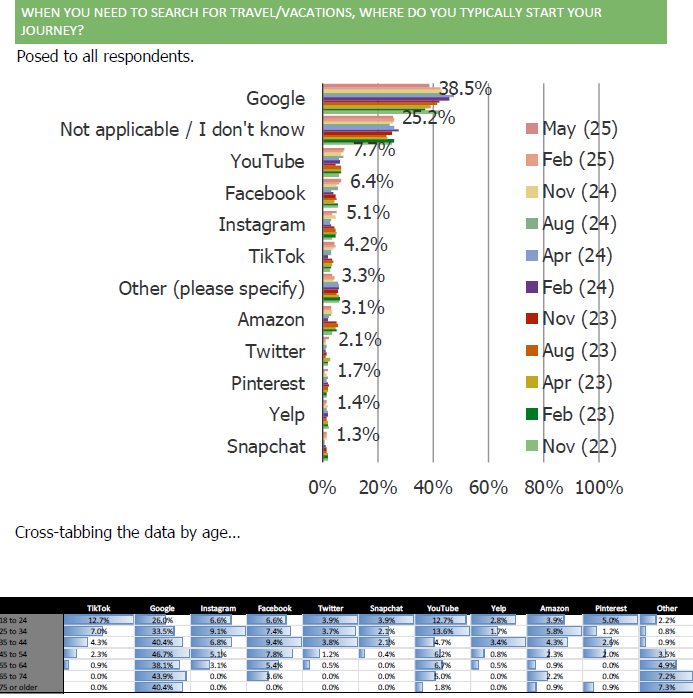

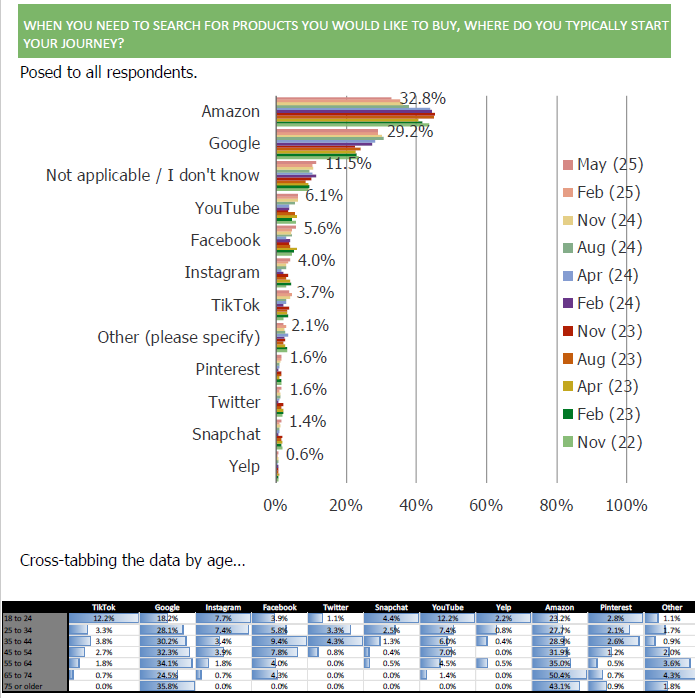

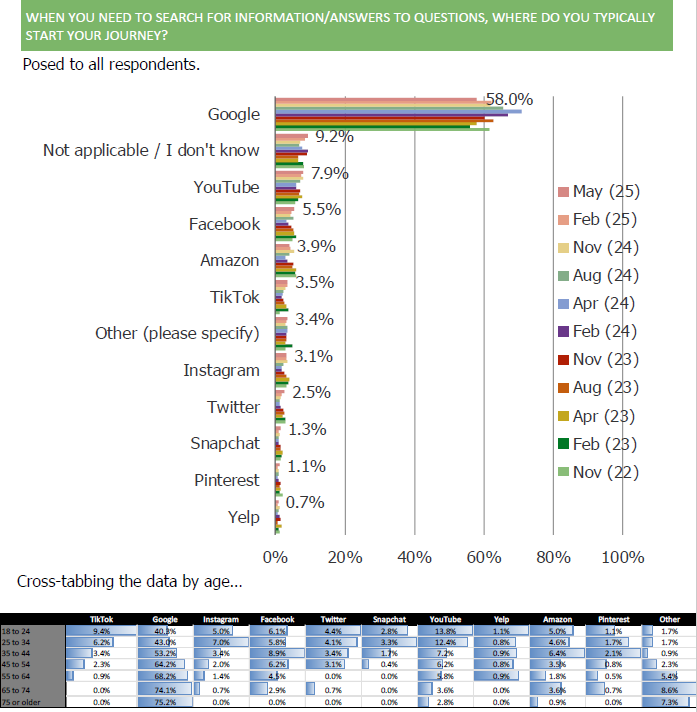

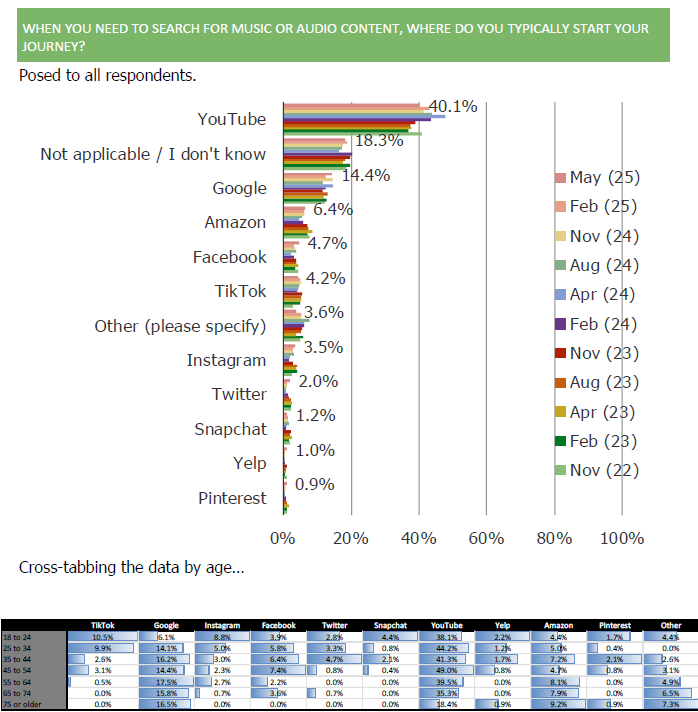

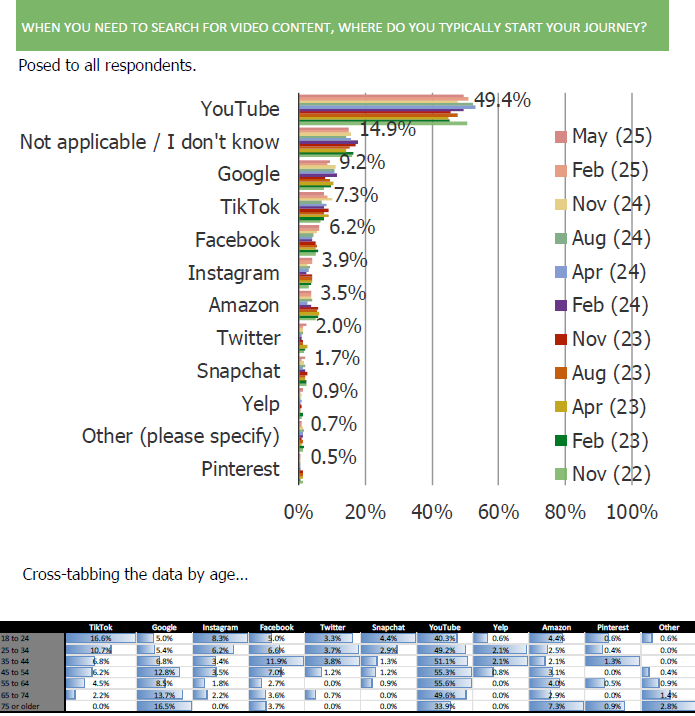

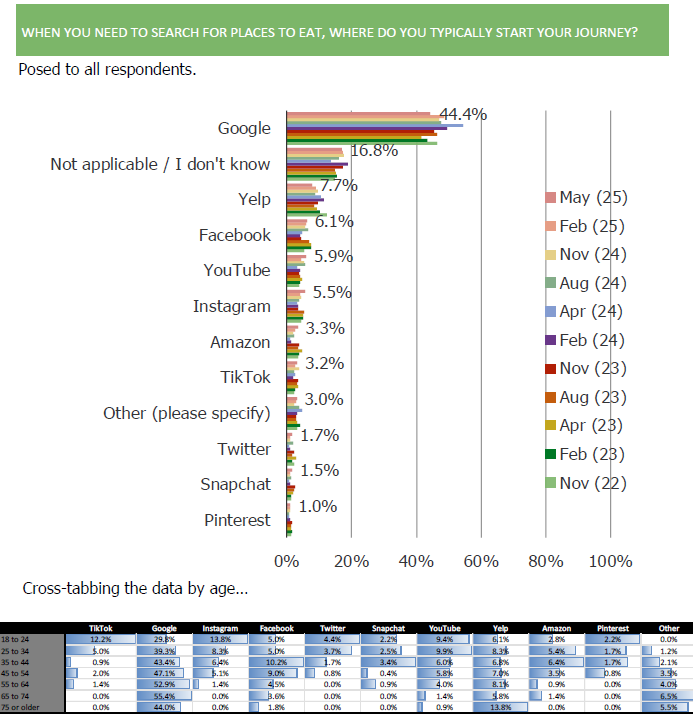

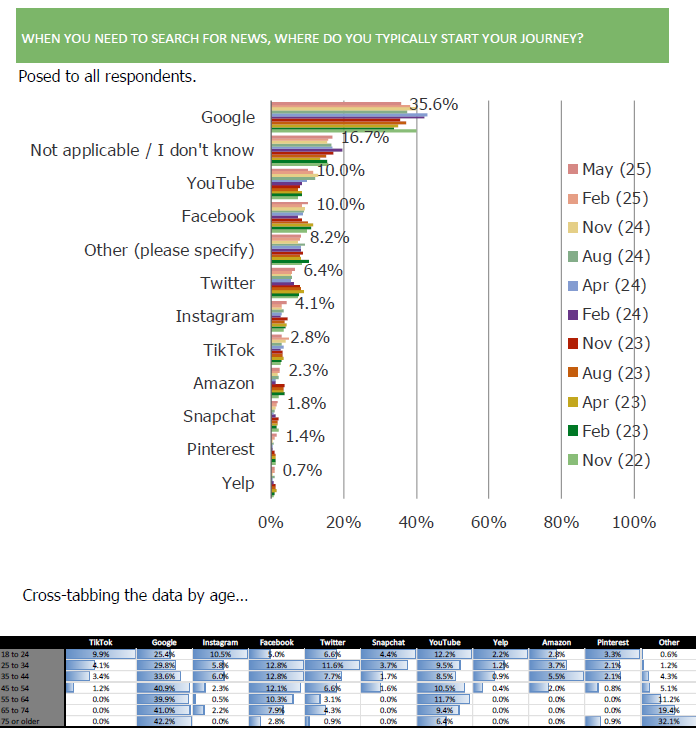

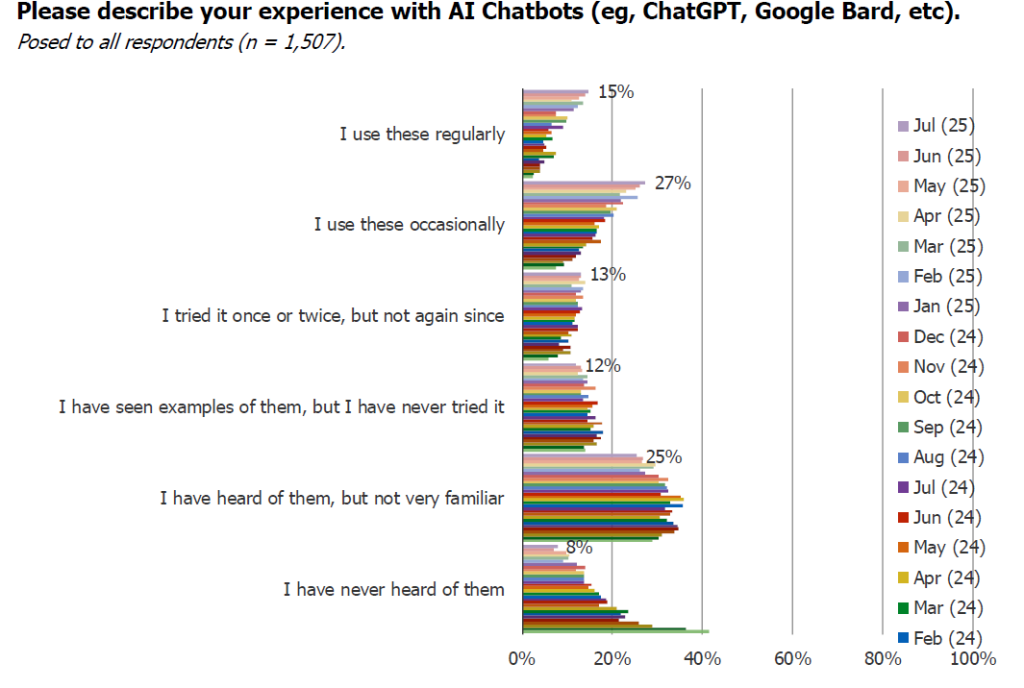

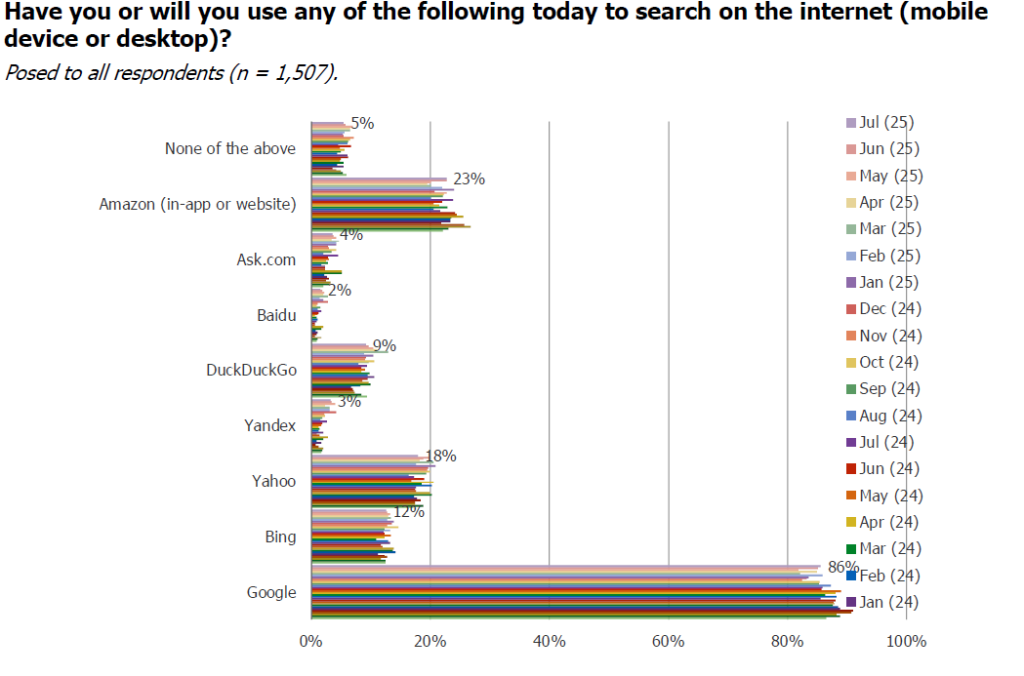

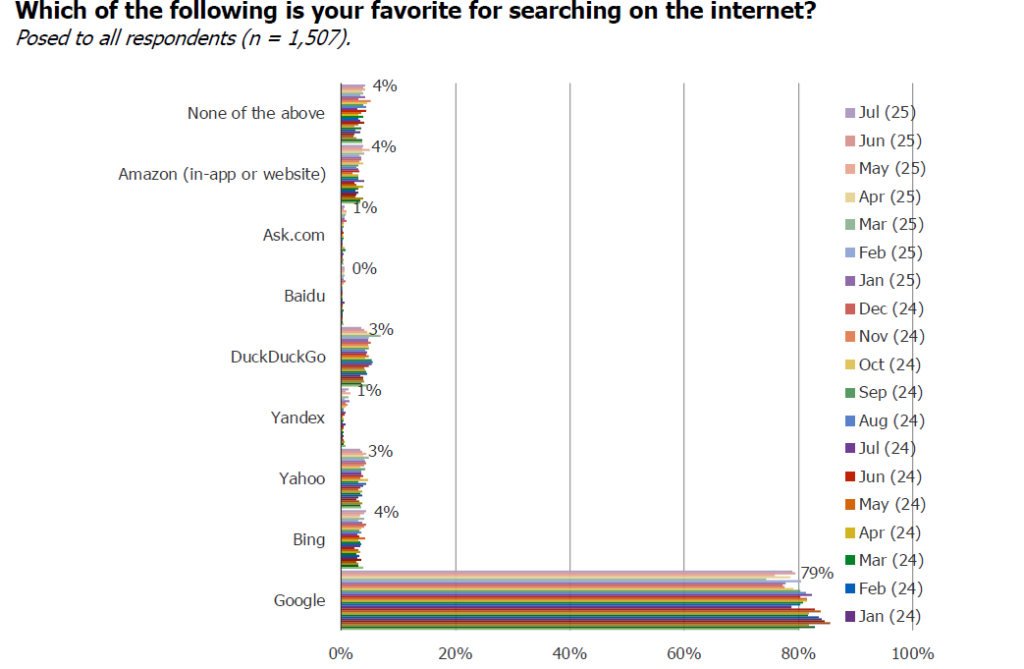

(GOOG, ChatGPT) Consumer Search Survey, Full Sample

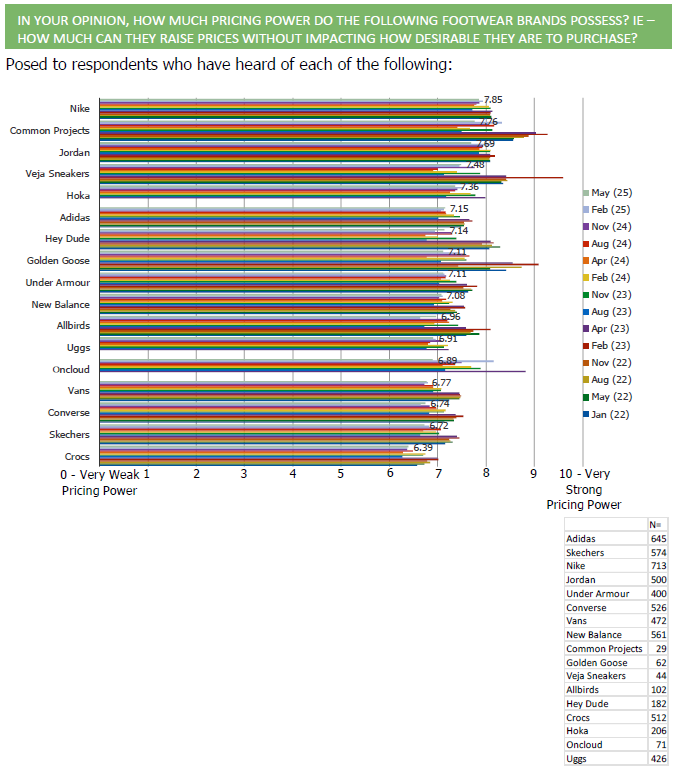

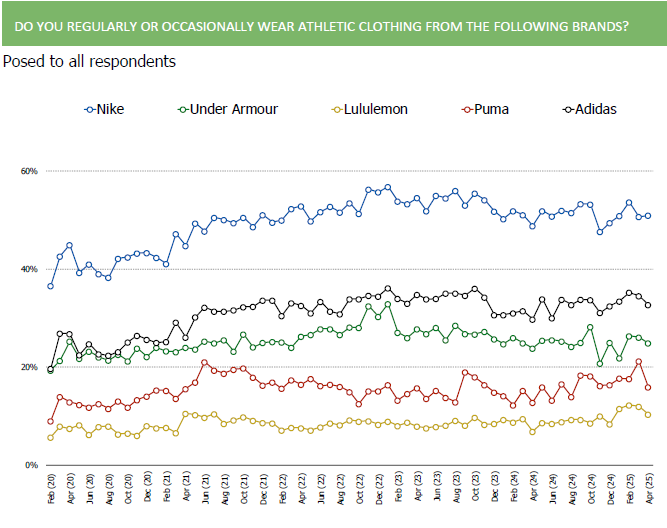

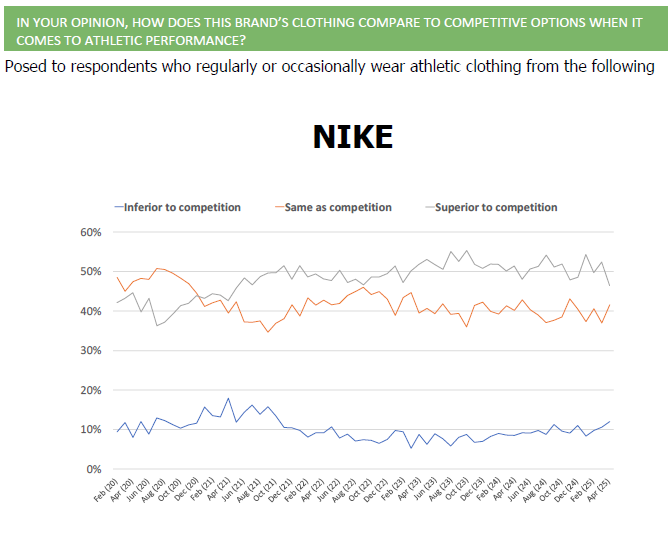

(NKE) Survey Data, US and China

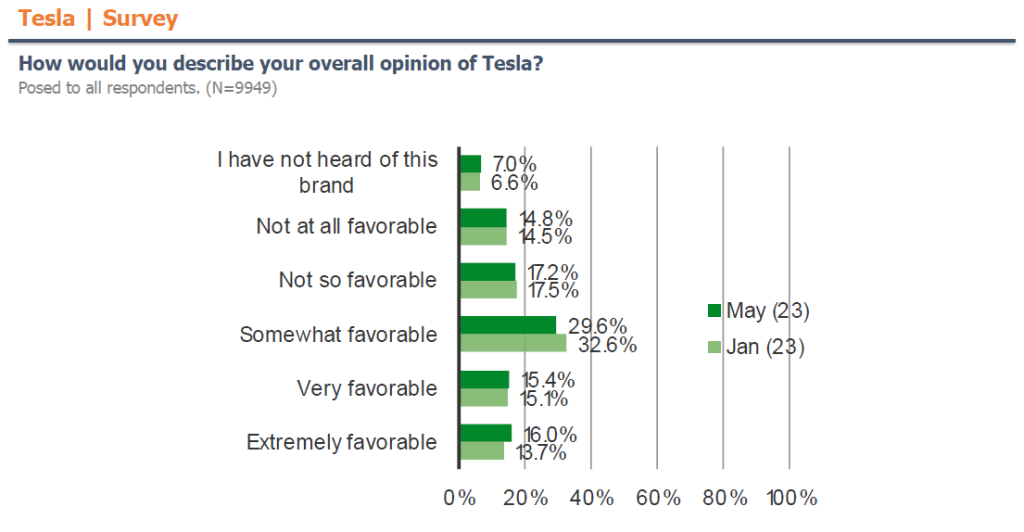

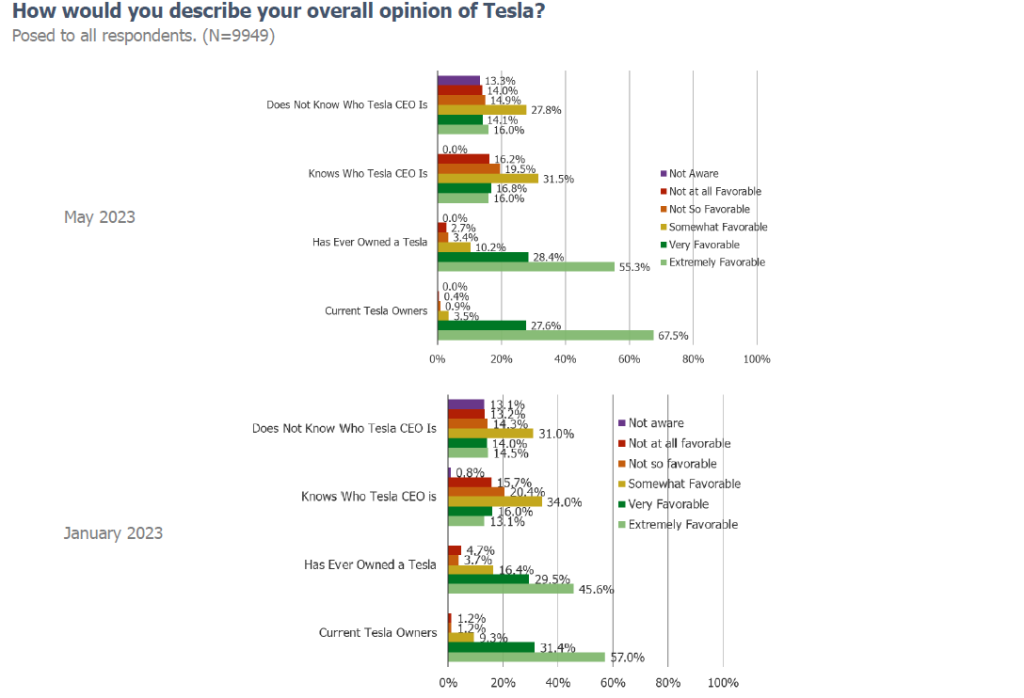

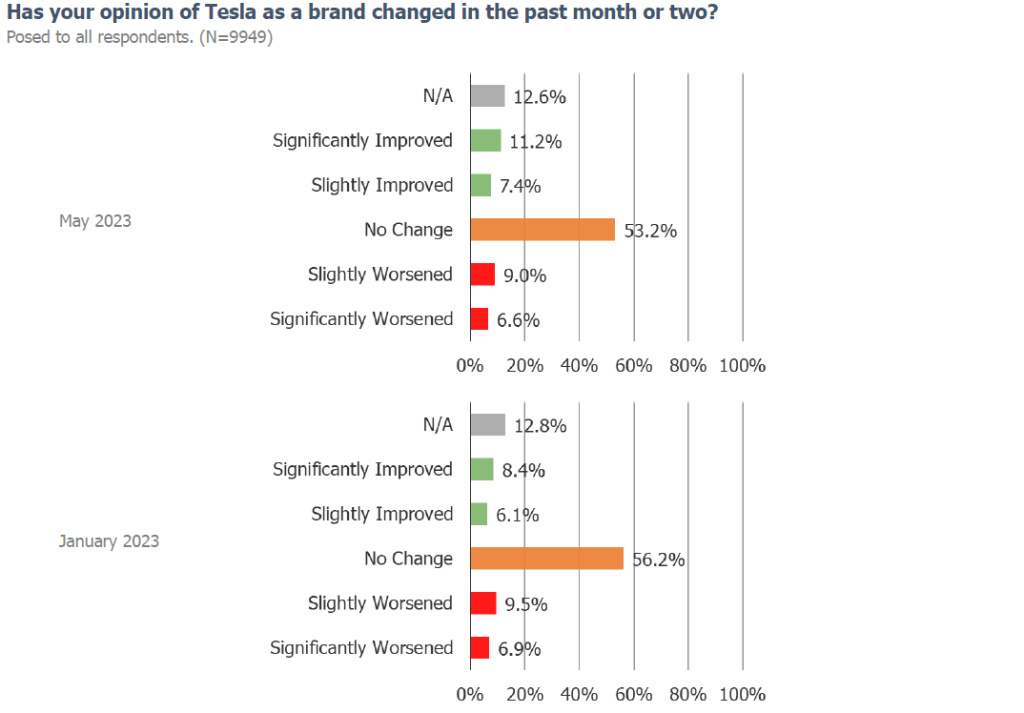

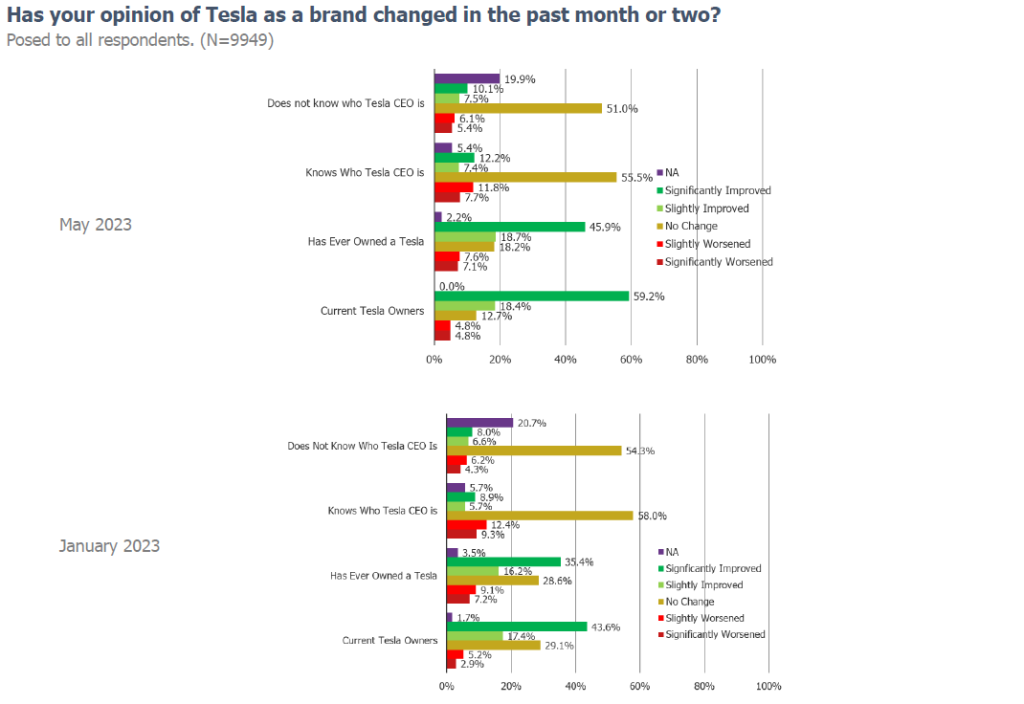

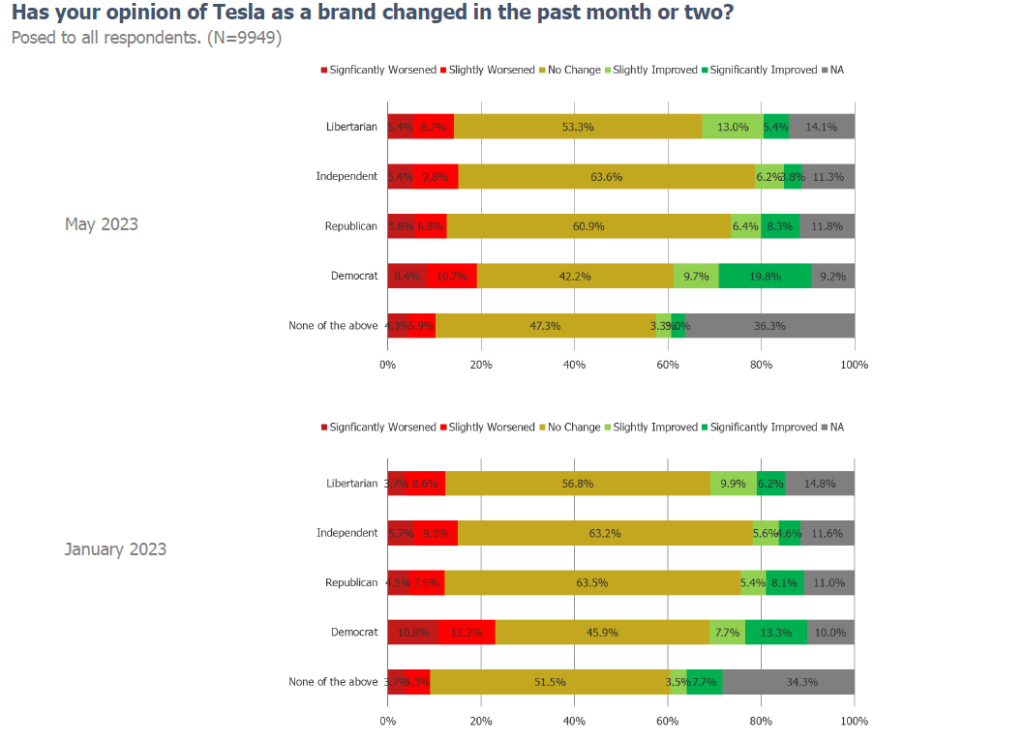

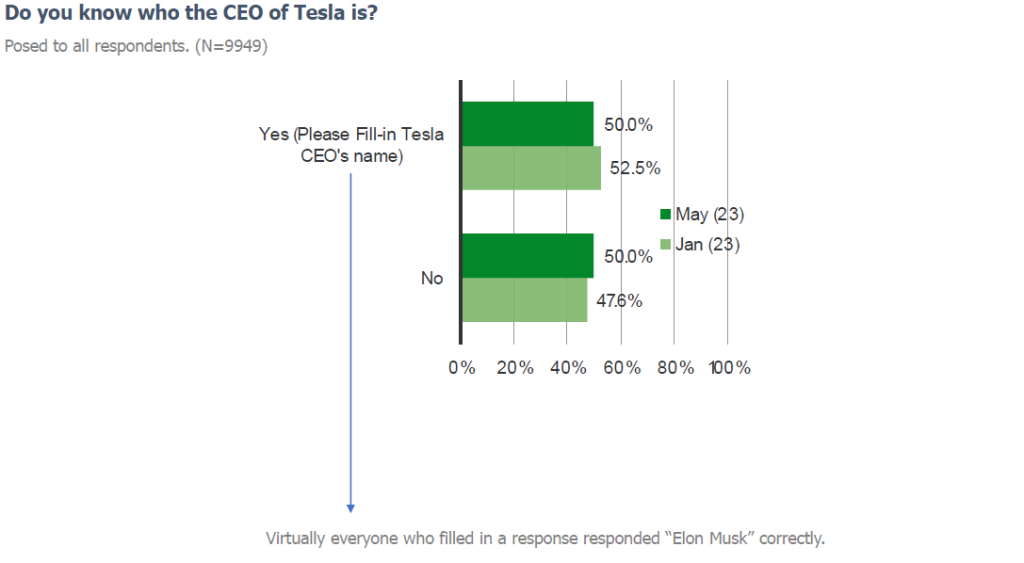

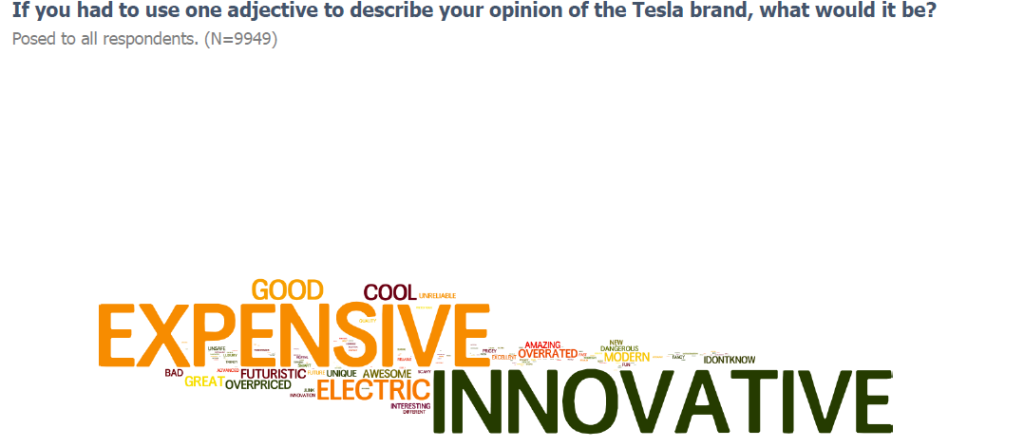

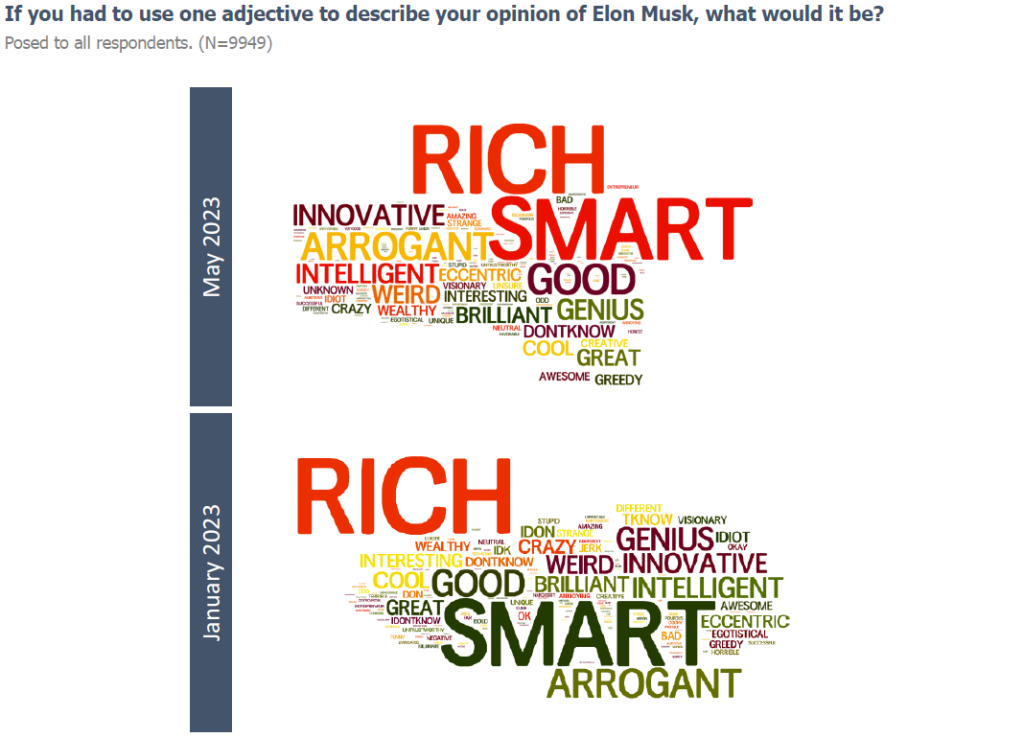

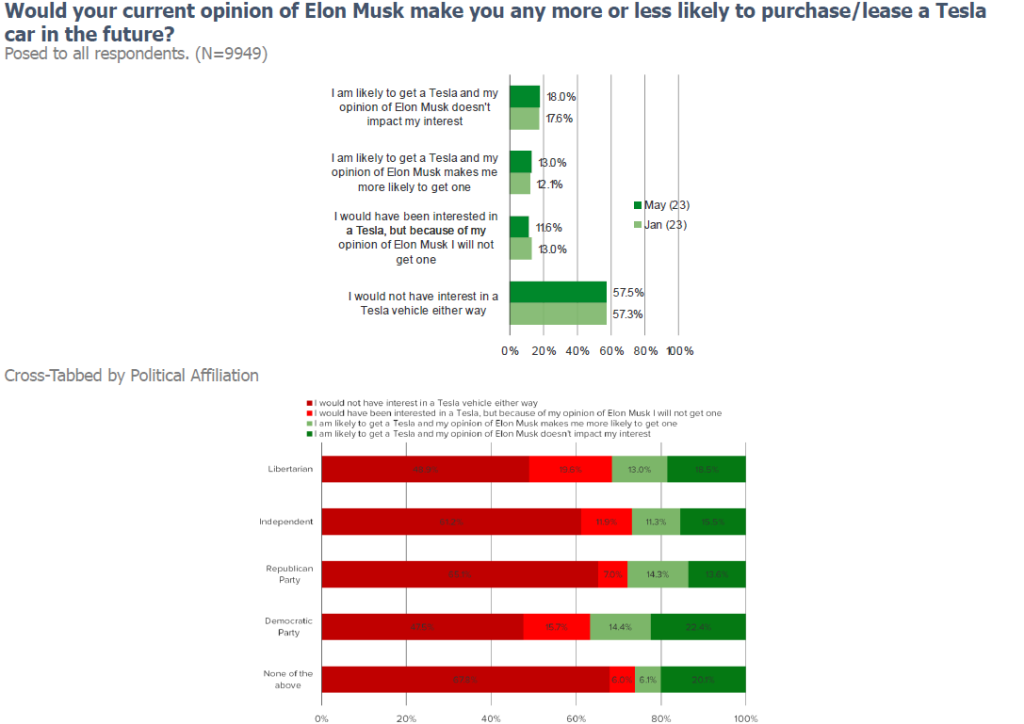

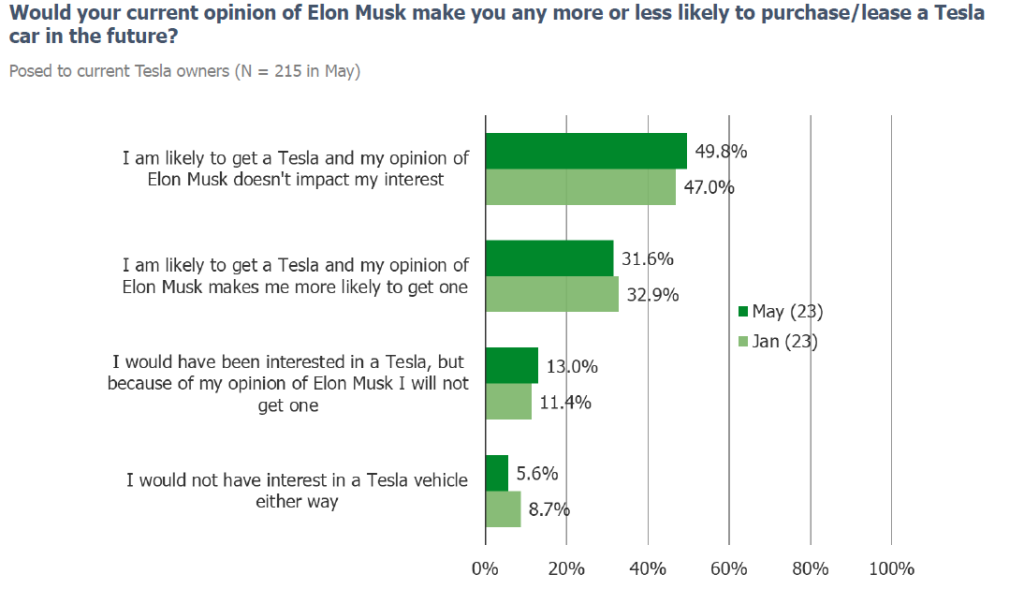

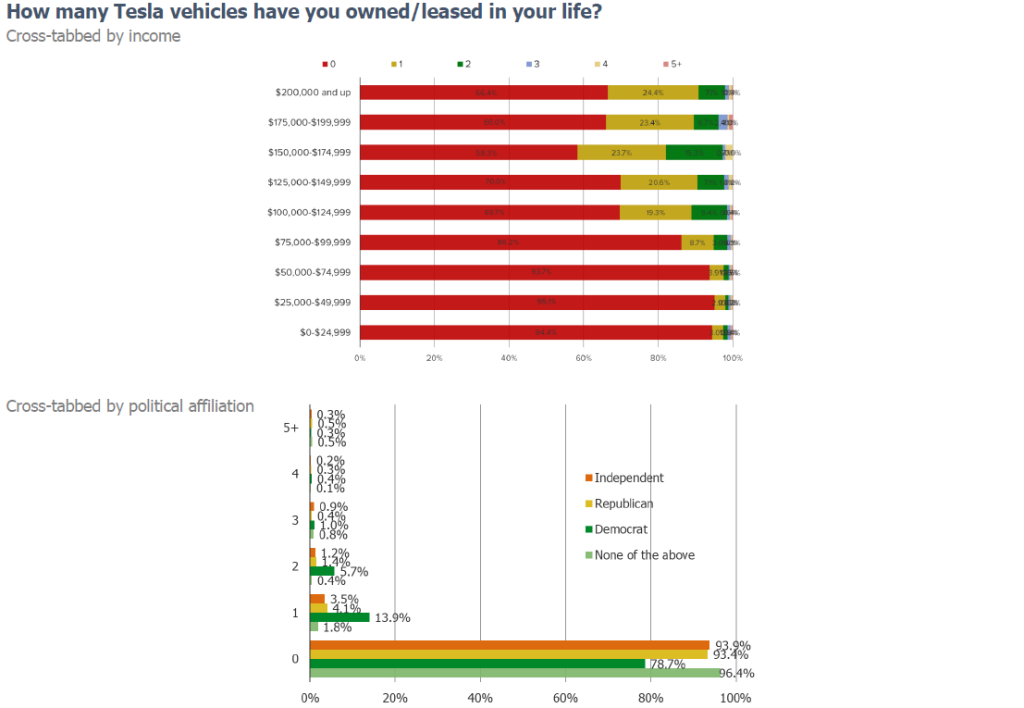

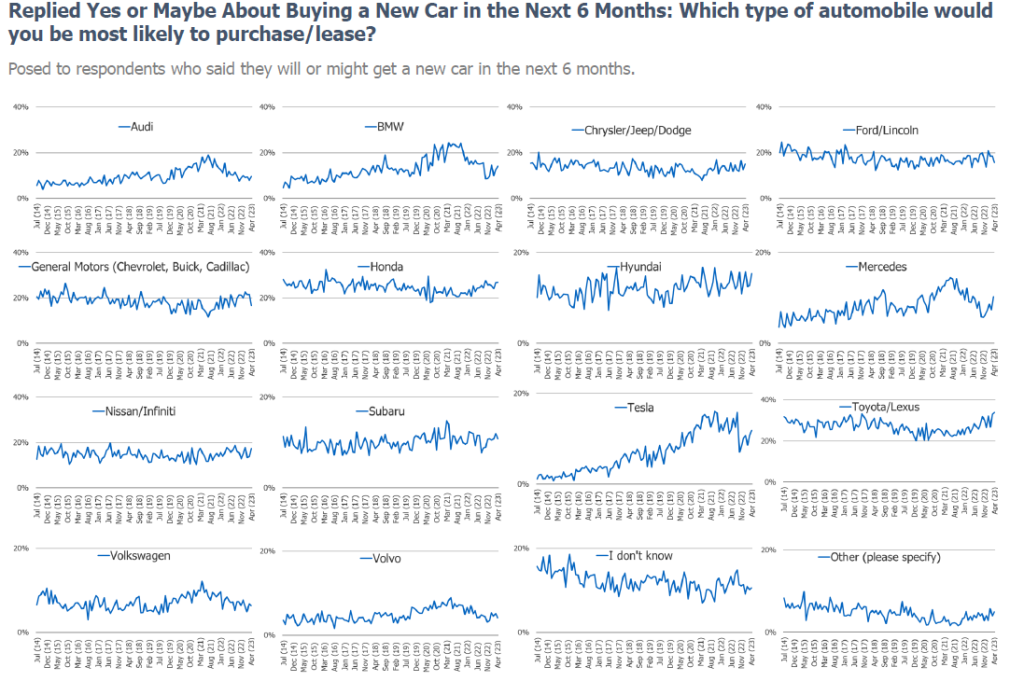

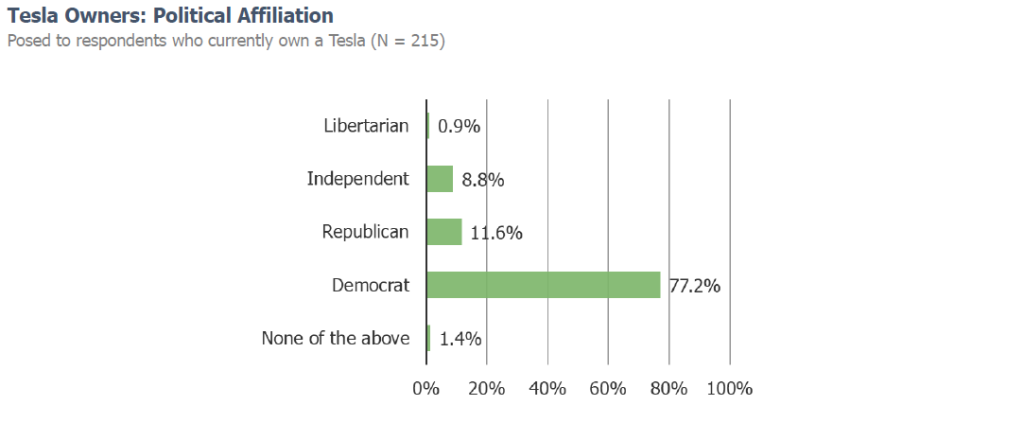

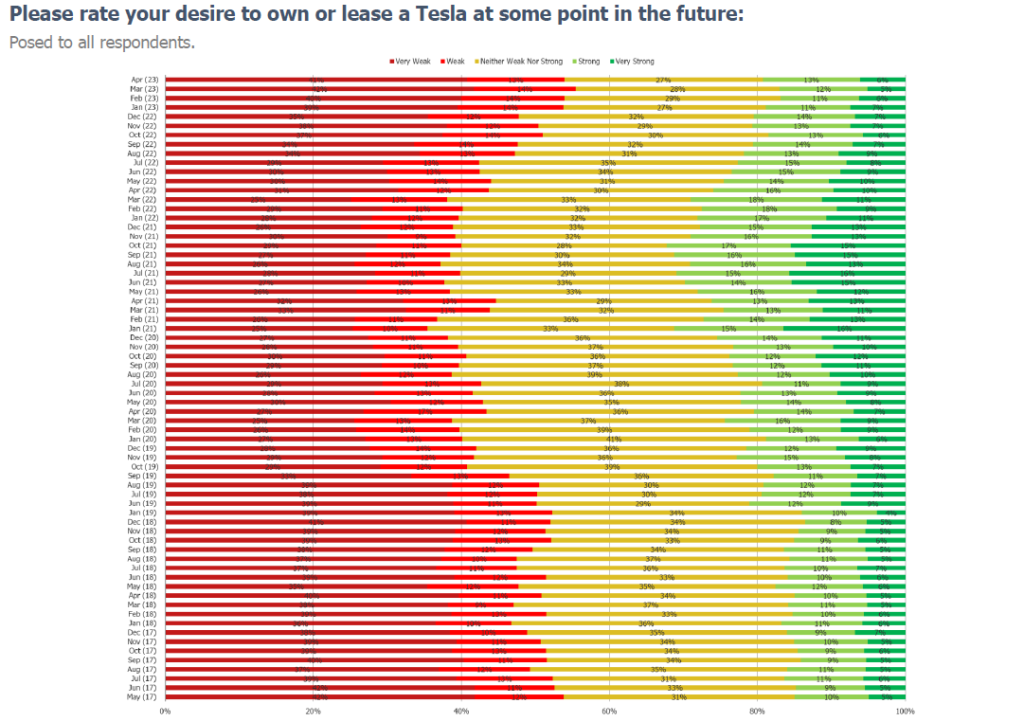

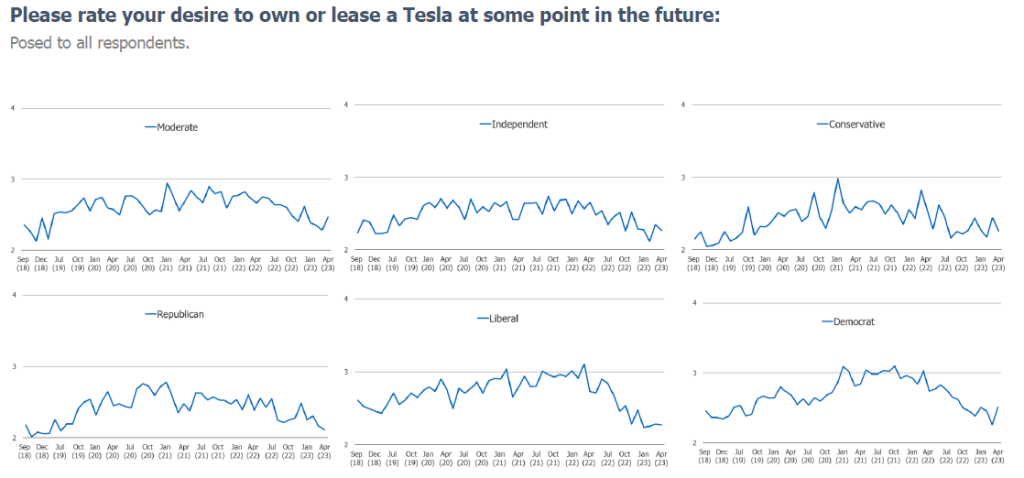

TSLA Brand Health Check (May 2023)

The below charts are from a survey conducted in May 2023. We will be running this same survey with consumers over the next week. Let us know if you might have any interest in the upcoming results!

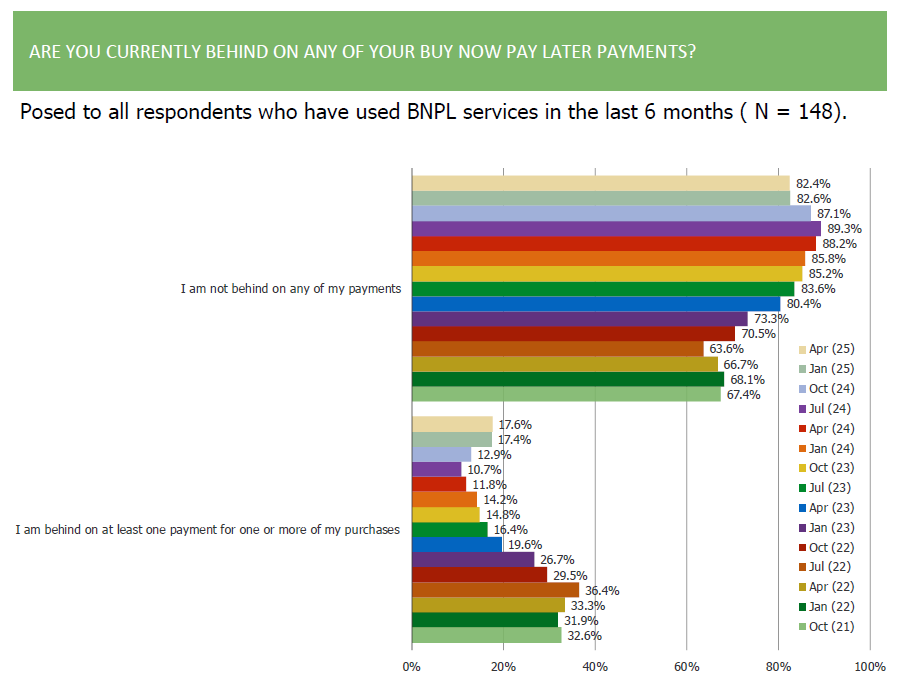

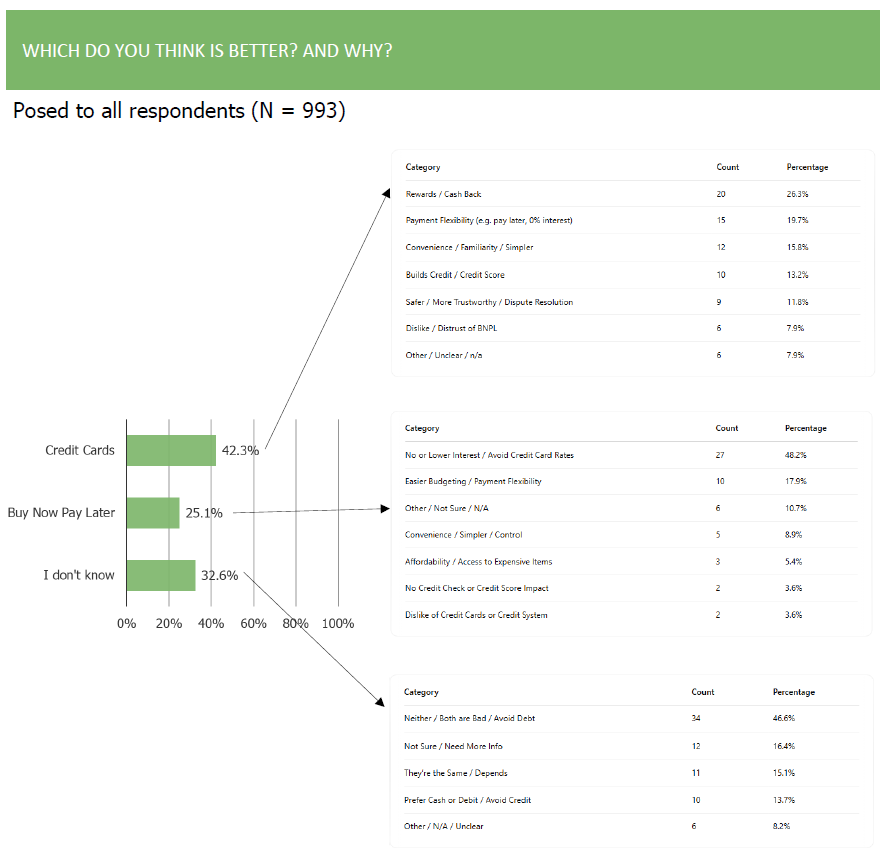

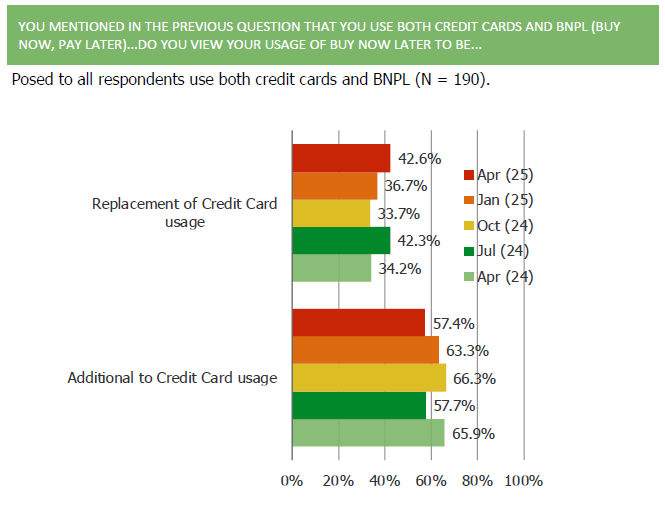

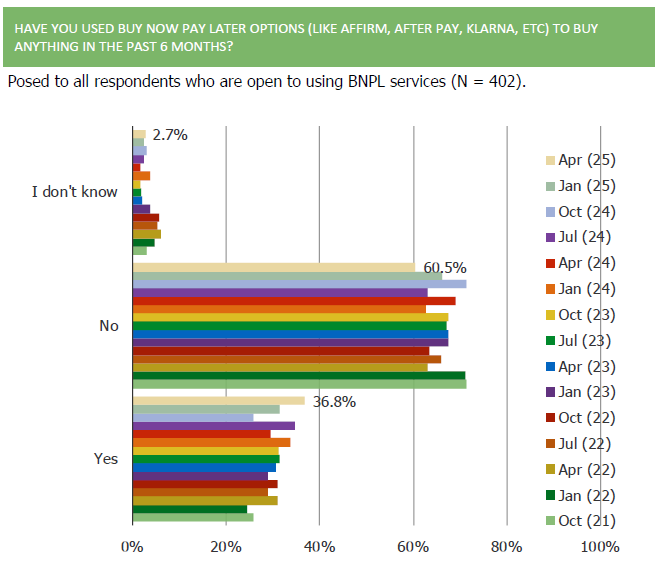

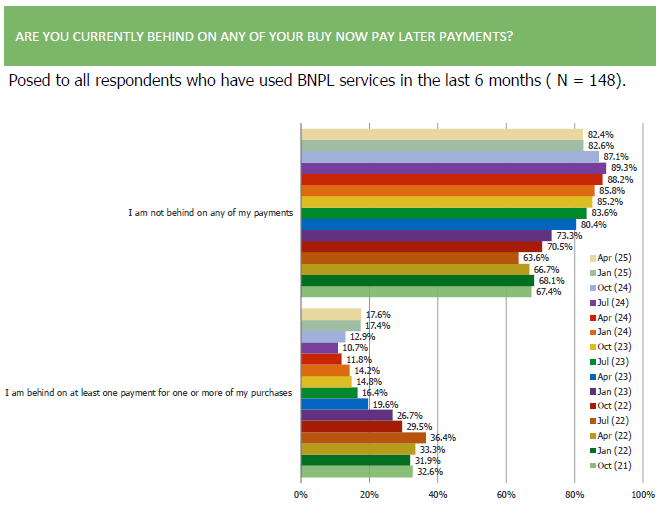

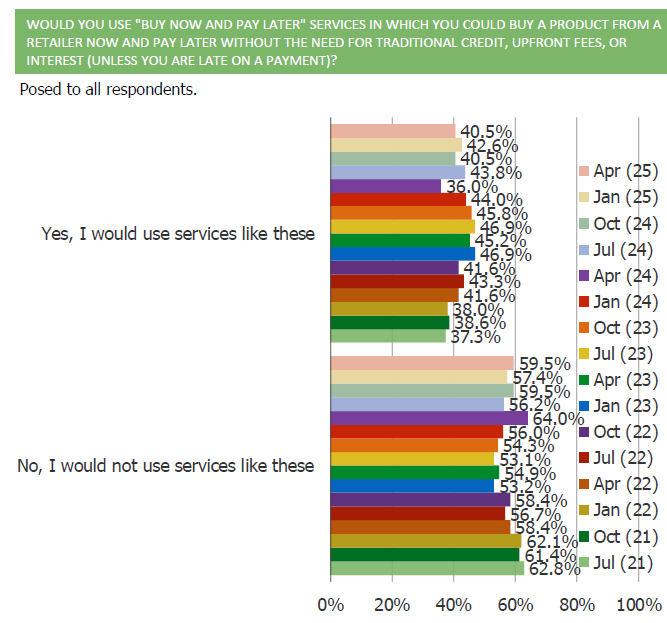

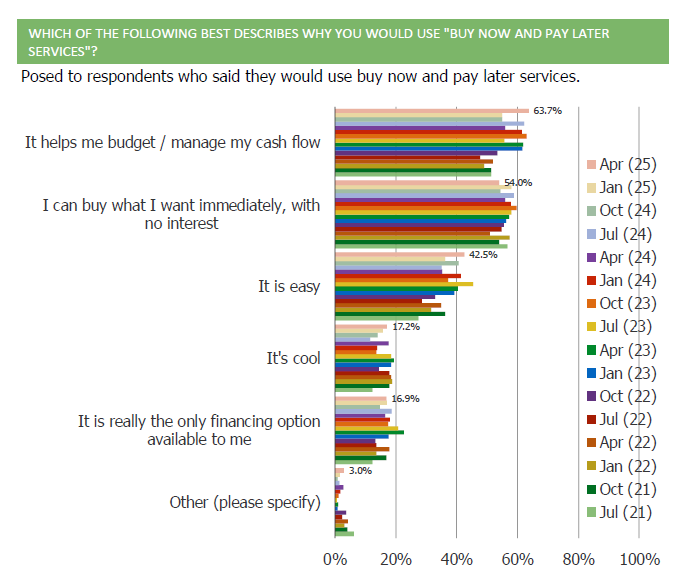

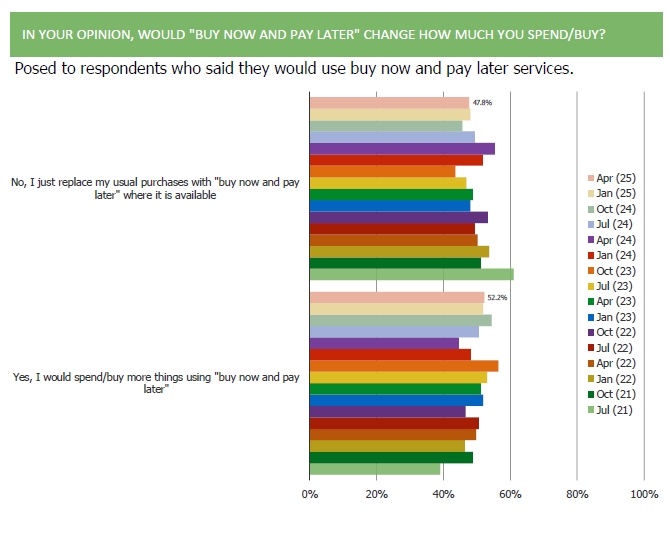

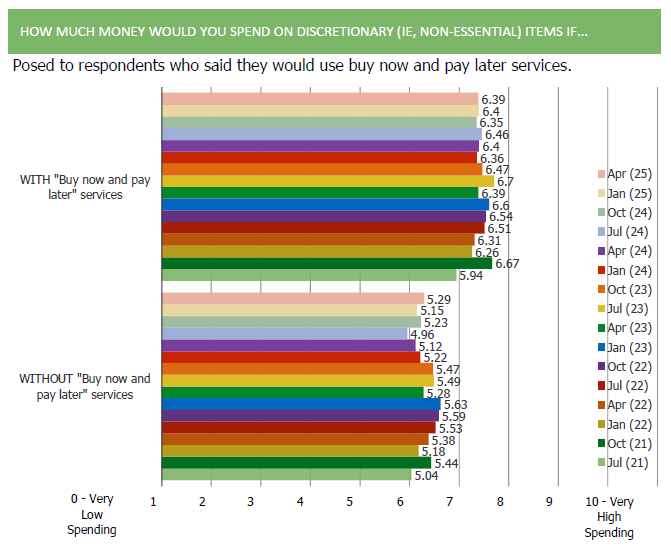

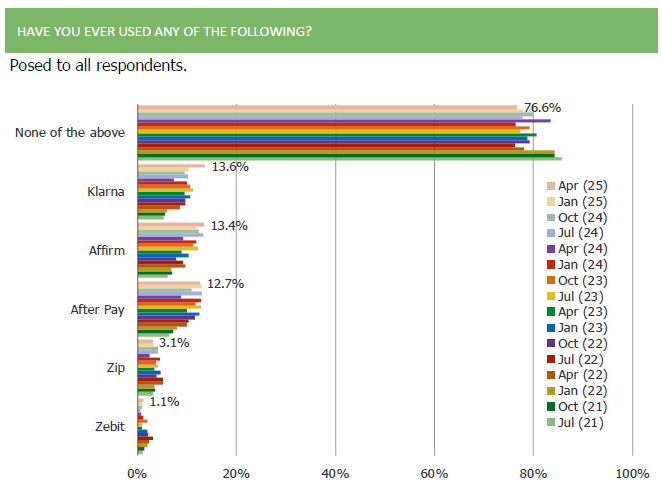

BNPL Survey Report, With History

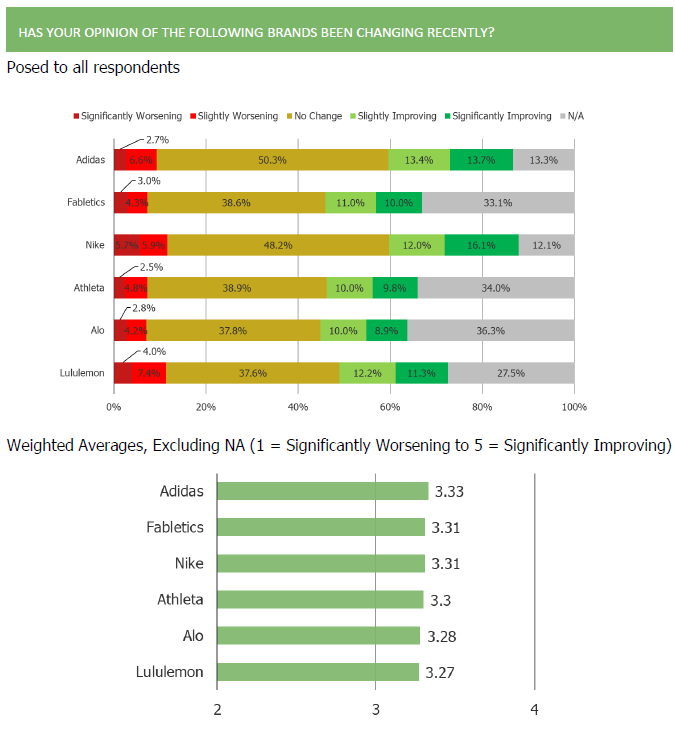

Consumers Are, ON CLOUD, Nine….

Positives:

- Consumers love the brand and opinions are improving.

- Pricing power with consumers.

- High quality customers (over-indexes to more frequent purchasers and brand direct folks).

- Over-indexes demographically to younger and higher income consumers.

- Customer base fees less bad about tariffs and has a much stronger outlook on their finances than the broader population

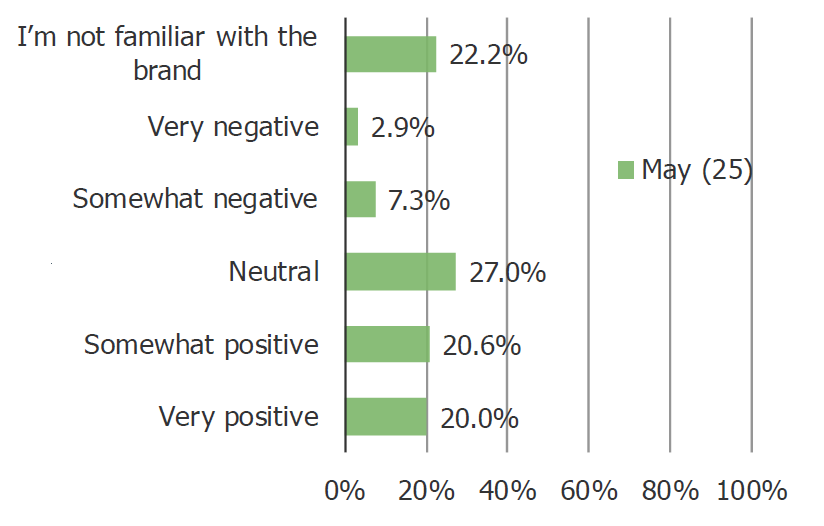

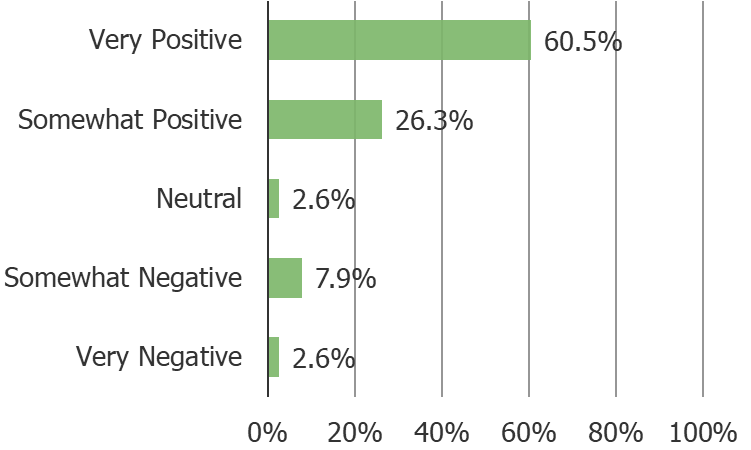

How would you describe your overall percenption of the ON (ON Cloud) brand today?

Posed to ALL respondents…

Posed to ON CLOUD Customers

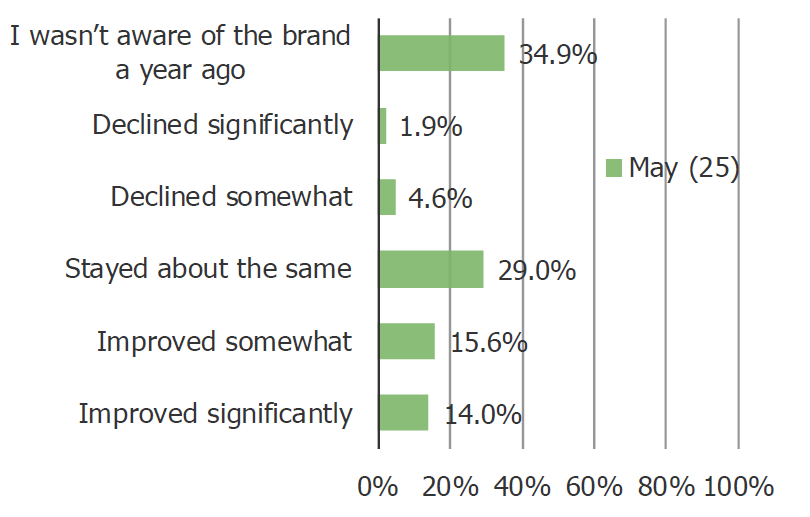

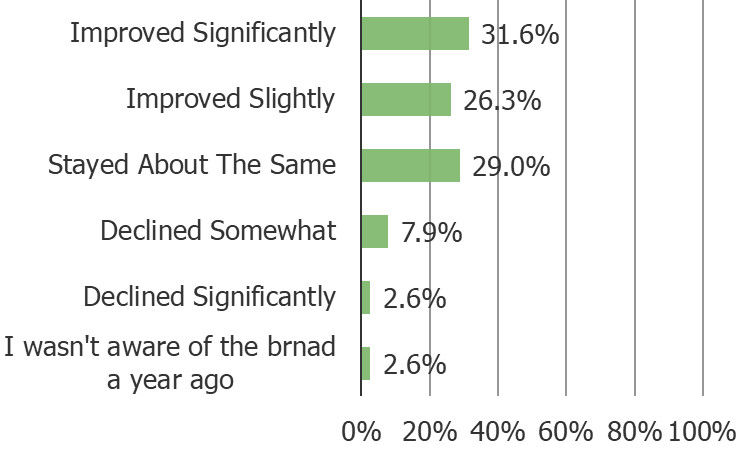

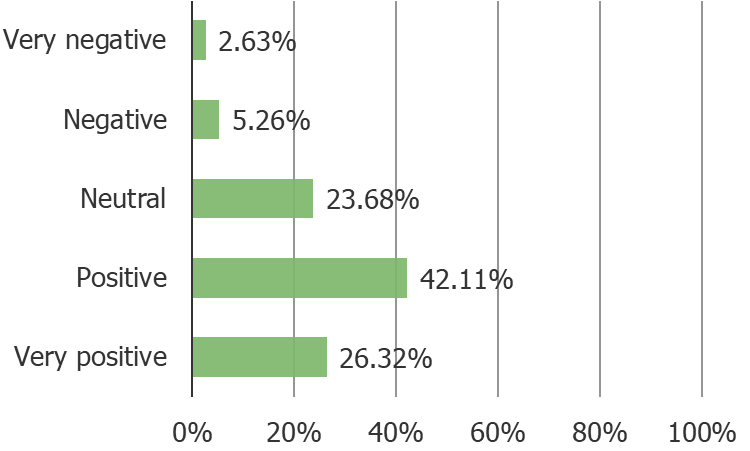

How has your perception of ON (ON Cloud) changed over the past 12 months?

Posed to ALL respondents…

Posed to ON Cloud Customers…

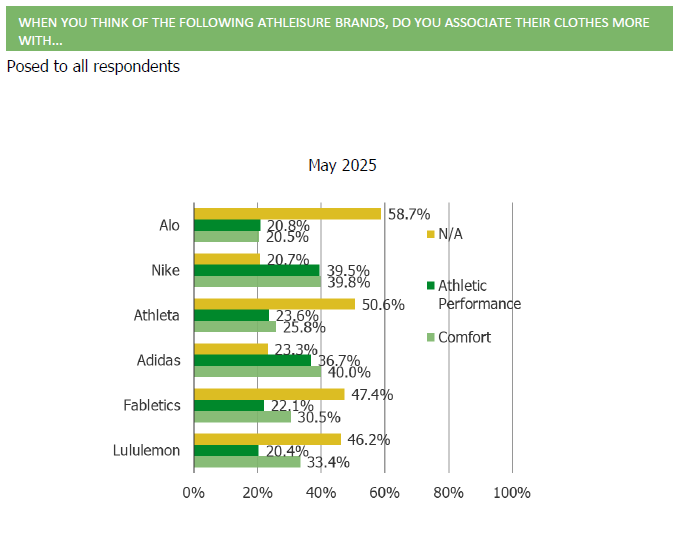

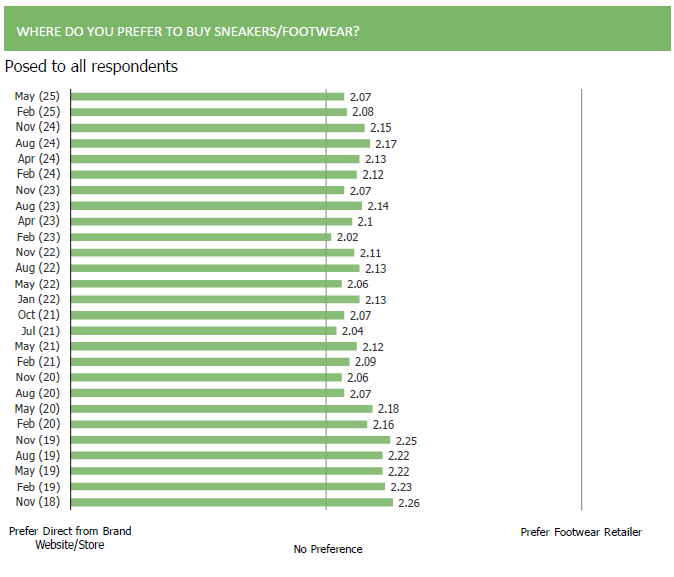

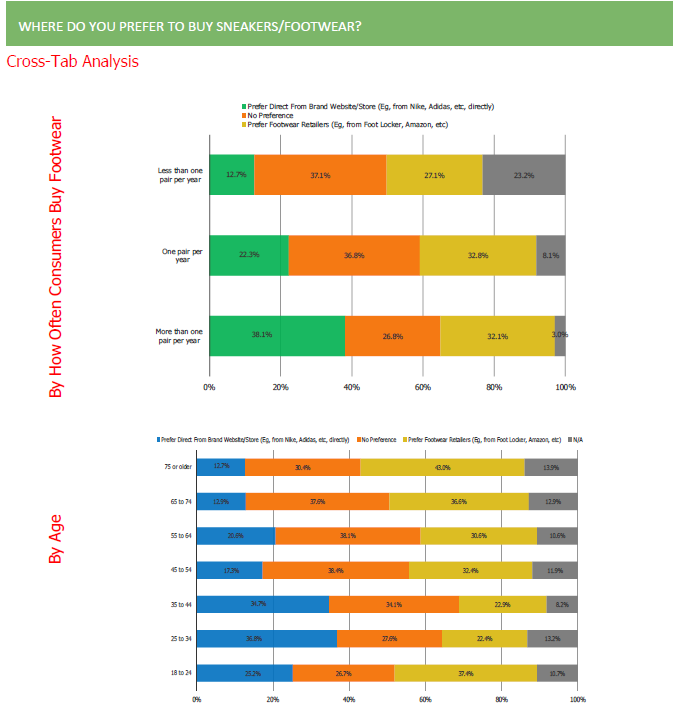

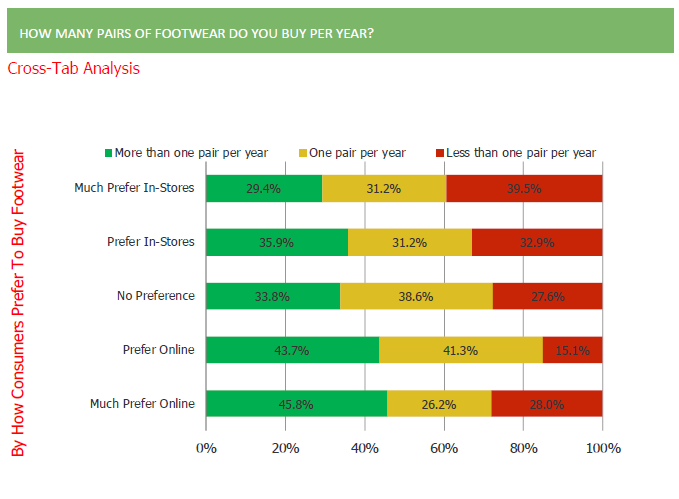

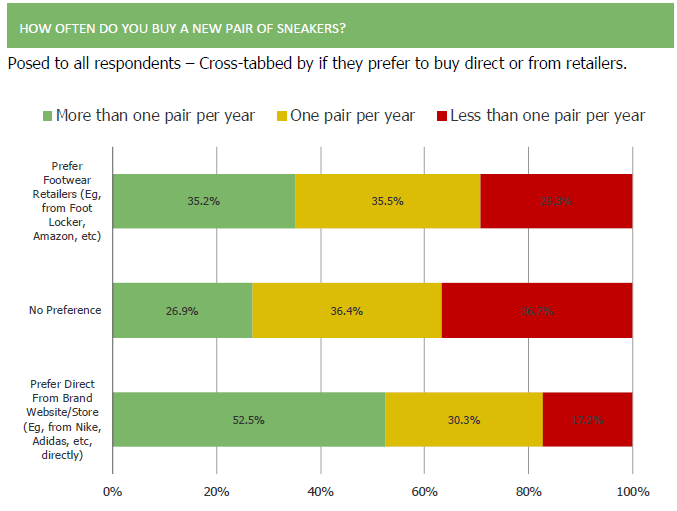

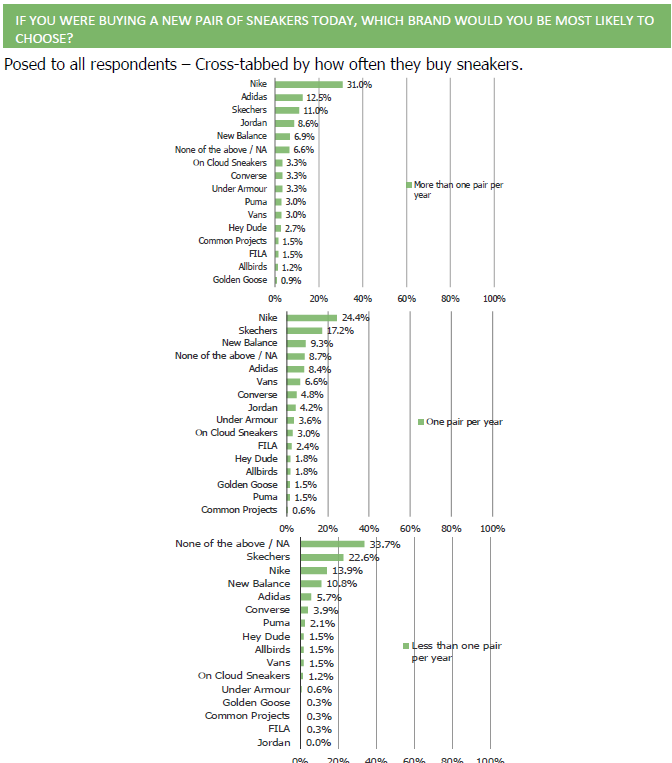

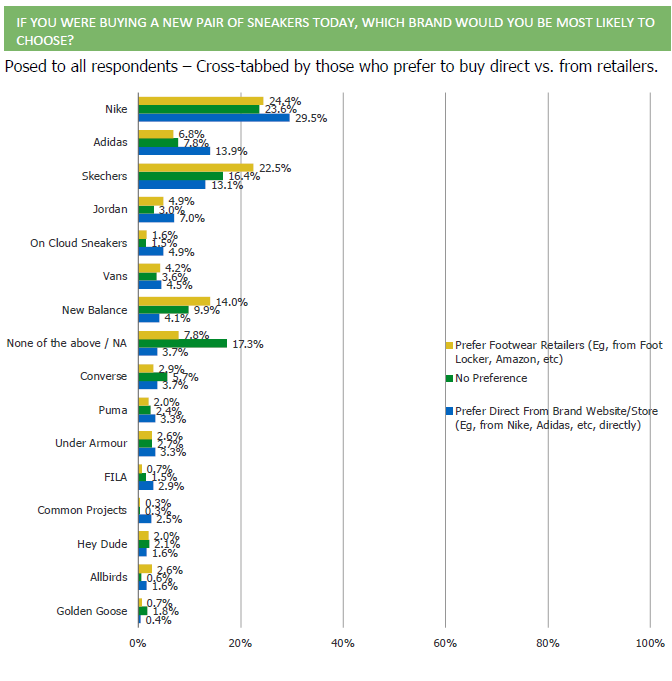

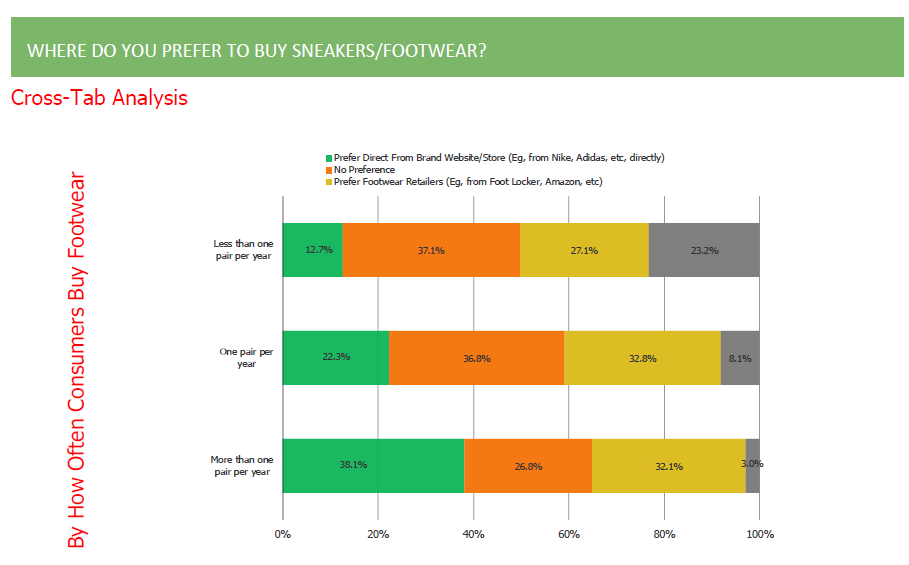

Respondents who prefer to buy sneakers direct from the retailer buy more pairs of shoes per year…

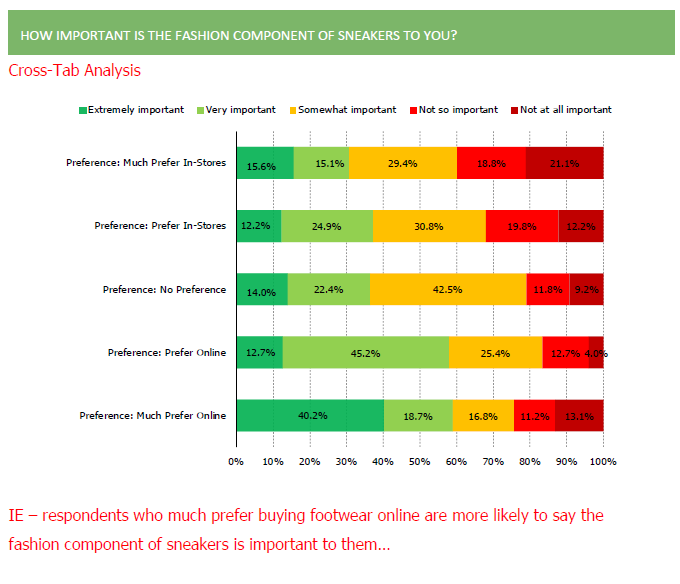

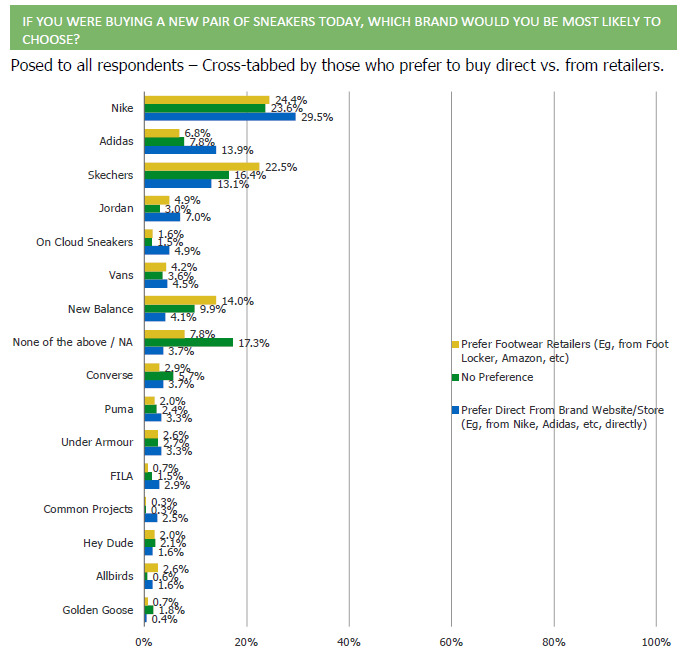

People who prefer to buy directly from the brand significantly over-index to a preference for ON Cloud sneakers… and indication of brand affinity that outstrips their current market penetration.

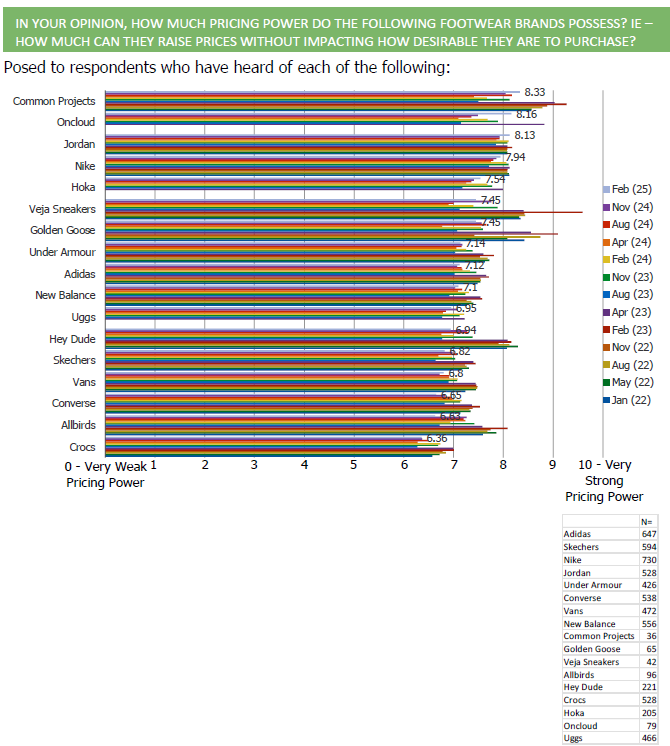

Consumers perceive the brand to have strong pricing power…

Their customer base feels good about their finances and are more sanguine on Tariffs than the broader population.

How would you currently describe your personal financial situation? When we refer to your personal financial situation, we mean factors that directly affect you — such as your income, ability to pay bills or make purchases, savings, job stability, and overall sense of financial security. This is about your own household finances, not the broader economy or what you’re seeing in the news.

Posed to On Cloud Customers

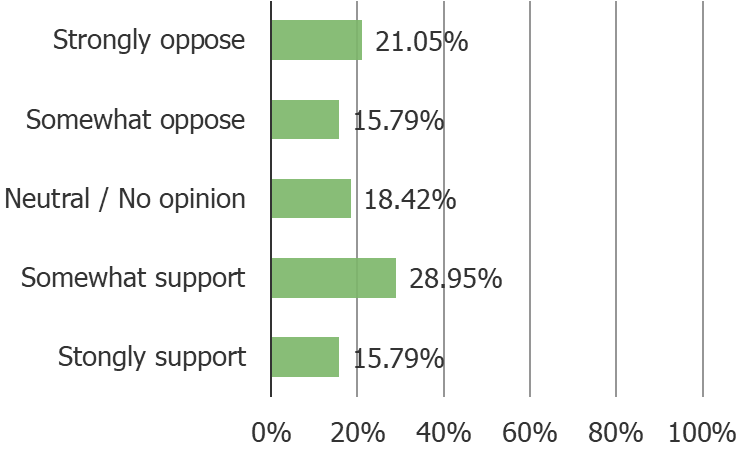

The U.S. has recently announced new tariffs on goods imported from a number of countries. Do you support or oppose these tariffs?

Posed to On Cloud Customers

Do you think the impact of tariffs will be…

Posed to On Cloud Customers

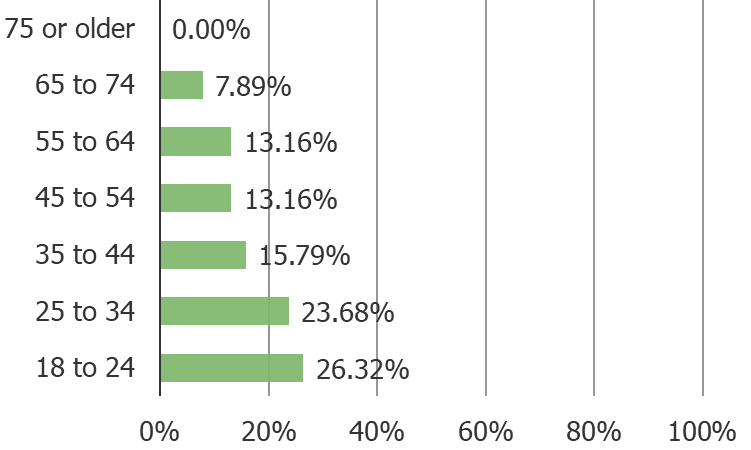

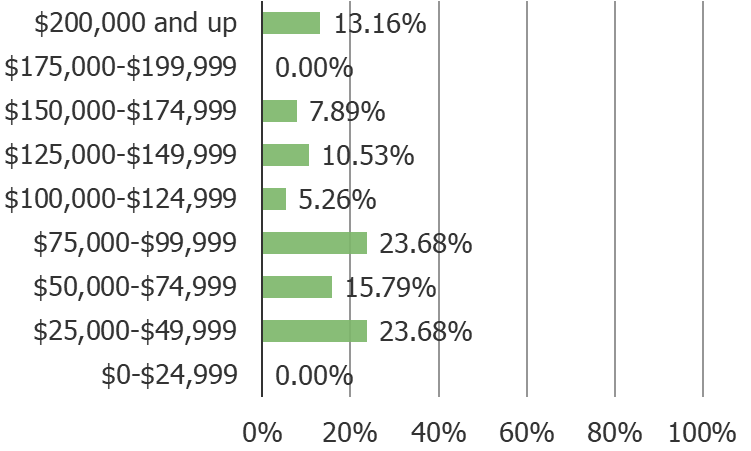

Their customer base over-indexes to higher income and younger respondents.

On Cloud Customers Demographics…

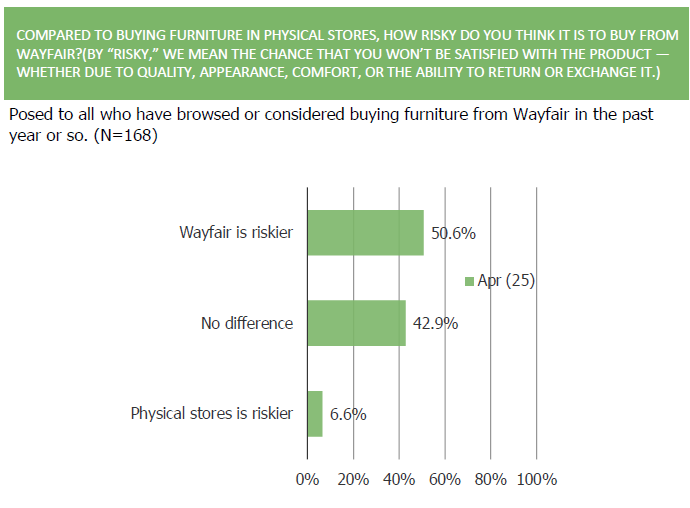

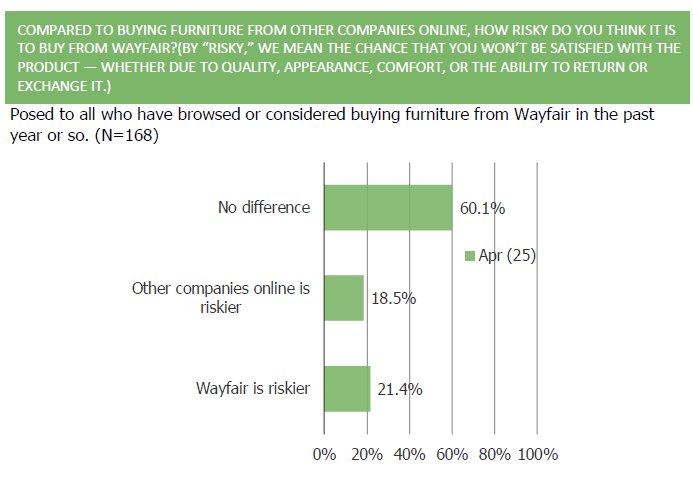

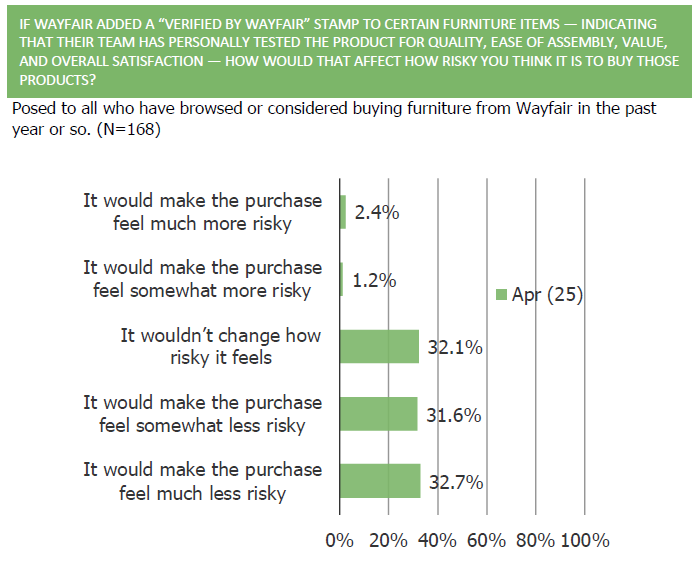

Wayfair’s Verified: Un-Wobbling Confidence

Wayfair knows what consumers are thinking: Is this $189 side table actually going to hold anything? Enter the “Verified” badge — their newest attempt to ease furniture anxiety without sending customers a wrench and a therapist. We surveyed 1,000 U.S. consumers and found that a surprising number say a little badge could go a long way. So… is trust just a sticker away?

The Problem: From our survey (chart below)… 50.6% of those who have considered buying furniture from Wayfair in the past year said that they perceive Wayfair to be “riskier” than buying from a furniture store in person (42.9% said no difference and 6.6% said physical stores are riskier).

The Solution: Wayfair Verified. Check out our blog post here to see how many of the folks above said that a “Verified by Wayfair” stamp would make the purchase feel less risky.

Charts Below!

X Money vs. Venmo and Zelle

Elon Musk’s X (formerly Twitter) is moving deeper into financial services with the development of X Money, a new payments system in partnership with Visa. This move could challenge established players like Venmo, Zelle, and PayPal, but how do X users actually feel about it?

In our latest mobile payments survey, we asked X users about their trust in X Money, how they might use it, and what features would compel them to switch. The results highlight both opportunities and challenges for Musk’s financial ambitions.

Key Findings:

- 67% of X users would trust X Money the same or more than existing providers like Venmo and Zelle.

- X Users would be most likely to use it for Peer to Peer payments, followed by Bill payments, E-Commerce transactions, and then business payments.

- The top two features that would compel X users to switch from their current payment app to X money are A) Faster Transfers and B) Lower Fees.

- 35.3% of X users said they would adopt X Money and would either reduce or stop using other platforms.

Further Reading:

If you are a client, log-in to view the full report (including more on this topic). If you are not a client and want to learn more contact us (pgorynski@bespokeintel.com).

Realtor Survey | NAR Settlement Fee Changes

The recent National Association of Realtors (NAR) settlement has introduced major changes to how broker commissions are structured, reshaping the landscape for real estate transactions. As these new rules take effect, realtors are adjusting their business models, and investors are eager to understand the financial implications of these shifts.

To gauge the real-world impact, we surveyed a panel of realtors to learn how they are adapting to the new fee structures. The findings reveal clear trends:

Reduced Commissions: 50% of realtors report a decline in their average commission per transaction, while only 9.6% have seen an increase.

Buyer Fee Negotiations Are Rising: 58.3% of realtors say buyers are more frequently negotiating their agent’s commission.

Changing Business Practices: Nearly 65% now require written buyer agreements before working with clients.

Our full report includes in-depth insights and data visualizations on these shifts. If you’re an investor, policymaker, or real estate professional looking to understand the evolving fee dynamics, this report is a must-read.

Contact us (pgorynski@bespokeintel.com) if you would like to see more insights from our deck and/or if you’d like to learn more about our proprietary panel of realtors and surveys.

Survey Excerpt:

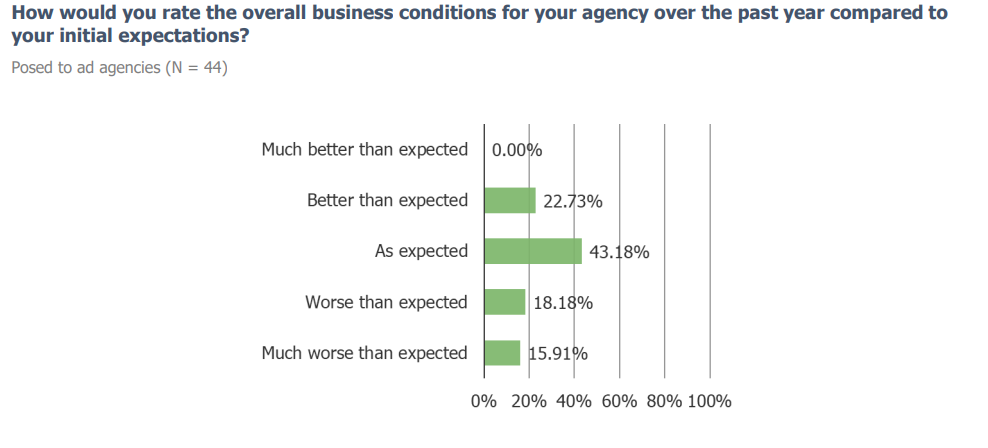

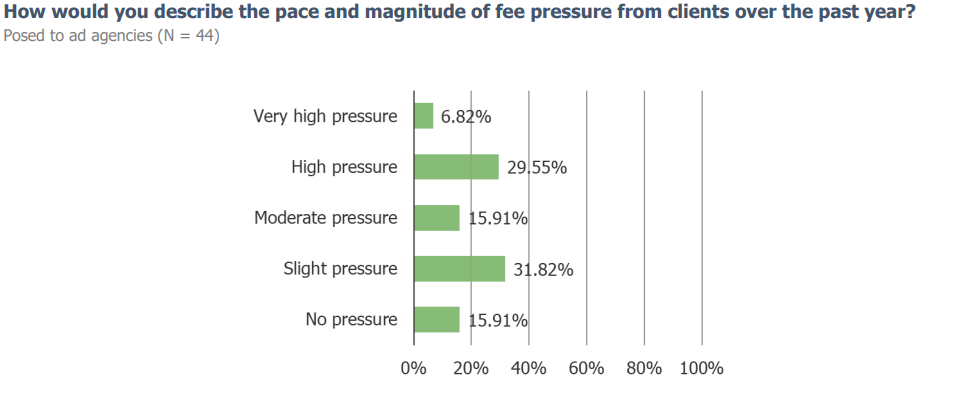

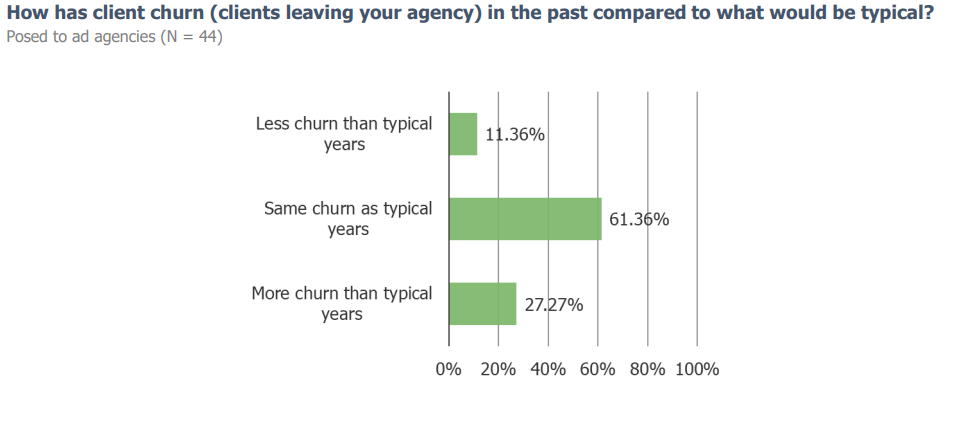

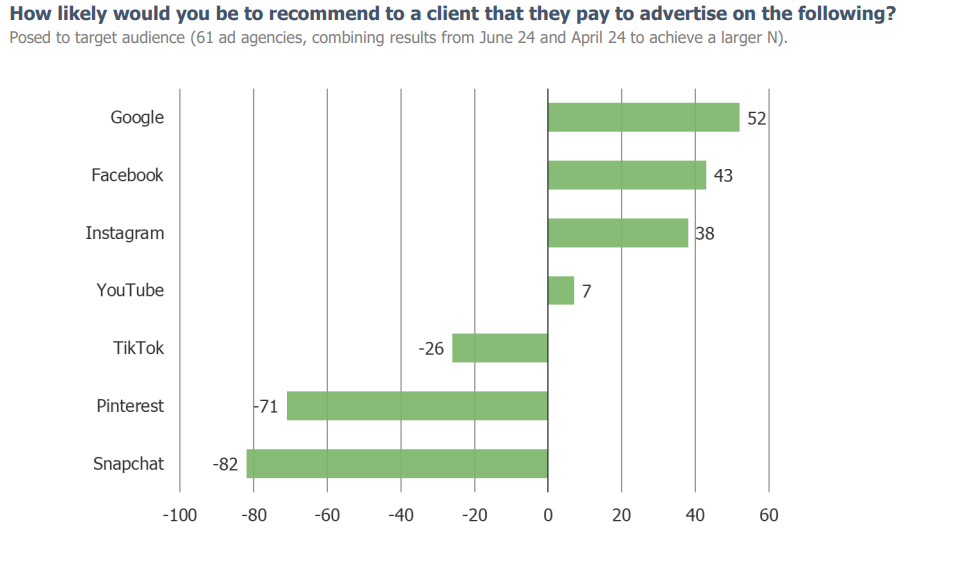

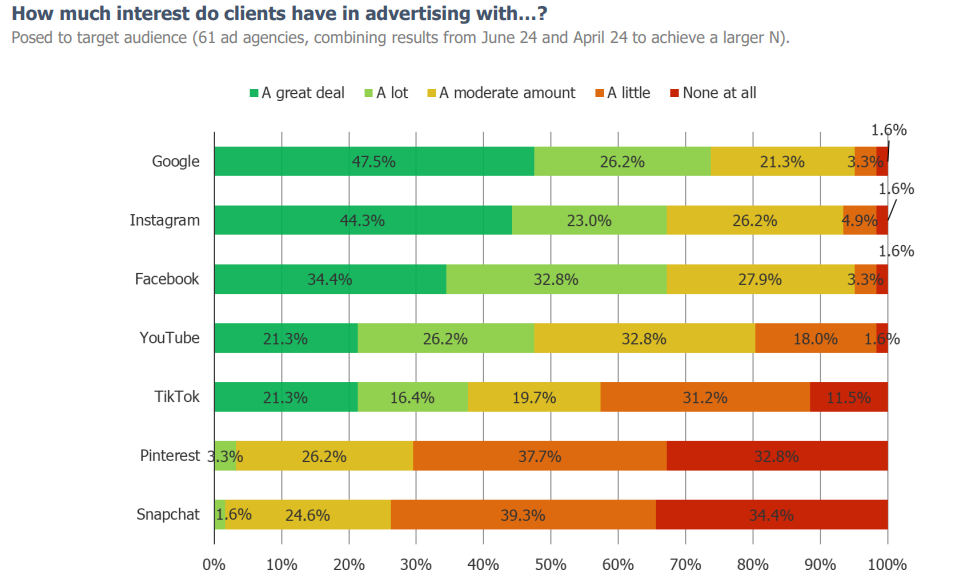

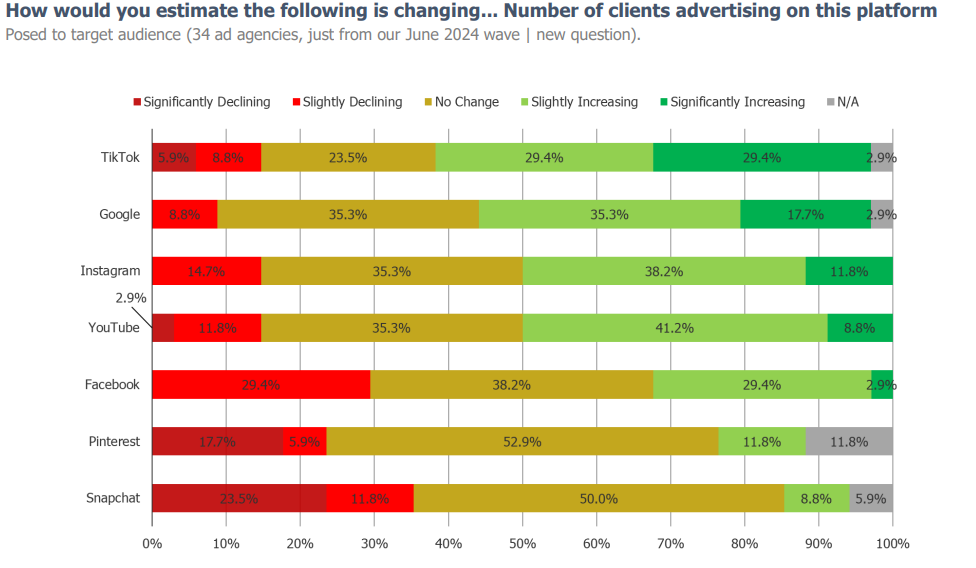

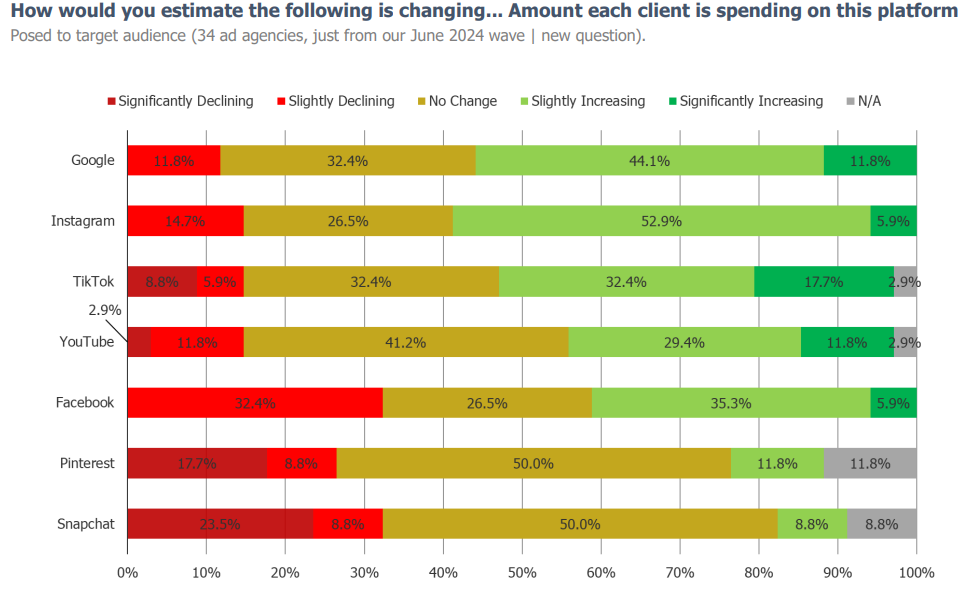

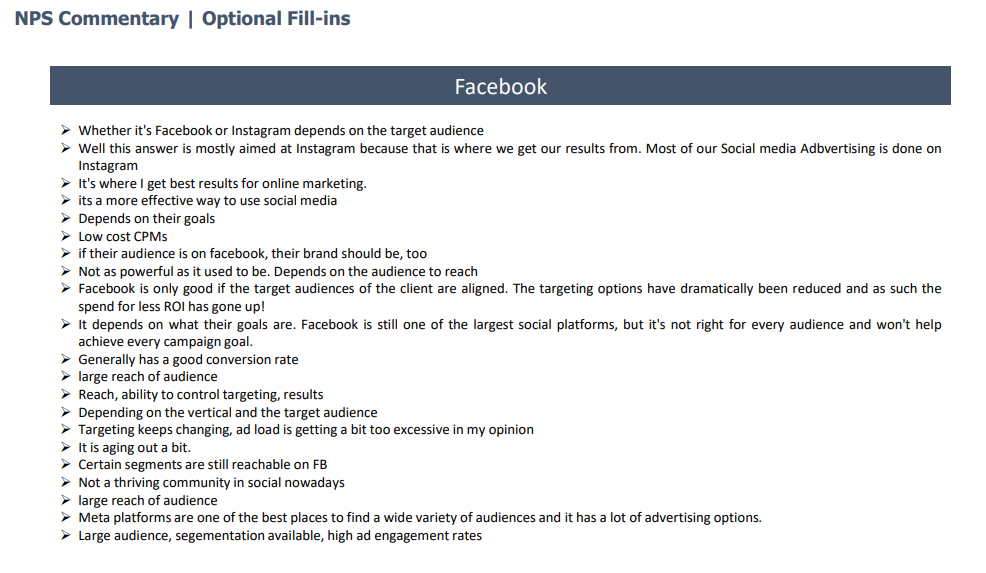

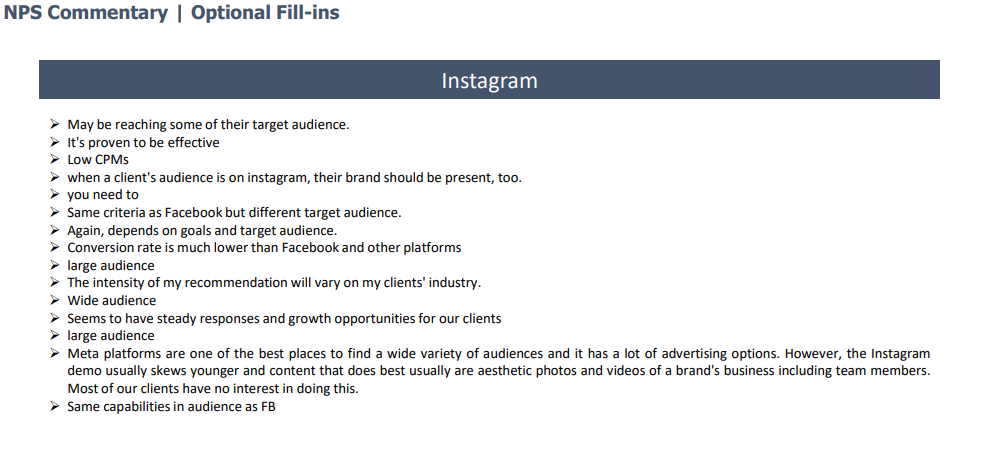

(GOOG, META) 61 Expert Network Calls in 5 Minutes

Some color below from our proprietary panel of ad agencies. These are folks who we found using our proprietary research recruiting methodology, not people we surveyed through a consumer panel by job title. That means very high quality responses (zero bots or fake respondents). Why spend hours on the phone with experts when you can absorb their feedback in a matter of minutes?

We will be re-running this ad agencies survey next week along with surveys on the below audiences. Start a trial with us today to check out the upcoming results / our full library.

Other B2B Audiences In Our Panel:

- Travel Agents

- SMB Owners

- Restaurant Owners

- Realtors

- HVAC Managers

- Construction Managers

- Chief Information Officers

- CFOs

- Doctors

- HR Managers

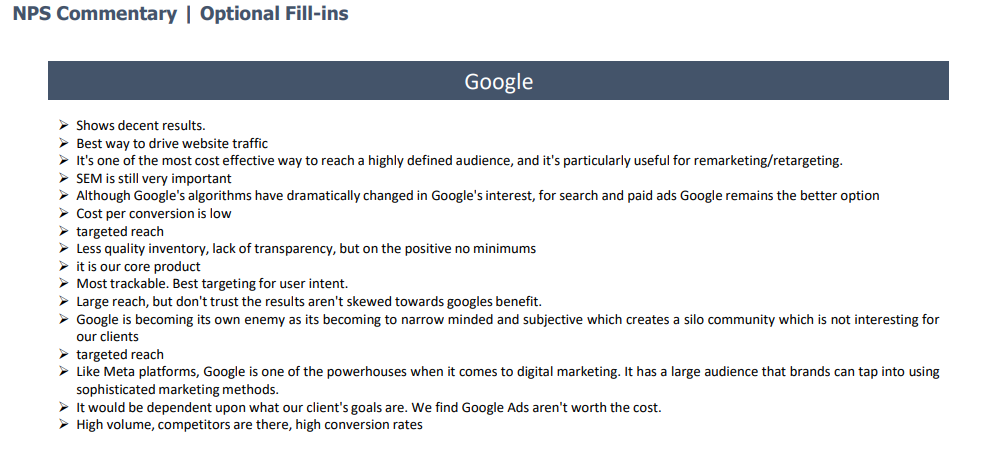

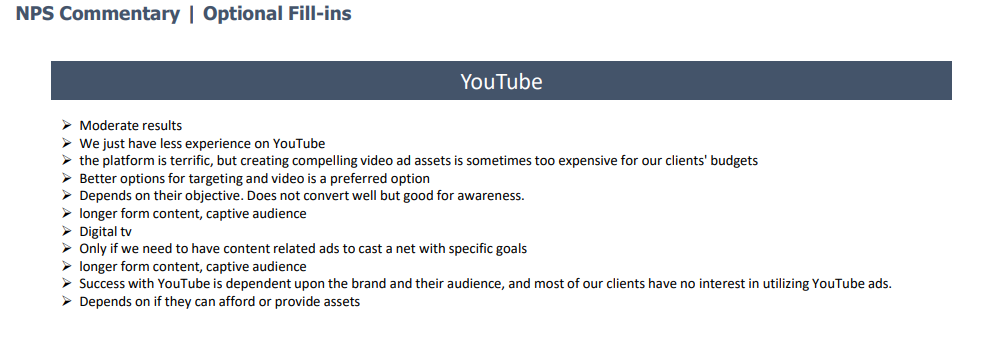

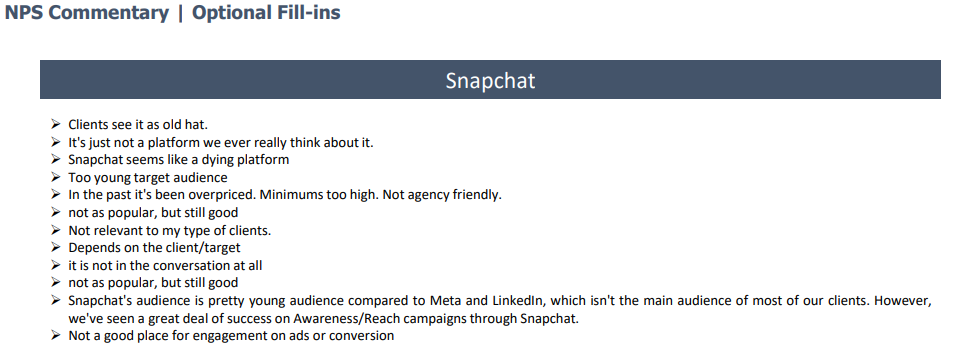

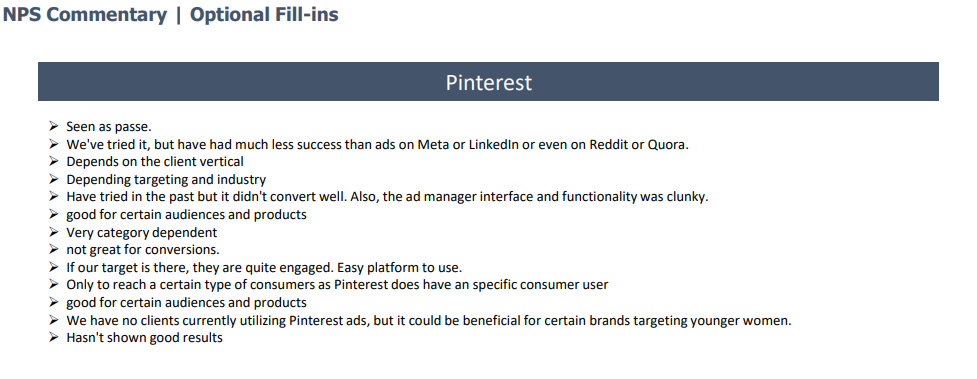

Ad Agencies | Social Media Platforms Color

Ad Agencies | AI Color